Schwab Market Perspective: Confidence is Key

Key Points

- The investing environment continues to be uncertain, with confidence among businesses and investors shaken. History, however, has proven that times like these can make or break successful investing strategies.

- The correction in stocks doesn’t yet seem to be corroborated by a sharp US economic downturn. In fact, recent economic data has been encouraging, but shattered confidence can lead to a self-fulfilling prophecy.

- Recent economic readings from around the world also suggest that the globe is not slipping into a recession.

Tough times

There are many words that could be used to describe the first six weeks of 2016 with regard to stock performance but given that this is a family publication we’ll stick with frustrating. There have been rebounds, including the latest fierce recovery which has taken US stocks out of correction mode; but a lot of confidence has been shattered. These are the times that can make or break an investing plan. Our long-held mantra is that panic is not an investing strategy and that investing should always be a disciplined process over time; never about decisions at moments in time. So we continue to give the advice that throughout history has proven to be effective and profitable—stick with your long term plan, take advantage of volatility to periodically rebalance portfolios and remain disciplined. Apocalyptic warnings often sound compelling because in effect they’re telling investors to do something right away. Long-term disciplined investing advice is typically not all-or-nothing, and is advice more sedate in nature, but it’s been time-tested over and over again.

Confidence has been shaken, which can create a self-fulfilling prophecy—although economic data has not deteriorated significantly, risks are elevated in terms of both further downside and the possibility we “talk ourselves into” a recession. Market-based indicators, like stocks, credit spreads and the yield curve (all until recently) have been suggesting recession risk is elevated; however, leading economic indicators are signaling a much less dire scenario. There is a reason for the old adage, “stocks have called nine of the past five recessions,” in that market-based indicators have had many false signals historically. One of the rationales for having a “neutral” rating on stocks (meaning investors should hold to their normal equity allocation) and not an “underweight” is our belief in the continued likelihood of fierce rallies in the midst of corrective phases. . Trying to time the short-term ups and downs of the market is extremely difficult, if not impossible to do consistently, and investors have often lost more money by trying to time the market than by riding out the storms.

Economy doesn’t reflect correction…so far

Part of the reason that the correction in stocks has been so frustrating is that the economy doesn’t seem to us to be reflecting that degree of negativity. Of course we understand that stocks are a leading indicator so the risk of a more serious economic downturn is elevated. And, as mentioned, corporate executives and consumers looking at a declining stock market may wonder what they are missing, and decide to hold off on investments and consumption until the dust clears, further pressuring economic activity.

But at this point the leading economic indicators continue to point to a decent US economic picture. In fact, after a disappointing 0.7% rate of gross domestic product (GDP) growth in last year’s fourth quarter, the Atlanta Federal Reserve GDPNow model, which is pretty widely respected and has a good track record, recently increased its estimate for first quarter 2016 growth to 2.7%, not robust but a long way from recession territory.

Further, other indicators are not consistent with an impending recession. US consumers continue to improve their financial position and represent 69% of US GDP. The low unemployment rate (4.9%) and continued historically low initial claims for unemployment may finally be pressuring wages higher. This should help to boost consumer spending, illustrated by a nice 0.4% month-over-month gain in retails sales, which doesn’t foretell a coming recession.

Rise in consumers’ earnings not consistent with recession

Source: FactSet, U.S. Dept. of Labor. As of Feb. 16, 2016.

Consumers have been getting an additional boost from falling oil prices, which have also never led into a recession—recessions are typically preceded by spiking oil prices.

Neither are falling oil prices

Source: FactSet, Dow Jones & Co. As of Feb. 16, 2016.

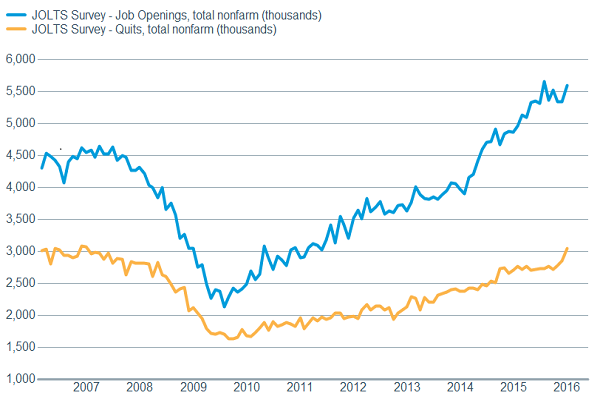

In addition, the recent release of the Job Openings and Labor Turnover Survey (JOLTS) shows that voluntary quits are increasing, which indicates greater confidence in the job market, while job openings also continue to rise.

JOLTS report indicates growing job confidence

Source: FactSet, U.S. Dept. of Labor. As of Feb. 16, 2016.

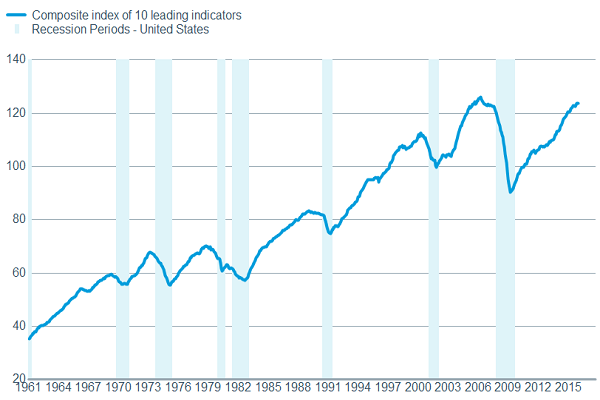

And finally, although the Conference Board’s Index of Leading Indicators (LEI) has weakened over the past two months, the six-month smoothed LEI remains healthy and consistent with decent economic growth, not an impending recession.

LEI hasn’t rolled over

Source: FactSet, U.S. Conference Board. As of Feb. 16, 2016.

The Fed is disconnected with the market

Unfortunately, part of the loss of confidence of investors may be as a result of a loss of confidence in global central banks, including the Federal Reserve, to continue to positively manipulate the financial markets. Given the Fed’s desire to move to a more “normal” monetary policy and the tightness in the labor markets resulting in wages starting to move higher, they still seem to have rate hikes in 2016 on the table. The market, in contrast, is now pricing in no hikes in 2016.

Given the Fed’s statements, we continue to lean toward no more than two 25 basis points hikes this year, but likely only after we see some stabilization in financial volatility. Making the Fed’s job even more difficult is the fact that close to a quarter of the world’s GDP is now operating with negative interest rates, something the Fed has indicated would be considered in the United States if conditions warranted them. In general, we believe much of the volatility in global markets is at least partly a function of the diminishing returns of excessive central bank interventions and the realization that central banks are not omnipotent and perhaps suffer from credibility problems.

Global recession worries may also be overdone

Expanding our view, world economic growth has remained below-average, but stable so far in 2016, according to January’s economic data and leading indicators. Nevertheless, global stock markets have already priced in a recession—although one that does not include the United States, based on historical averages. The global stock market measured by the MSCI ACWI Index (which includes the United States), fell -19.1% from April 27, 2015 to the low point on February 11, 2016. This loss is similar to the -16.8% average decline associated with global recessions (periods of sub-3% global growth) that did not include a US recession, as you can see in the chart below. Global recessions that included a recession in the United States saw an average bear market decline of -45.2%. While the risk of recession may have risen modestly this year, global stock markets may have been too aggressive in pricing in the certainty of a recession.

Global markets may already have priced in a recession

Source: Charles Schwab, FactSet, MSCI, OECD. Data as of 2/11/16.

Gray shaded areas represent global recessions where the U.S. was also in recession, blue shaded areas represent global recessions without a U.S. recession. Recessions as defined by the OECD based on peaks and troughs in the OECD reference series.

MSCI ACWI is the MSCI All Country World Index.

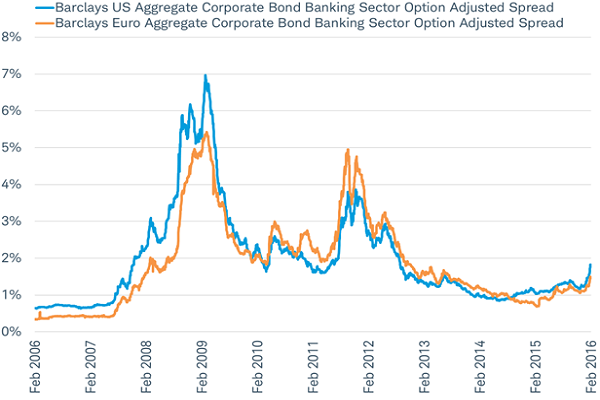

Global financial stocks have also been pricing in a negative environment in recent weeks. This year’s global stock market decline has been led by the financial sector, with the biggest declines seen in Europe. The selloff of financial stocks can be attributed to a combination of factors including central banks’ negative interest rate policies and a weak underwriting market for initial public offerings and high yield bonds. However, the declines do not seem to be associated with a global financial crisis resulting from deterioration of bank balance sheets, since credit spreads for banks have only modestly increased relative to the selloff in these stocks, as you can see in the chart below. Also, bank credit spreads in Europe have widened less than those in the United States, suggesting that the sharp selloff in global financial stocks is more motivated by weak earnings than weak balance sheets, translating to less risk of spillover to the global economy.

Rise in bank credit risk in 2016 remains well below 2008-2012 crisis period

Source: Charles Schwab, Factset data as of 2/17/2016.

China’s economic slowdown remains a source of concern for the pace of global growth. However, Chinese borrowing surged in January, as you can see in the chart below. While the spike for January looks impressive, actual growth in total outstanding borrowings accelerated only modestly to 12.1% year-over-year, up from 11.3% in December. Borrowing often starts out with a leap in January, as new loan quotas for the year unlock funds only to be followed by more modest growth as the year goes on. This year, the desire to refinance some foreign currency-denominated loans, and the timing of the Chinese New Year in early February, may have further boosted the January borrowing total. Growth in borrowing has been highly correlated with economic growth in China and may suggest policymakers are committed to stabilizing growth. The pace of borrowing was the strongest since early 2015, but remains below the 14.4% seen in 2014, and far from the 30%+ pace of 2009. January’s lending suggests a continued economic slowdown is still likely for China, but not a crash that would contribute to a global recession.

China’s January borrowing boom

Source: Charles Schwab, Bloomberg data as of 2/17/2016.

So what?

We understand that investing can be frustrating at times but history has proven that sticking with your long-term plan, if well put together, is very often the best course of action. At this point the US economy doesn’t appear to be heading into a recession, which should help to support stocks, but volatility is likely to persist. The Fed seems as uncertain as investors, and its official forecasts of short-term interest rates remain highly at odds with market expectations, adding fuel to the volatility. Globally, the markets have also been pricing in a recession that doesn’t appear to be in the cards in the near term, setting up for a potential rebound.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events will be created that may increase your tax liability. Rebalancing a portfolio cannot assure a profit or protect against a loss in any given market environment.

The Job Openings and Labor Turnover Survey (JOLTS), conducted by the Bureau of Labor Statistics of the U.S. Department of Labor, involves the monthly collection, processing, and dissemination of job openings and labor turnover data. The data, collected from sampled establishments on a voluntary basis, include employment, job openings, hires, quits, layoffs and discharges, and other separations.

The Conference Board Leading Economic Index is an American economic leading indicator intended to forecast future economic activity. It is calculated by The Conference Board, a non-governmental organization, which determines the value of the index from the values of ten key variables.

MSCI ACWI, a market capitalization weighted index designed to provide a broad measure of equity-market performance throughout the world. The MSCI ACWI is maintained by Morgan Stanley Capital International, and is comprised of stocks from both developed and emerging markets.

Barclays US Aggregate Corporate Bond Banking Sector Index is the banking component of the finance sector investment grade U.S. corporate bonds. Option-adjusted spreads (OAS) are quoted as a fixed spread, or differential, over U.S. Treasury issues. OAS is a method used in calculating the relative value of a fixed income security containing an embedded option, such as a borrower's option to prepay a loan.

Barclays Euro Aggregate Corporate Bond Banking Sector Option-Adjusted Spread is the banking component of the finance sector investment grade corporate bonds participating in the European Monetary Union. Option-adjusted spreads (OAS) are quoted as a fixed spread, or differential, over German government bond issues. OAS is a method used in calculating the relative value of a fixed income security containing an embedded option, such as a borrower's option to prepay a loan.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(0216-CSFS)