Corporate Caution…Global Recession?

Key Points

- U.S. equities have again failed to break out to new highs. A modest pullback is in keeping with our expectations and consistent with weak earnings and elevated valuations. We would like to see corporate confidence, along with earnings, rise to help fuel the next leg higher.

- The U.S. economy continues to muddle along, contributing to the lack of corporate and consumer enthusiasm. The Federal Reserve appears stuck, with the economy not firing on all cylinders, but with a desire to move interest rates to a more “normal” level.

- Global yield curves aren’t indicating we’re on the cusp of a global recession, which argues against the “sell in May” adage for longer-term investors.

U.S. stocks struggle to break out

A strong U.S. equity rally off the February 11th lows has paused, again failing to break through to new record highs. Since the S&P 500 hit 2,134 on May 20th of last year, stocks have had runs to the upside but have failed to reach all-time highs each time. The latest pullback came after the index reached an intraday high of 2,111 on April 20th, leaving equity investors with a very modest negative return over the past year.

It can be difficult to remain disciplined—it’s often at times like these when investors get impatient and reach for return by increasing risk, or conversely throw up their hands and get out of the market. Our perspective on stocks remains “neutral”, which means we suggest investors stick to long-term allocations, taking advantage of volatility for rebalancing purposes.

Companies remain cautious

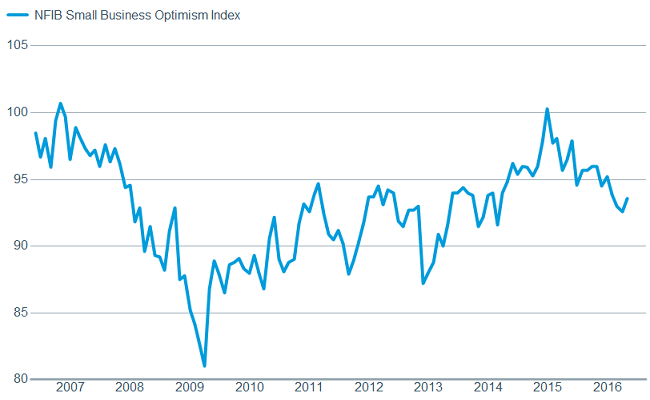

Whether it’s the economy failing to gain traction that’s causing companies to be cautious, or companies’ caution leading to the muddling environment is a bit of a chicken-and-egg debate. The recently released National Federation of Independent Business (NFIB) Optimism Index rebounded slightly but remains relatively low, while the percentage of small businesses planning on increasing capital expenditures over the next three-to-six months was also weak.

Business optimism remains dim

Source: FactSet, Natl. Federation of Independent Business. As of May 10, 2016.

On the manufacturing side of the U.S. economy, we continue to flirt with a recession, with Industrial Production falling again last month and the Institute for Supply Management (ISM) Manufacturing Index slipping back to near the dividing line between contraction and expansion.

Manufacturing flirting with recession

Source: FactSet, Institute for Supply Management. As of May 10, 2016.

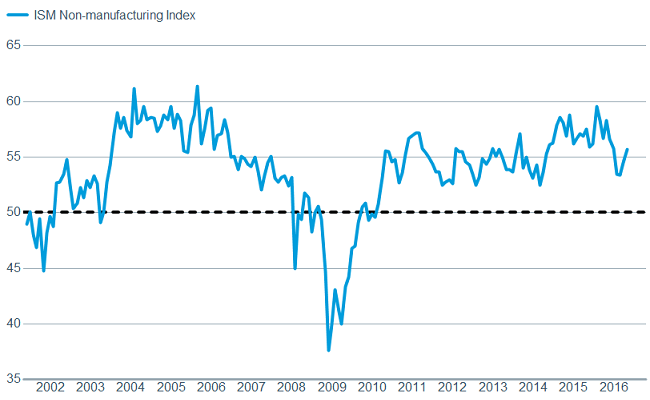

But positively, the much larger service side of the economy continues to hold up fairly well;, with the ISM Non-Manufacturing Index rising to 55.7 from 54.5 and the forward looking new orders component moving to a relatively robust 59.9. The labor market also continues to improve; but as we’ve noted in recent notes, the rate of improvement is likely to slow—the lower the unemployment rate, the fewer people there are to hire. The latest employment report showed that 160,000 jobs were added and the unemployment rate stayed steady at 5.0%. Wages appear to be gaining some momentum as average hourly earnings were up 2.5% on a year-over-year basis according to the U.S. Department of Labor.

But services are looking good

Source: FactSet, Institute for Supply Management. As of May 10, 2016.

And employment has improved substantially

Source: FactSet, U.S. Dept. of Labor. As of May 10, 2016.

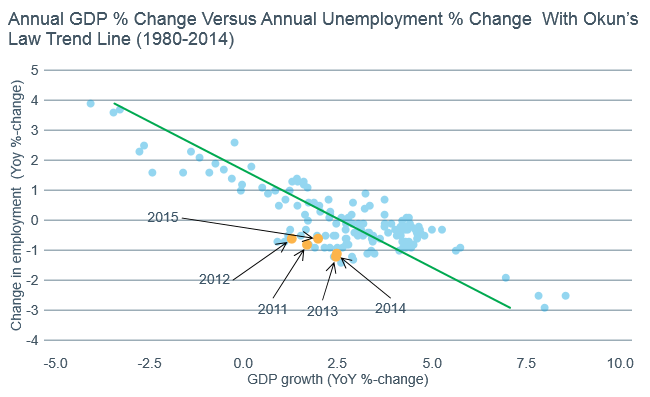

But here is where part of the problem appears to be. Since employment has improved so much, shouldn’t the economy be doing better? Historically, yes. According to “Okun’s Law,“ named after its discoverer Arthur Melvin Okun, for every 1% decrease in the unemployment rate we should see a roughly 2% gain in gross domestic product (GDP). As you can see in the chart below, until the last few years, that has held true.

The economy “should” be doing better

Source: Macrobond. U.S. Bureau of Labor Statistics, U.S. Bureau of Economic Analysis. As of May 10, 2016.

Okun's Law trend line – the relationship between unemployment and GDP, of when there is a 1% decrease in unemployment, there is a 2% increase in GDP.

Now the harder question—why is this occurring? There are many theories about why productivity has disappointed during this recovery, but a contributor seems to be companies being willing to add to labor but not spend money on equipment or technology that could help to boost productivity. If corporate leaders are uncertain about the future of the economy or are under the pressure of more onerous government regulations, it’s easier to let employees go than to sell equipment at fire sale prices during a possible downturn. This is the component we would like to see turn in order to fuel the next equity move higher.

Corporate profits as a share of U.S. GDP have peaked and are now trending down according to ISI Evercore Research. Inversely, labor costs/wages have troughed and are now trending up. This is good news for workers, but less good for profit margins (and potentially inflation). If corporate confidence improves, it should lead to increased capital expenditures, which should lead to an increase in productivity, and in turn economic activity.

Fed seems stuck

The Federal Reserve has been trying to get that ball rolling since the financial crisis through some extraordinary measures, with some success. The economy has recovered, employment has improved, housing has bounced back, and asset prices have appreciated. But the economy is still not firing on all cylinders. After keeping interest rates at effectively zero since 2008, the Fed is looking to move rates to a more “normal” level. There remains a risk of the Fed moving too quickly, but there are also risks to staying too low for too long---leaving the Fed in a difficult position as we head toward the next Federal Open Market Committee (FOMC) meeting in June. As has been the case over the past couple of years, we expect economic activity to pick up in the second quarter from the weak first quarter, but whether it will be enough to allow the Fed to raise rates again, it’s too soon to tell.

And then there were two

A lessening of the regulatory burden and/or getting a hefty dose of fundamental tax return would certainly help; but both are highly unlikely in advance of the November election. After months of debates, primaries, diners, town halls, tweets, etc., we are down to the two presumptive candidates who will square off in November. So what does it mean for the market? Typically the market doesn’t pay a lot of attention to elections until we get into the fall, but this is anything but a typical election year. We expect some increased election-related volatility, with rhetoric and passions running high.

Sell in May and go away? No way says the yield curve

On top of both corporate caution and political concerns, investors may be wondering if they should “sell in May and go away” given the historical tendency of stock market returns to be -lower during the May through October period. In recent years, pullbacks in global stocks during the summer have taken place in five of the past eight years: 2008, 2010, 2011, 2012, and 2015, as measured by the MSCI ACWI Index. But four of those five periods amounted to mere volatility as stocks rebounded several months later. Only the 2008 losses were sustained given the global financial crisis and recession. Barring a recession, any weakness during this period is likely to be contained.

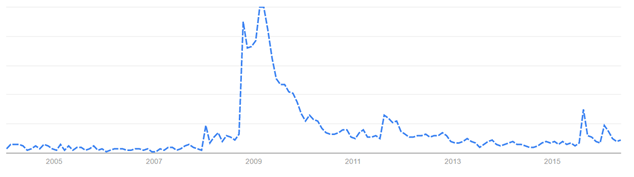

The declines of more than 10% in the global stocks measured by the MSCI ACWI Index that took place last fall and again early this year coincided with spikes in Google searches for the phrase “global recession,” as you can see in the Google Trends chart below. The recent spikes in search interest are minor compared with the anxiety reflected at the peak of the global recession and financial crisis in 2008 and 2009. However, they were similar to those seen during the 2011 European debt crisis. The pickup in market volatility seems to have some investors concerned about prospects for a global recession and an accompanying prolonged bear market.

Search interest for "Global Recession"

Source: Google Trends-Numbers represent search interest relative to the highest point on the chart.

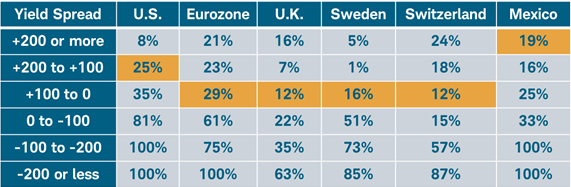

Those investors may be able to breathe a little easier. Global yield curves indicate a low probability of a recession in the world’s major economies in the coming year. Historically, a reliable indication of a recession within the coming year in economies around the world has occurred when central banks hike short-term rates and the spread between short and long term interest rates, known as the yield curve, turns negative. The more the yield curve is said to flatten—meaning short-term interest rates rise relative to long-term rates—the higher the probability of entering a recession within the next year, as illustrated in the table below.

Yield curve suggests 12-29% odds of a recession in the year ahead for various countries

Yield spread is in basis points. 100bps = 1%. Shading refers to where the yield curve is as of 5/11/2016.

The yield spreads for each country/region are measured using the spread between the 10 year and 3 month yields, except Mexico, which is 5 year and 3 month, and Eurozone, which is 10 year and 2 year.

Historical time period begins: U.S. 1967, Eurozone 1970, UK 1970, Switzerland 1975, Sweden 1970, Mexico 2000.

Source: Charles Schwab, Macrobond data as of 5/11/2016.

Fortunately, the chance of a recession over the next 12 months among many of the world’s largest economies is currently indicated to be between 12-29% by the yield curves in these countries. While that is certainly above zero, the chances of a recession are never as low as zero, but they are - below 50%. However, it is worth noting that if yield spreads were to drop by another 100 basis points for the Eurozone and Sweden, the risk of recession indicated by the yield curve would jump to over 50%.

Although current interest rates in many economies are very low in absolute terms (and even negative in some), the yield spread has been a useful indicator of a forthcoming recession at all yield levels. Nevertheless, some investors may believe central bank manipulation is biasing the signal from this time-tested indicator. This is worth consideration since negative interest rates have pushed down short-term rates in some countries to below zero and quantitative easing (QE) bond buying programs have pushed down long-term yields. Fortunately for investors, these central bank policies are distorting yields each in their own way; but these two policies together tend to offset each other and have a neutral net effect on the signal from the yield curve.

For example, it is easy to understand how the June 2014 adoption of negative interest rate policy by the European Central Bank (ECB) has been pulling short-term rates lower, as you can see in the chart below.

Eurozone 3 month yields fell below zero after ECB adopted negative interest rate policy

Source: Charles Schwab, Bloomberg data as of 5/11/2016.

On the other hand, our analysis of the futures market expectations for a rate hike by the ECB and long-term bond yields in the Eurozone suggest that longer-term rates are being pulled lower by a similar amount since the ECB introduced QE, as you can see below.

Eurozone 10 year yields widened gap with expectations for timing of first rate hike after ECB adopted QE

Source: Charles Schwab, Bloomberg data as of 5/11/2016.

These two effects are offsetting on the yield spread leaving us to conclude that the yield curve is likely to remain a useful (though not perfect) indicator of recession. We believe growth is likely to remain below average, but avoid a global recession and accompanying prolonged bear market over the coming 12 months. That suggests long-term investors should ignore the old adage to “sell in May” and instead stick with their diversified asset allocations and rebalance as needed.

So what?

Uncertainty among investors and companies has resulted in equities failing to push to new highs…for now. We remain fairly confident that stocks will reach new records, but patience in the near term is required. And selling in May doesn’t appear to be a great strategy for long-term investors as global yield curves are indicating low odds of a global recession. Perhaps hold in May is more apt. Bouts of volatility are likely to persist in light of uncertainty over Fed policy, the upcoming election, and global growth concerns.

© Charles Schwab