This weekend, my son and I had an opportunity to enjoy the Dairyland Classic at Road America, a spectacle of motorcycle racing at one of the best road courses in the United States. One of the things you learn if you follow these racers, who travel at speeds up to 180 mph around the 4 mile track, is that every move they make, each second, has a meaningful impact on the outcome of their race. One bit of hesitation, turning a few feet too early or late, and the racer’s place is at stake. It is safe to say that the Federal Reserve has a lot more time to determine their next move than these motorcycle racers.

Jobs

Last Friday, we received another “jobs” report for the month of May. These reports have taken on tremendous meaning as investors tend to look at the headline number and focus too much attention on whether it will impact the next interest rate increase by the Federal Reserve. In the very near term, the numbers only matter to speculative investors with a time horizon not much longer than that of those motorcycle racers. To us, and to our clients, how the economic data evolves over longer periods of time is more relevant. First, let’s look at last Friday’s information in the context of a longer dated view.

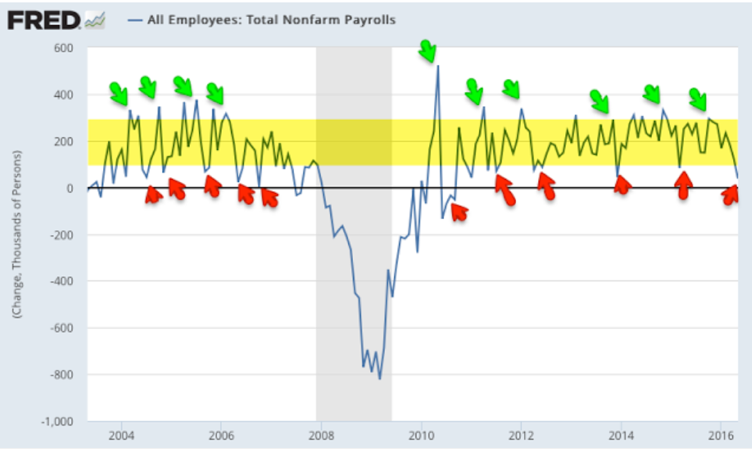

The headline report that got financial media tongues wagging, was the unimpressive 38,000 jobs created. Adding back the near 35,000 Verizon workers who were on strike and depressed the report, it was still only 73,000 for the month of May. This compares to a longer-term average nearer 180,000 jobs per month. However, the number of jobs created each month and reported as “Total Nonfarm Payrolls” is a seasonally adjusted number and so gets revised quite a bit. As an example, last Friday’s announcement also included a downward revision to April and May of 58,000 jobs. The chart below looks at the monthly report, and the highlighted area represents a monthly job creation number between 100,000 and 300,000. As you can see the monthly statistics are volatile.

Looking under the hood (or “fairing” if you race motorcycles) of the headline number we can see some important confirmation of current trends. The education, health care and business service sectors of the economy reported 77,000 jobs created. At the same time, manufacturing, construction and mining reported a job decline of 41,000 during the month. We know that the services sector of the economy has been healthier. And so, the jobs number in that part of the economy was not surprising. However, we also know that the housing market has seen a significant recovery, so it is likely that the construction part of the report is a blip in an otherwise positive trend. Still the report confirms continued weakness in manufacturing and energy (mining). We must keep in mind that this makes up less than 17% of the total economy, while the service sector is over 50%.

More importantly, the wage component of the report confirmed the current trend and showed modest improvement. Average hourly earnings were up 2.5% year-over-year and that confirms a steady growth rate in the fuel that adds to individuals’ ability to consume. Knowing that consumption continues to be one of the main drivers of our economy, a steady wage growth rate is important. We also note that it is not so high, that either wage inflation or faster economic growth is in the offing. That likely means that this is another data point confirming the very slow growth economy for 2016.

Time Horizon

Slow growth is what matters to the Federal Reserve and should matter most to equity and fixed income investors. While we’ve seen a slight uptick in the inflation rate, it isn’t likely that it will be so high as to cause central bankers concern about the pace at which they raise rates. In addition, slow growth will hamper the amount corporate earnings can grow, putting the current valuation of equity markets at risk as we move through 2016.

We are reminded however, that despite the fact we have a time horizon more like the motorcycle race team owner, which lasts many seasons, rather than the racer in a particular race, we can take advantage of market dislocations coming from an over-reaction to the information received in one report such as the nonfarm payroll report Friday.

Here is an example. Bond market participants were quick to add to re-priced bonds, raising prices and lowering yields to levels not seen in some time. The 10-year Treasury closed on Friday with a yield near 1.70%. Given that the current fair market value yield for that same security is closer to 2.25% (notice I didn’t say something like 3 or 4%), the price rally provides an opportunity to take profits in bond portfolios and re-position for a slight increase in yields. For those investing in much shorter maturities, say less than three years, it is an opportunity to reduce average maturity in advance of the inevitable increase in the Fed Funds interest rate, the rate the short end of the yield curve trades with.

Fed Funds Rate

I say “inevitable” because it is. While we are in the camp that rates may only go up by one or two .25% moves per year (we haven’t had any yet in 2016), the Fed Chair’s caution one week ago seemed telling. In her speech on May 27th, she noted that “we have limited scope for responding, and it is a reason for caution.” What she was saying is that an economic downturn is inevitable. If short-term interest rates don’t rise, even slightly, there will be little the Fed can do with normal monetary policy to stimulate growth, their normal course when we have a recession. In other words, if they don’t raise rates, even slightly, they won’t be able to reduce them.

So for now, we expect more of the same in terms of economic and profit growth. Slow. However, occasionally we will receive a piece of data that suggests the trend is no longer intact, markets will over-react and that will create opportunity. That is what racing and investing is all about. Understanding the course of events and knowing when and how to take advantage of opportunities when they present themselves.