Johnson Financial Group

Fed’s Warsh Era Begins with Hawkish Tone

The Federal Reserve left interest rates unchanged at its June 17 meeting, but investors were more focused on the future under new Fed Chair Kevin Warsh, whom Trump appointed in May.

Why Are Stocks So Resilient? Earnings!

Since early April, U.S. stocks have rallied sharply despite an ongoing war, rising inflation fueled by soaring oil prices (near $100/barrel), higher bond yields (up 0.6 to 0.7 percentage points), and frothy valuations (21 times projected earnings vs. a historical average of 17 times for the S&P 500 Index).

2026 Investment Outlook: Process Over Predictions

Our underlying theme for 2026 is that investors should focus on Process Over Predictions. The instinct of many investors is to chase the "winners" of the previous cycle or expect spectacular growth to continue indefinitely.

AI: A New Mom’s Best Friend

This year has certainly been a significant one for me. For the markets and the economy, it has been a big year as well. Rate cuts and no recession have been positive for stocks and bonds.

Living Up to Lofty Expectations

This Packers season has parallels to today’s financial markets. The Artificial Intelligence (AI) boom has propelled markets higher for the past 3 years. The S&P 500 is up just shy of 15% through 9/30/25, following 20%+ years in 2023 and 2024.

Alternative Assets in Defined Contribution Plans

Business owners who sponsor 401(k) and other defined contribution plans will soon be faced with another decision: whether to offer alternative-investment options among a plan’s investment options.

Risk, Reward, and Rory at the Masters

Elite golf is a mental game as much as physical—and so is investing. This year’s Masters tournament was one of the most compelling I have ever witnessed, and Rory McIlroy’s long-awaited playoff victory contains a number of life lessons that are relevant for investors.

Bonds Beckon with Higher Yields

Bonds look attractive again after the most recent rise in interest rates. Markets are likely to continue to overreact to every new employment report and inflation reading, keeping interest rate volatility elevated as yields dance up and down with each data point.

What Really Matters – In Investing

At the time of year where everyone is reflecting on the things that matter most to them in their personal lives, it is important to also consider what matters when it comes to investing. In this investment commentary, Johnson Financial Group shares what really matters as you put your money to work.

Just Give Me 5%

Money markets paid nothing. The dividend yield for the S&P 500 Index was 2%, and the 10-Year Treasury yield was stuck between 2%-3%.

“Are We There Yet?” Positioning Bond Portfolios for Peak Rates

The post-Covid era seems ripe for a Yogi-ism since economists and policymakers have been so wrong about the path of the economy and inflation. Yes, inflation is finally on a downward trend, but it has proven far stickier than the Federal Reserve and most economists predicted and remains above the Fed’s 2% target.

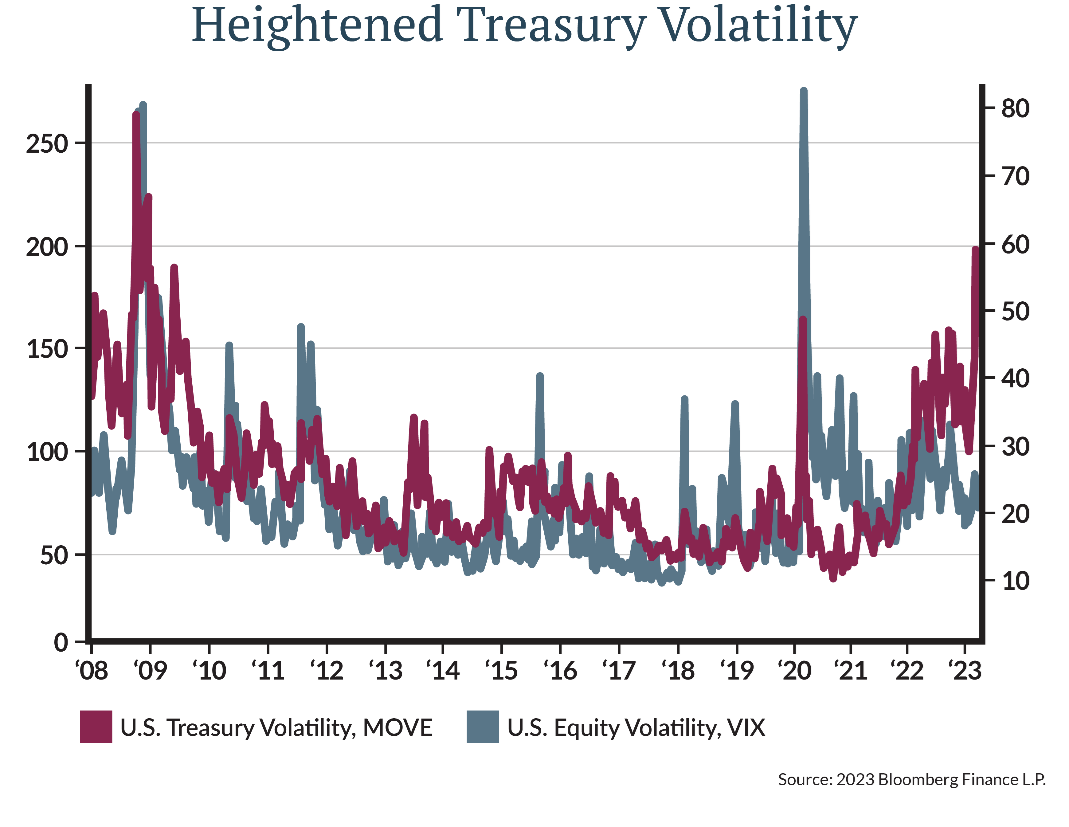

“The Fear Index” and “A Gentleman in Moscow”

During his spring break, Johnson Financial Group Portfolio Manager Brian Schaefer had the time to read “A Gentleman in Moscow,” which got him thinking about the how the current market moves could impact the American experiment. In this investment commentary, Schaefer discusses the MOVE and VIX indexes and what they might say about the markets.

Complementary Asset Classes: Why Now?

Given that (1) investors have benefitted from a market environment that reliably produced a source of positive returns from a 60/40 mix, and (2) we’ve just completed the best period for that mix in nearly 70 years of tracking, why would an investor want to consider a change?

Q2 Equity Outlook: Equities Continue on Recovery Rally

Just over a year since the COVID-19 virus began spreading around the globe and significant portions of our economy shut down, today the U.S. is solidly on the road to recovery.

First Quarter 2021 Economic & Market Outlook: Looking Beyond the Traditional

In a year that offered a pandemic and an election as reasons for investors to bail on risky assets, 2020 turned out to be a great year for those that stayed the course. A 60/40 portfolio of diversified stocks and bonds increased by a double-digit percentage, exceeding expectations.