Economic surprises may be peaking

Source: FactSet, Citigroup. As of Feb. 6, 2017.

At some point, perhaps soon, the inflection point will be reached in the opposite direction. That doesn't mean things are getting worse, just that expectations are catching up with the improvements in the data, which could have a dampening impact on investor enthusiasm in the near term. For example, the Consumer Confidence Index produced by The Conference Board pulled back a bit recently but still remains quite high. After jumping to 113.3 in December to the highest level since 2001 it pulled back to a still-robust 111.8.

Consumers remain confident, but rate of improvement may be leveling off

Source: FactSet, Conference Board. As of Feb. 6, 2017.

But despite a potential reduction in upside surprises, the data continues to look good. The Institute of Supply Management's (ISM) Manufacturing Index rose again to 56.5 from 54.5. For context, the average level in 2016 was 51.5 and in 2015 it was 51.4, so it seems clear that manufacturing sentiment has broken out on the upside. Additionally, the new orders component, which is more forward looking, remained robust at 60.4. The service side of the economy also continues to look good, with the ISM Non-Manufacturing Index posting a solid reading of 56.5, just a tick lower than the previous month. The labor market is equally strong, with a better-than-expected 227,000 non-farm payroll jobs added in January. The unemployment rate did tick up to 4.8% from 4.7%, but that was for a "good reason" and due to the participation rate rising from 62.7% to 62.9%. Wage growth fell back toward its recent trend, but we continue to believe the labor market remains tight enough to keep wage growth on an upward trajectory.

The story is much the same with the now-mature earnings season. Expectations going into the season were elevated, so investor reaction to releases was more cautious than we have seen in previous quarters. Results that beat expectations weren't necessarily rewarded to the same degree as during the past several reporting periods, while misses appeared to be punished a bit more harshly. This is to be expected given higher expectations, but the results themselves were largely positive and as mentioned above, the forward-looking commentary from managements remained cautiously optimistic. Patience is likely to be required with regard to potential tax and regulatory reform, but ultimately we do believe that if something on both fronts gets done this year it would be a meaningful net positive for the earnings.

Fed also remains cautious

The January Federal Open Market Committee (FOMC) meeting ended with no rate hike, as expected; while the accompanying statement that was perceived to be slightly more dovish than expected (read more from Liz Ann here). If economic data continues to surprise on the upside, a March rate hike is likely to be on the table; while there is an additional risk that the Fed may be forced to speed up the tightening process should inflation accelerate from here.

Better growth and bigger risk

Despite uncertainty over political developments, the U.S. economy has accelerated thus far in 2017, as seen in the Citi Surprise Chart above. However, January's economic data confirms that the growth outlook for the rest of the world is stable, but not as bright.

-

United Kingdom - The UK economy grew a bit faster than expected in the second half of last year, confirming that the Brexit vote had little immediate impact. While it appears to us January data sustained this pace, gross domestic product (GDP) growth may slow from last year’s 2.2%, as higher inflation slows real household spending and evolving Brexit negotiations limit business investment. But the positive impacts of looser monetary policy and the weaker British pound may help prevent a steep slowdown or recession in 2017.

-

Europe - Growth in the Eurozone accelerated a little in the fourth quarter of 2016, and it appears to us the January data suggest the economy has maintained momentum into 2017. However, we do not expect a further pickup in GDP growth beyond 1.6% this year, as the impact of rising energy costs acts as a drag on consumers’ disposable incomes. In addition, heightened political uncertainty ahead of key elections in France and Germany is likely to weigh on business investment.

-

Japan - Japan's growth may experience another year with less than 1% GDP growth; as the ongoing drags from demographic declines in the workforce, combined with weak income growth, are only partly offset by aggressive stimulus programs and a weaker yen supporting exports.

-

Emerging markets - In emerging economies, we expect growth in China to slow this year as stimulus has already been scaled back. This is evidenced by the raising of a key cost of loans by China's central bank, and in our view the focus has shifted (perhaps only temporarily) to containing bad lending rather than boosting growth. Brazil and Russia may emerge from recession this year thanks to the partial recovery in commodity prices, but tight budgets may keep a lid on GDP growth in both countries at around 1%.

Summing up, global growth may pick up slightly from around 3.1% in 2016 to 3.4%, according to International Monetary Fund (IMF) estimates. However, this slightly-better real (inflation-adjusted) growth is combined with an increase in inflation of one percentage point to 1.7%, to produce nominal GDP growth of 5.1%. This was the first time growth has been at or above the 20-year average since 2011, as you can see in the chart below.

Nominal global GDP growth may return to 20-year average in 2017

Source: Charles Schwab, Bloomberg data as of 2/8/17.

A risk to better global growth in 2017 is the threat of trade wars. With global trade equivalent to two-thirds of global GDP, even changes among just a few countries can have a material impact on global growth and corporate sales. There are a few things to keep in mind on trade developments:

-

No abrupt changeshave been made. The Trump administration did not label China a currency manipulator on day one. Instead President Trump has started his trade agenda by focusing on negotiating with Mexico, before moving to China and other trading partners. These developments signal a deliberate approach, rather than abrupt changes.

-

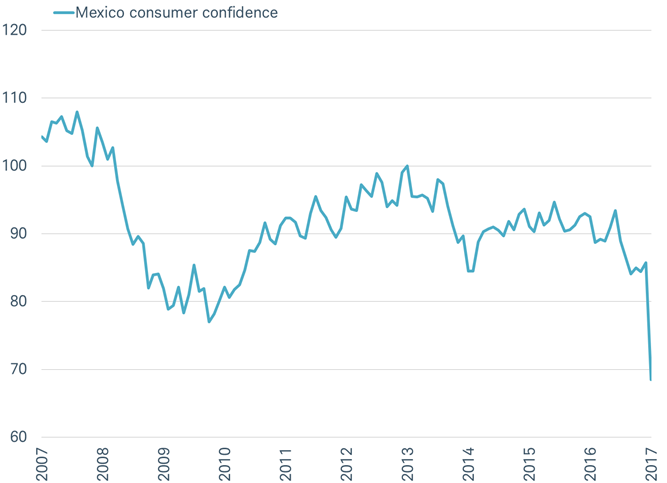

Stocks are taking the trade issues in stride, so far. The response in the markets has been mild, with the U.S., Mexican, and Canadian stock markets posting year-to-date gains. Yet some worries are being felt, as we can see in the record drop in Mexican consumer confidence in January.

Some trade-related worries are being felt

Source: Charles Schwab, Bloomberg data as of 2/8/17.

-

The collapse of NAFTA could have immediate and serious consequences for the U.S. and Mexican economies. The North American Free Trade Agreement (NAFTA) encompasses the United States, Mexico, and Canada (two of the United States' three largest trading partners). If it were scrapped, supply chains could break down and jobs would be lost on both sides of the border. Deteriorating economic conditions in Mexico could prompt more undocumented immigrants to move across the border.

-

The NAFTA talks may stretch out over much of 2017. Wilbur Ross, Trump's nominee for Secretary of Commerce, is slated to lead the talks with Mexico once his appointment is confirmed; and Mexican officials seem prepared to begin discussions. Ross has said he thinks tariffs are the last resort, and that he considers trade agreements a better way to achieve free trade while safeguarding U.S. interests.

-

Talk of deportations and a proposed border wall might create enough controversy to derail NAFTA talks. President Trump's repeated statements about having the Mexican government pay for a border wall doesn't actually involve NAFTA, but may make it politically difficult to cut a deal.

In our view, the global stock market impact of a trade war with NAFTA countries would be negative, but recent developments since President Trump has taken office suggest a process that may lead to months of talks rather than actions, allowing the market to adopt a wait-and-see attitude to how the deal may develop. Nevertheless, a potential trade war remains a risk to better economic growth in 2017.

So what?

Patience is key for investors, with political realities colliding with hoped-for reforms. Elevated earnings and economic expectations could lead to a pullback or more sideways action. Ultimately, we believe fiscal stimulus is coming—although perhaps later than anticipated—and the bull market in U.S. stocks will continue. International economic growth is stable, but does not appear to be accelerating, leading us to favor U.S. stocks over developed international stocks at the present time.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The Chicago Board of Exchange (CBOE) Volatility Index (VIX) is an index which provides a general indication on the expected level of implied volatility in the US market over the next 30 days.

The Consumer Confidence Index<.strong> is a survey by the Conference Board that measures how optimistic or pessimistic consumers are with respect to the economy in the near future.

In Mexico, the Consumer Confidence Index (ICC) measures the current perception and future expectations that people have about their economic situation, their family and the country in general, in respect to the purchase of consumption durables and non-durables, as well as employment, inflation and savings. The index is based on a sample of 2336 households located in the 32 major cities of the country. The ICC has a base of 100 as of January of 2003, levels above 100 indicate optimism, 100 neutrality and below 100 pessimism.

The Citigroup Economic Surprise Index measures the amount that economic activity surprised or disappointed relative to analyst expectations. It’s defined as weighted historical standard deviations of data surprises (actual releases vs Bloomberg survey median). A positive reading of the Economic Surprise Index suggests that economic releases have on balance beating consensus. The index is calculated daily in a rolling three-month window.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Institute for Supply Management (ISM) Non-manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms by the Institute of Supply Management. The ISM Non-manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© Charles Schwab

Read more commentaries by Charles Schwab