Turn the lights back off!

That may be what some investors are saying after the health care debacle, exposing the inner workings of sausage-making (oops, we mean lawmaking). At this point, we don't think the failure of healthcare reform meaningfully lessens the odds of tax reform. After licking its wounds, we think the administration and Congress will jump into the tax reform debate. Although we are optimistic about tax reform getting done, the process is likely to be complicated—especially if corporate and personal tax reform continues to be packed together (corporate reform and/or tax cuts are arguably the lower-hanging fruit). But Schwab’s team in Washington also cautions that the timeframe is likely later in 2017; which may mean tax reform is more of a 2018 economic and earnings story.

Brexit Begins

Arguably the most lasting political event occurring recently wasn't in the United States, as United Kingdom (UK) Prime Minster Theresa May triggered Article 50, beginning Britain's two-year withdrawal from the European Union (EU).

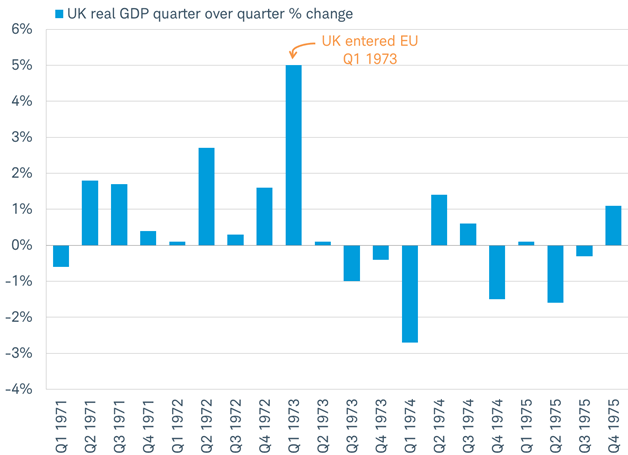

Article 50 has never been triggered before, so nobody really knows for sure how an exit from the EU will unfold or how long it may take for the UK to form new relationships. But it poses a risk for investors even in the near-term since the potential for major changes can have a negative economic impact. For example, when the UK entered the precursor to the EU in January 1973, the economy quickly slipped into a recession just four months later.

A recession quickly followed the UK entering the EU in 1973

Source: Charles Schwab, UK office for National Statistics data as of 3/29/2017.

The Bank of England (BoE), which is the UK's central bank, is going to stress test banks in the UK for what might happen if the Brexit goes badly. These tests include a sharp rise in inflation, interest rates, and unemployment during a period of a shrinking economy, reduced global trade and high levels of consumer debt. These are some of the worst-case outcomes that could come from a plunging currency and rising trade barriers. The BoE won't know results of the theoretical tests until the fourth quarter.

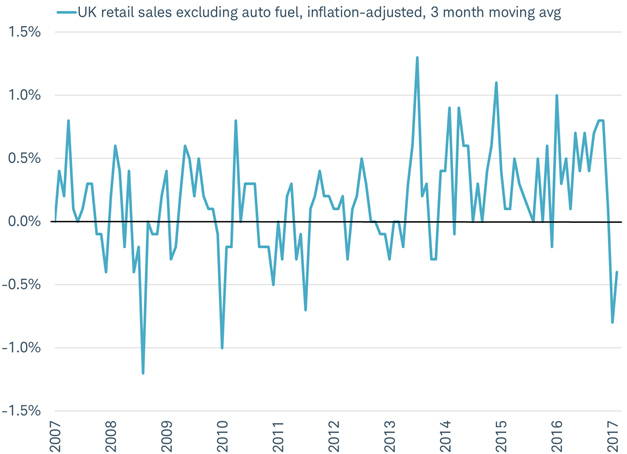

In the real world, we're already seeing UK households cut back their borrowing and spending as they prepare for the worst. We can see this in the big drop in inflation-adjusted retail sales this year, as you can see in the chart below. This could act as a major drag on the UK's first quarter gross domestic product (GDP).

UK consumers already pulling back?

Source: Charles Schwab, UK Office for National Statistics data as of 3/29/2017.

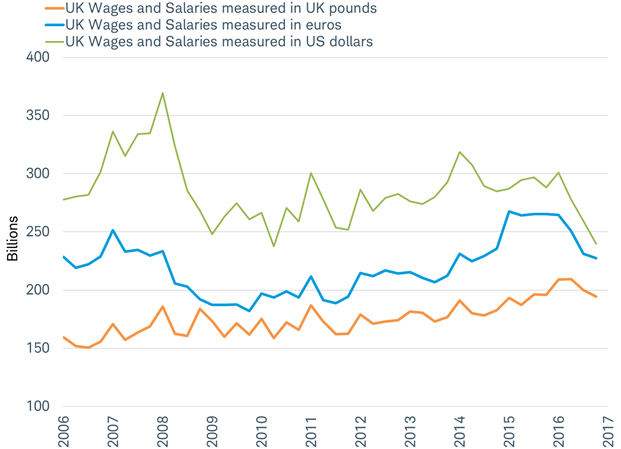

Also, inflation is jumping higher, with imports costing more after the 15% drop in the value of the British pound—and wages aren't keeping up, as you can see in the chart below. For example, measured in U.S. dollars, UK wages are the lowest in 10 years. Investors should keep an eye on the value of the British pound as a gauge of Brexit-related risk.

UK wages and salaries measured in different currencies

Source: Charles Schwab, Bloomberg data as of 3/29/2017.

The economic data bear watching, but markets also may react to the negotiations. Now that Article 50 has been triggered, we will be hearing about Article 218, which governs the terms of negotiation. The back and forth will likely influence how consumers and businesses assess the potential outcomes and adjust their behavior. It could lead to volatility in the markets.

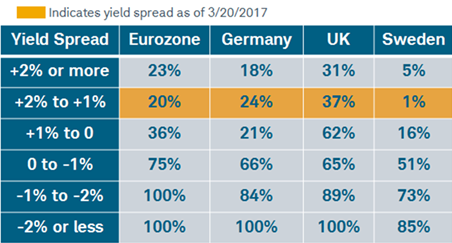

Fortunately, the worst-case scenario of a Brexit-induced recession and financial crisis is far from a sure thing. According to the UK yield curve (which measures the spread in yield between short-term and long-term UK government debt and has been a good forecaster of recessions in the past), the odds of a UK recession in the next 12 months are currently 30-40%, based on 50 years of history. So there's an elevated chance of recession, but it's not the base case. Investors should pay attention to changes to the yield curve; if short-term interest rates in the UK rise relative to long-term rates it would be a sign of deepening concern, and rising probability of a coming recession that could negatively affect global stock prices.

Yield curve-based prediction of recession in next 12 months by country/region

Historical time period begins: Eurozone 1970, Germany 1970, UK 1970

All yield spreads calculated as 10 year less 3 month.

Source: Charles Schwab, Macrobond data as of 3/20/2017

The latest polls show that only 29% of UK consumers think the economy will fare better after Brexit; that could mean a lot of pessimism is already reflected in consumer behavior and markets. Investors should stay diversified and invested according to their asset allocations—the most reliable indicators are telling us it isn't time for a more defensive stance. But we’ll be keeping a close eye on them as Brexit negotiations develop.

So what?

The recent pullback in stocks and failure of the ACA repeal appears to have helped take some of the froth out of the market and correct some overly optimistic sentiment conditions. We believe this will prove to be healthy for the continuation of the bull market, with an improving economy and a still business-friendly administration supporting further gains. But potential political-induced volatility isn't limited to the United States, as the official Brexit process started. A UK recession doesn't appear to be in the cards at this point, but risks have risen; while U.S. recession risk remains quite low.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Diversification and rebalancing a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The Consumer Confidence Index is a survey by the Conference Board that measures how optimistic or pessimistic consumers are with respect to the economy in the near future.

Leading Economic Index (Indicators) is an index that is a composite average of leading indicators and is designed to signal peaks and troughs in the business cycle.

Composite Index of 10 leading Indicators is an index that is a composite average of ten leading indicators in the US complied by the Conference Board. It is designed to signal peaks and troughs in the business cycle, generally known as the leading economic index (LEI). Components of the LEI include average weekly manufacturing hours, average weekly initial claims, new orders for consumer goods and non-defense capital goods, building permits and stock prices. Other components are indexes of supplier deliveries and consumer expectations, M2 money supply and the interest rate spread between 10-year Treasury bonds and federal funds.

The National Federation of Independent Business NFIB Small Business Optimism Index is compiled from a survey that is conducted each month by the National Federation of Independent Business (NFIB) of its members.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© Charles Schwab

Read more commentaries by Charles Schwab