Key Points

- Much of the pick-up in economic growth, as well as the earnings turn, pre-dated the election and shouldn’t be fully credited to President Trump.

- Growth has accelerated globally; while nominal growth in the United States is under-appreciated.

- Recent consolidation in stocks likely about sentiment having gotten a tad too frothy.

Trumponomics, the Trump Trade, the Trump Rally—and more recently Trumpocalypse—you've heard them all. Now you'll read a story (and perhaps hum a tune) about economic inflection points and a stronger stock market which may have had little to do with the results of the election. I'm not dismissing the impact on confidence readings of the hope for pro-growth Trump administration policies, but as we've been pointing out for several months, many of the fundamentals supporting stocks had their inflection points pre-election.

One of these things...

This week I broke from my long tradition of using rock song titles for my reports. But recently I recalled fondly a Sesame Street song from my childhood, with these catchy lyrics:

One of these things is not like the others

One of these things just doesn't belong

Can you tell which thing is not like the others

By the time I finish my song?

It popped back into my head the other day when I looked at this chain of charts:

Source: FactSet, The Conference Board, as of March 31, 2017.

Source: FactSet, The Conference Board, as of March 31, 2017.

Source: FactSet, National Federation of Independent Business (NFIB), as of February 28, 2017.

Source: Gallup Presidential Approval Center, as of April 1, 2017.

If all (or even most) of the improvement in the economy and stocks were attributed to the Trump election win, one would expect his approval rating to have received a bump. Clearly, that is the "thing not like the others."

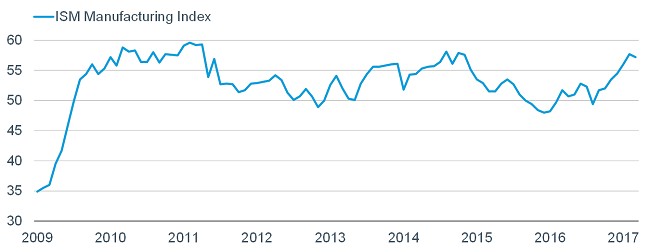

Data turn pre-dated election

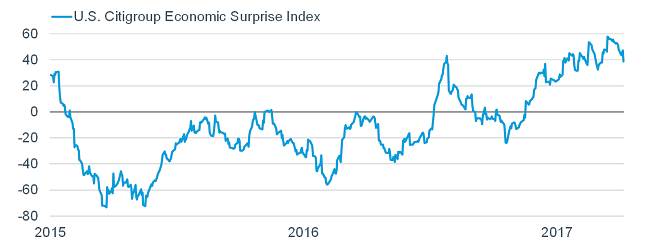

Although the spike in confidence readings post-dated the election, the turn in the ISM Manufacturing Index, as seen above, pre-dated the election. In fact, looking at high-frequency economic data more broadly, it began outperforming expectations in mid-October last year. The Citi Economic Surprise Index (CESI) measures how data is coming in relative to expectations, and you can see the inflection below.

Source: FactSet, as of April 7, 2017.

Although it's not always been the case, presently there is a high positive correlation between the CESI and stocks. In other words, the market has been cheering better-than-expected news, even if it means a faster pace of rate hikes by the Federal Reserve. Be mindful of the rolling over of the CESI however. It could be short-term, but estimates for first quarter gross domestic product (GDP) have weakened—the Atlanta Fed’s GDPNow forecast is now below 1%.

Not just a U.S. story

Further support to the notion that the market’s surge since early-November isn't solely (or perhaps not even largely) about Trump, is the fact that global growth has also accelerated markedly, as seen in data such as global PMIs, earnings and leading indicators. Even in France and Germany, where they await their contentious elections (about which my colleague Jeffrey Kleintop has written), French INSEE household and German Ifo business confidence are both higher recently.

What we've been witnessing has been the multiplier effect on the stock market of the massive amount of global central bank stimulus over the post-financial crisis years. In fact, although we don't have access to the data to show it in a chart, according to BCA Research, in spite of still-high global policy uncertainty, the sum of the Citi Global Economic and Inflation Surprise Indexes is just off the highest level in the 14-year history of the survey.

Nominal matters

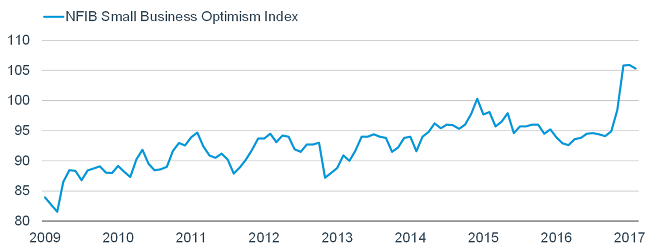

One force for the good of business confidence has been the expected uptick in nominal GDP growth. In years past, with inflation running at historically low levels, the spread between nominal and "real" (inflation-adjusted) growth was quite narrow. But with reflation kicking in, the spread is widening; meaning nominal growth is on the rise. Not only is NFIB small business confidence (seen in the chart above) more highly-correlated to nominal than real growth, corporate earnings are also more highly-correlated to nominal growth as they're reported in nominal terms.

As you can see below, after a four consecutive quarter earnings recession spanning the second half of 2015 through the first half of 2016, S&P 500 earnings have rebounded sharply...and should continue to do so through at least the end of this year. Clearly, that inflection point pre-dated the election.

Source: Thomas Reuters, Yardeni Research, Inc., as of April 7, 2017. 1Q17-4Q17 based on estimated earnings growth.

Power of inflections

I talk and write about inflection points a lot. As a leading indicator, stocks tend to start to move when economic/earnings data stops getting worse and starts getting better ... not after things are already better. It's why I often say "better or worse tends to matter more than good or bad" when it comes to the relationship between economic/earnings data and the stock market.

I believe the recent mild pullback/consolidation in stocks was driven less by Trump malaise and more by some sentiment froth which needed working off. We are likely to see another leg up for stocks courtesy of continued genuine improvement in the U.S. and global economy; not just on hope for or a bet on Trump and his pro-growth policies. To borrow a word from BCA, the market is unlikely to fall prey to the “Trumpocalypse” barring a new exogenous shock.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab

Read more commentaries by Charles Schwab