Key Points

- The long running bull market continues to show remarkable resiliency and we expect that to continue. However, risks have risen and a pullback is likely.

- The U.S. economy remains a mixed bag of slow trend-like growth with waning inflation pressures. But solid earnings growth should continue to support stocks.

- The threat of a sharp slowdown in China appears to have diminished but global tensions are still emanating from that region.

How long?

Are risks growing or will the bull market continue? We believe the answer to both is yes. Political bumbling, monetary policy shifts, and geopolitical tensions have all escalated, but the bull continues to power ahead, largely unscathed by the tumult that surrounds it. This is actually in keeping with history, as partisan conflict in particular has served as a contrarian indicator for stocks in the past. Since past performance is not an indication of future results, consider it yet another brick in the wall of worry. However, it's uncertainty around monetary policy that would likely be a culprit behind any coming choppiness in stocks.

The bull has had few detours

Source: FactSet, Standard & Poor's. As of July 18, 2017.

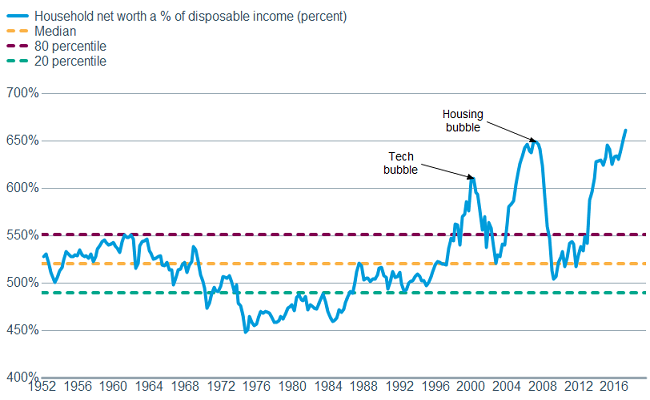

The aforementioned uncertainties have kept investor sentiment from becoming too frothy, which helps to support the ongoing bull market. We don't see signs yet of a "melt-up" scenario, where investors frantically rush into stocks, afraid they’re missing out on gains. As good as melt-ups feel while they’re underway, they don't end well. The possibility of a correction (defined as a greater than 10% pullback) is greater now than it was at the beginning of the year; especially given the uncharted territory in which the Federal Reserve finds itself, as it soon begins to unwind its $4.5 trillion balance sheet. We are modestly concerned about asset valuations that have soared in the era of artificially low interest rates and a bloated balance sheet.

Asset inflation reaching concerning levels

Source: FactSet, Federal Reserve Bank, Strategas Research. As of July 18, 2017.

We don't think the bull is ready to take a bow just yet, and at this point would view pullbacks as healthy. According to Strategas Research it has been 268 trading days since the last 5% pullback—the fourth longest streak since 1950 (the 1990s had two of them).

Earnings growth is the mother's milk of sustainable stock market gains and the next few weeks will go a long way to determine the status of corporate health. With one quarter down and another one in the process of being reported, it looks good, with the Thomson Reuters-reported consensus expecting at least a 10% year-over-year increase in earnings for 2017. What is more impressive is that the year's expectations have only been downgraded slightly from the 14% growth rate projected at the beginning of the year. To illustrate how solid that is, look back to 2016, when projections at the beginning of the year were for 13% annual growth in earnings. Those projections were steadily downgraded throughout the year before ending up with an actual growth rate last year of less than 2%.

Of course, a high expectations bar leaves open the possibility of disappointments, which could add to volatility in the coming weeks. Already we've seen major banks largely beat estimates but pull back on some concerns about some seasonally soft numbers—which arguably should have been built into expectations. And the energy sector's contribution to forward-looking expectations is already past its peak.

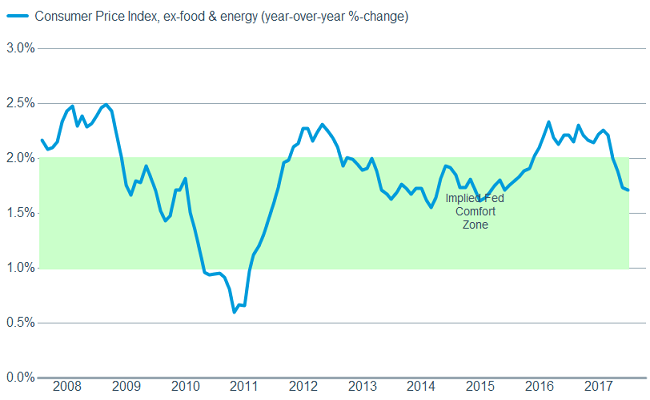

Economic data continues to confound

Another support for stocks may be coming from economic data that is showing a robust labor market, but few signs of inflation building. The unemployment rate is 4.4%, yet wage gains remain modest. The Consumer Price Index (CPI) was flat month-over-month, while ex-food and energy it only ticked 0.1% higher.

Source: FactSet, U.S. Dept. of Labor. As of July 18, 2017.

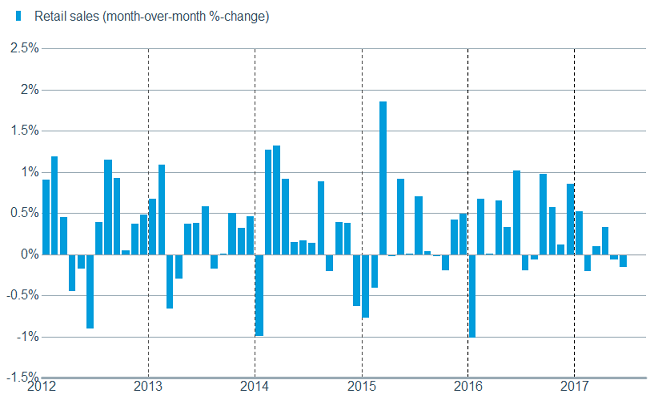

More concerning is the lack of solid increases in retail sales, although we believe the measuring process may be somewhat flawed due to the changing mix of sales. Nonetheless, it isn't particularly encouraging for an acceleration of economic growth when retail sales as reported by the Census Bureau were down 0.2%, and ex-autos and gas sales ticked 0.1% lower.

Retail sales continue to be tepid

Source: FactSet, US Census Bureau. As of July 18, 2017.

On the plus side, the latest industrial production reading provided by the Fed bested estimates by showing a 0.4% gain, while capacity utilization moved higher to 76.8%; heading in the right direction but still 3.3 percentage points below the long-term average. Also, after a sharp decline, the U.S. Citi Economic Surprise Index has started to turn around, which should be another support for the ongoing bull market in stocks.

Economic surprises have started to reverse course

Source: FactSet, Citigroup. As of July 18, 2017.

Fed seems confused, while politicians are befuddled

Economic uncertainty has confounded the Fed, which may raise the risk of a policy mistake and/or bouts of market volatility. In her testimony before Congress last week, Chairwoman Yellen indicated that the Fed is somewhat confounded by lower-than-expected inflation; citing "temporary" (and transitory) factors. She voiced no concern about elevated asset valuations, arguably brought on to some degree by the Fed's unprecedented monetary policy since the financial crisis. This put the potential for another rate hike this year into greater doubt. We're sticking with our forecast for one more hike this year along with the start of a gradual reduction in their balance sheet in their effort to "normalize" monetary policy; but also believe the latter could come before the former. However, Yellen also bolstered the doves' case by noting that it is becoming more apparent that the "normal" level of interest rates may be below what it had been historically.

Down the street…what can be said? Politicians continue to play politics. Behind the headlines some business friendly policies have begun to have some positive impact, such as a reduction in the regulatory burden. But the three biggies—health care reform, tax reform and infrastructure spending—all appear mired in the morass that is Washington. Business leaders are used to this sort of muck in Washington and have made few plans based on potential changes. But there is little doubt in our mind that if nothing gets done, there will be disappointment among businesses and investors alike, which could add another log to the pullback fire. Already we are seeing the subjective "soft" data (survey- and confidence-based) catch down to the weaker objective "hard" data, as we expected.

China's growth stabilizes

One potential danger spot may have diminished a bit as China released its second quarter gross domestic product (GDP) of 6.9% this past week. China is always among the first countries to report the performance of their economy and there is good reason to doubt the accuracy of the steady quarter-to-quarter official numbers. But the monthly data for June, some of it from more trustworthy sources, suggests that after some slowing, the pace of growth firmed up as the second quarter ended. That may have been due at least partially to help from government support in the form of infrastructure spending, and easier borrowing conditions evidenced by a drop in interest rates in June following a steep climb in one-year rates during the prior seven months.

After tightening credit conditions for seven months, China appeared to ease them in June

Source: Charles Schwab, Bloomberg data as of 7/19/2017.

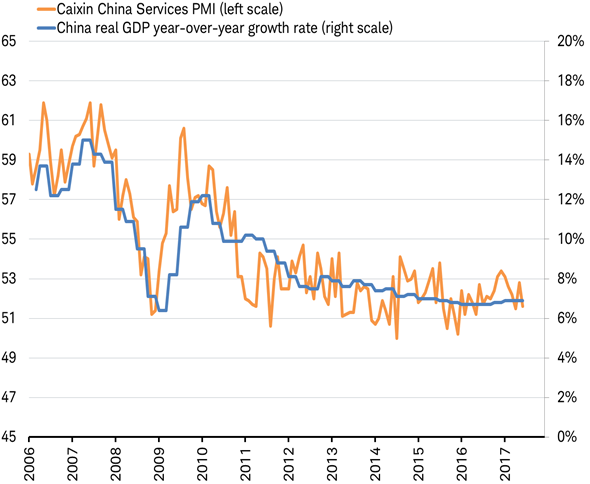

The firming in growth can be seen in most of the June data, including the manufacturing purchasing managers' index (PMI) produced by the private-sector, which stabilized at 50, rather than continuing to contract. The service sector PMI—which is most indicative of the pace of overall economic growth in China (as you can see in the chart below)—remained above 51 in June, signaling continued growth. To be sure, China’s growth rate continues to slow modestly, but June’s data suggest the risk of a rapid slowdown in the third quarter, with a negative spillover effect on global earnings, is less likely.

China’s service sector PMI reveals some of the volatility hidden in smoothed GDP data

Source: Charles Schwab, Bloomberg and Factset data as of 7/19/2017.

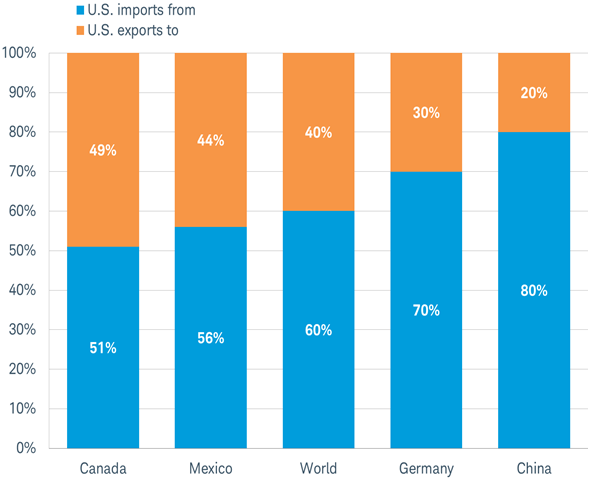

A meeting in Washington D.C. between trade representatives of China and the United States overshadowed the economic data this past week. The meeting followed the 100-day trade resolution agreed to in April as a further effort to reduce the trade imbalance between the two countries. The resulting concessions by China on opening up China's market to U.S. beef (for the first time since 2003), liquefied natural gas, and some financial services amount to a few successes for the Trump administration amidst a backdrop of little progress on key initiatives in Congress. But these developments will have little impact on balancing the $350 billion trade gap that extends from U.S. exports making up only 20% of total US-China trade, as you can see in the chart below. The United States and China have pledged to work together over the coming year on tougher issues which would likely include excess capacity in steel and aluminum in China, and the United States' refusal to sell high tech products to China that could have military applications.

Out of balance: 2016 trade balance with the United States by country

Source: Charles Schwab, International Monetary Fund data as of 7/19/2017.

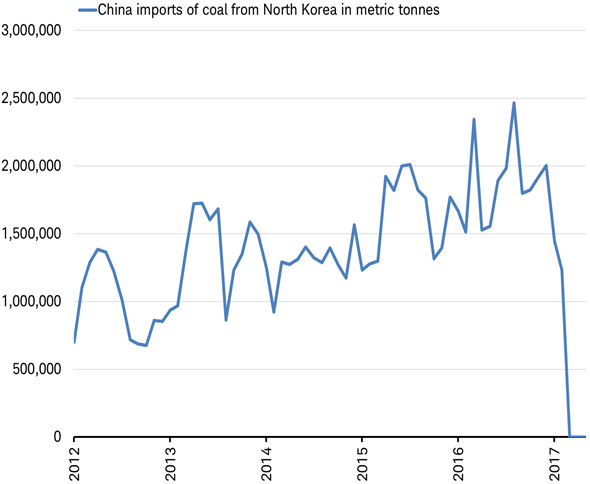

The United States could threaten sanctions, but wants China's help with diffusing the North Korea nuclear threat. China is using trade measures, such as halting coal imports (as you can see in the chart below) as a tool to manage, but not resolve, the situation. Almost 90% of North Korea's exports go to China, and coal makes up about half of those exports.

China has reported no imports of coal from North Korea for three months

Source: Charles Schwab, Bloomberg data as of 7/19/2017.

Given China's trade efforts and the offer for talks with North Korea by South Korea's new administration—combined with several U.S. naval carrier strike groups having left the Pacific in the past two weeks—it appears that an imminent military strike is unlikely. But a long-term solution is equally unlikely given that the regional security situation has not changed enough to force aggressive actions by North Korea’s neighbors. The advancement in North Korea's missile range, to potentially extend it to U.S. territory, is a major change for the United States; but Seoul has long been within range of North Korea’s heavy artillery and China has long contended with a nuclear armed India, Pakistan, and Russia on its borders. The result is most likely an occasional rise in tensions, accompanied by trade moves by the United States targeting Chinese firms that do business with North Korea and China's ongoing trade curbs on North Korean exports; but a near-term military confrontation remains unlikely in our view.

So what?

A solid earnings season should contribute to a continuation of the bull market in stocks. Dangers are lurking, however, and the possibility of a decent-sized pullback has grown over the past couple of months, in light of monetary policy and geopolitical uncertainties. While we would likely view such a move as healthy, it can be disconcerting. Stay diversified and be prepared to guard against overreacting to any such move.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Diversification and rebalancing a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The S&P 500 Composite Index is a market capitalization-weighted index of 500 of the most widely-held U.S. companies in the industrial, transportation, utility, and financial sectors.

The Consumer Price Index (CPI) Ex Food & Energy released by the is a measure of price movements by the comparison between the retail prices of a representative shopping basket of goods and services. Those volatile products such as food and energy are excluded in order to capture an accurate calculation.

The Citigroup Economic Surprise Index is an objective and quantitative measures, which show how economic data are progressing relative to the consensus forecasts of market economists.

The Shanghai Interbank Offered Rate (or Shibor), is a reference rate based on the interest rates at which banks offer to lend unsecured funds to other banks in the Shanghai wholesale (or "interbank") money market.

The Caixin China PMI, including the Caixin China Manufacturing PMI and Caixin China Services PMI, is compiled by Caixin Media and Markit, a provider of financial information services. The Caixin China Report on General Manufacturing is based on data compiled from monthly replies to questionnaires sent to purchasing executives in more than 420 manufacturing companies. The Purchasing Managers’ Index™ (PMI™) is a composite index based on five of the individual indexes: New Orders, Output, Employment, Suppliers’ Delivery Times and Stock of Items Purchased.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© Charles Schwab

Read more commentaries by Charles Schwab