Key Points

-

For tactical investors, we recommend a neutral weight to U.S. equities; but a bias therein toward large cap stocks.

-

"Beta bounce" has been like clockwork during this bull market.

-

Most secular trends point to large cap

outperformance; but

there are risks to the story.

Having recently upgraded our view on developed international markets (hat tip to Jeffrey Kleintop), we are now recommending investors keep their allocations to all three major equity asset classes—U.S., developed international and emerging markets—in line with strategic targets. We are maintaining our bias toward large capitalization (cap) stocks, within an otherwise neutral U.S. equity allocation. Today's report is an update on my thinking around the cap call.

Secular and cyclical trends

I like to think about markets in both a cyclical and secular framework. From a cyclical perspective, small cap stocks have made several impressive runs at sustainable leadership—and could continue to do so, especially if tax reform gains traction (they are likely bigger beneficiaries). But I think the secular winds are blowing in favor of large caps.

Cyclically, small caps are no longer trading at a trailing P/E premium to large caps, courtesy of recent strong large cap performance—especially within the technology sector. But on forward (full year 2017) estimates, small caps' P/E remains at a premium.

"Beta bounce"

The Leuthold Group does some of the best work on market valuations and cap biases, and I've been a student of their work for more than three decades. They recently highlighted small caps' "beta effect," in which more than all of small caps' historic outperformance has been earned during the first year of bull markets, as you can see in the chart below.

Source: The Leuthold Group. 1945-June 30, 2017. *Annualized spread, small cap minus large cap total returns.

In fact, the pattern has unfolded nearly perfectly during the current bull market. The "beta bounce" kicked in right at the March 2009 low, driving the Russell 2000 up 98% over the subsequent year (versus +72% for the S&P 500). While small caps eventually moved to a much higher "relative" peak by 2011, those excess returns evaporated by the onset of the 26% decline in 2015-2016.

Following that cyclical bear market, another powerful 12 month "beta bounce" kicked in off the February 2016 low. This pattern is one of several cyclical factors which drive the small cap leadership cycle; alongside interest rates, the yield spread, sector momentum, relative valuations, relative technical conditions, economic growth, government spending and the U.S. dollar. According to Leuthold, the "beta bounce" has been one of the more consistent of these factors.

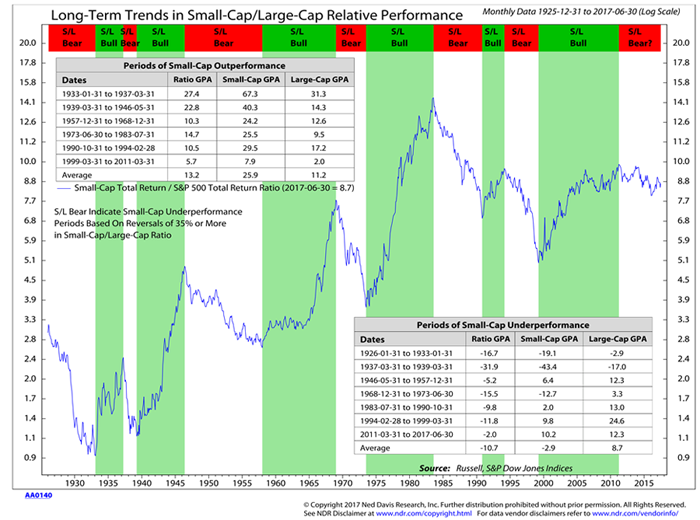

Lower highs, lower lows

Thinking longer-term, as you can see in the Ned Davis Research (NDR) chart below, the secular downtrend in small caps relative to large caps is becoming more established. Technically, the small/large cap ratio remains in a range of lower highs and lower lows. In fact, the small/large ratio has never gone this long (6.25 years) in between new highs during a small/large secular bull market.

NDR notes that one of the reasons U.S. economic growth has been so tepid since the recession ended is the "negative output gap" (the difference between actual and potential economic output). Since an improving economic backdrop favors large caps over small caps, the output gap has tended to narrow or become more positive during small/large secular bear markets. The output gap has climbed from a near-record low of -6.1% during the recession to -0.7% presently. Continued improvement would be a tailwind for large caps.

Another factor in favor of large over small is the yield curve, which has been largely flattening as the Federal Reserve has been raising short-term interest rates; but longer-term rates have been held down by low inflation. Historically, a flattening yield curve has been positive for large over small. But that, of course, brings up a risk to the large over small call. If the curve were to steepen, small caps could find some cyclical relative strength.

Another risk relates to government spending, which has been relatively flat as a share of gross domestic product (GDP) since 2011. While less government spending tends to support large over small, if spending begins to ramp up (without offsetting deficit reduction), it could also serve as a cyclical tailwind behind small caps.

Finally, a note on the middle child in this family. From a tactical perspective and for diversification purposes, investors should also keep an eye on mid-caps (range definitions vary by index provider). NDR has found that mid-caps have outperformed small caps in 100% of previous small cap secular bear markets.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab

Read more commentaries by Charles Schwab