A Cat and Mouse Fall

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Points

- U.S. stocks remain near all-time highs, but we expect some continued churn as fall is shaping up to bring a series of political, geopolitical and monetary policy conflicts which could contribute to greater volatility.

- Ample global liquidity, healthy economic growth combined with a solid earnings outlook should ultimately allow the bull market to continue.

- Global economic growth is looking good and is helping to fuel investor optimism over further gains in international stock markets.

The hits keep on coming

Americans are unbelievably strong and resilient but this is getting ridiculous. First Harvey and then Irma have left destruction in their wakes. The stock market impact has been relatively modest and in fact stocks rallied after Irma ended up being less destructive than feared—but the human impact is on a scale that is heartbreaking to us all. On the flip side, it has been heartening and a reminder to us all what a great country this is and how we come together when it matters to help those in need.

Historically, following major hurricanes, there has been a downtick in economic activity and a short-term surge in unemployment claims; while the subsequent quarter or two brought strength from recovery/rebuilding activity. There is a unique double whammy this year with back-to-back storms along with a tight labor market. This could limit the number of workers available to help in the recovery efforts (for more on the hurricane aftermath see Liz Ann's Trying to Reason with Hurricane Season: The Aftermath of "Harma")

While the hurricanes haven't had a major impact on the broader market, the continued cat and mouse game between North Korea and the United States has been a source of increased volatility. Risk aversion appears to rise every time the nation conducts a nuclear weapons test; before again settling down as investors place their faith in the hopes that cooler heads will prevail. We believe the odds of a full-scale military conflict are low and recommend that investors remain disciplined around their long-term asset allocations. In addition, seasonal tendencies are ostensibly not in the market's favor, with September having historically been the worst month on average for U.S. stocks, with an average return of -0.5% since 1950.

Growth vs. stagnation

Fundamentally, U.S. economic growth has picked up from the sluggish pace of the first quarter, while inflation remains subdued—the classic "Goldilocks" environment. We were encouraged by the uptick in both Institute for Supply Management (ISM) surveys in September, with the manufacturing index moving to 58.8 from 56.3 (new orders remained at a robust 60.3); and the non-manufacturing index rising to 55.3 from 53.9, (new orders rose to 57.1 from 55.1).

ISM surveys show continued economic expansion

Source: FactSet, Institute for Supply Management. As of Sept. 11, 2017.

We’ve also seen copper move higher, which tends to be an indicator of world economic growth and is sometimes referred to by the moniker "Dr. Copper" for its frequent historical predictive ability.

"Dr. Copper" points to an improving global economy

Source: FactSet, Dow Jones & Co. As of Sept. 11, 2017.

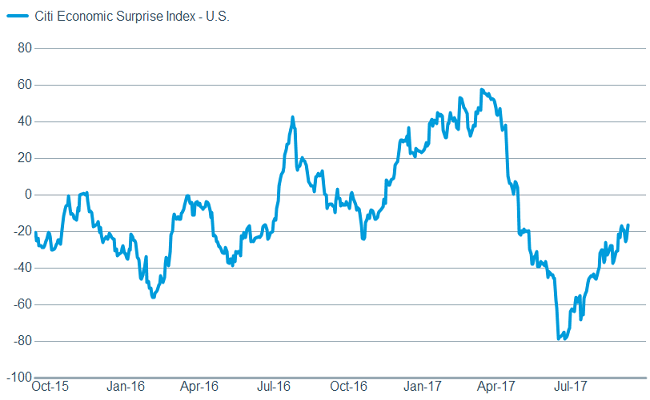

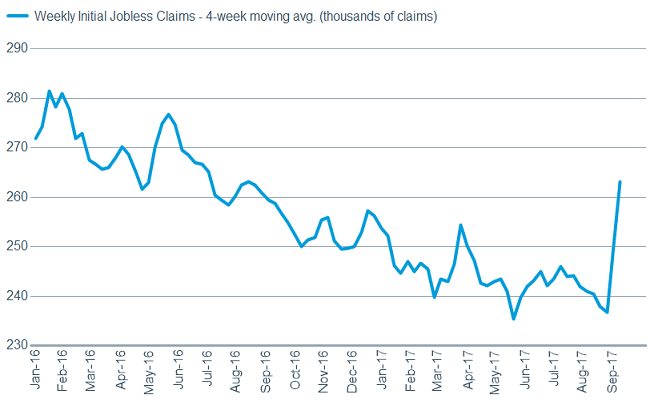

The rebound in the U.S. Citi Economic Surprise Index has also been encouraging, although it is likely to weaken in the immediate aftermath of the dual hurricanes. As we touched on, we've already seen a Harvey-related uptick in jobless claims—much as we did following Hurricane Katrina a dozen years ago—and more is expected in the wake of Irma. But in the past that phenomenon has proven to be relatively short-term in nature (fewer than eight weeks) and we expect that to be the case this time around as well.

Two areas of notable strength have been in small business optimism, which, as measured by the National Federation of Independent Business, has remained at extremely high levels all year; and job openings, which recently hit yet another all-time high. The labor market is unquestionably tight, which could mean wage gains are likely to pick up.

Encouraging but could see some near-term softness

Source: FactSet, Citigroup. As of Sept. 11, 2017.

Claims should temporarily rise post-hurricanes

Source: FactSet, U.S. Dept. of Labor. As of Sept. 11, 2017.

Source: FactSet, U.S. Dept. of Labor. As of Sept. 14, 2017.

Congress is back in session and we saw some bipartisanship as a deal was brokered to provide hurricane relief, while extending the deadlines for a budget deal and a debt ceiling increase until December 15. We are skeptical that this spirit of working together will result in any meaningful policy breakthroughs and concede that the can was again just kicked slightly down the road rather than providing longer-term certainty. As a result, we'll likely see continued fighting between the parties, with the tax reform debate taking center stage. Schwab's team in Washington believes the likelihood of getting tax reform accomplished during this calendar year is slim.

Hawks vs. Doves

The Federal Reserve is also playing their own internal cat and mouse game with some officials citing low inflation as a reason to delay further tightening; while others want to stay on the steady path toward normalization, due to the aforementioned tighter labor market. We continue to believe that the start to the slow winding down of the Fed's massive balance sheet will be announced this month; but that an additional rate hike before year end remains in question. We continue to believe the Fed's "quantitative tightening" (QT) could be the cause of some heightened volatility.

Excessive vs. Rational Optimism

Halfway through the month of September global stocks are on track to make it an 11th consecutive monthly gain, as measured by the MSCI All Country World Index; which would tie the all-time record for the index set in 2003-04.

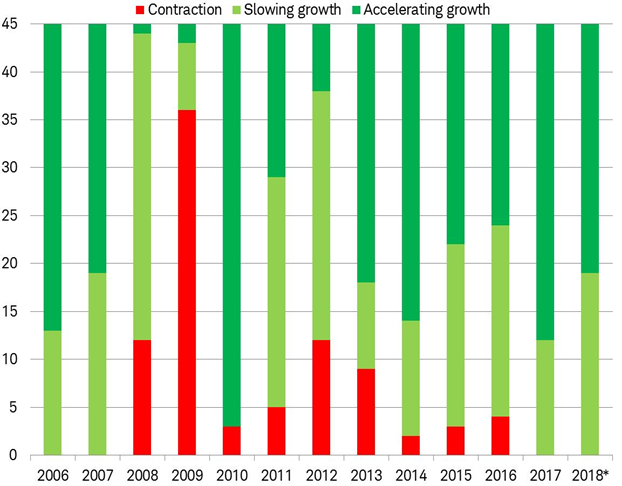

This exceptional string of gains begs the question: have investors become too optimistic about growth? We don't think so. Global economic growth has also been exceptional. Every one of the world's 45 largest economies tracked by the Organization for Economic Cooperation and Development (OECD) are growing this year and are expected to post another year of growth in 2018, per OECD forecasts, as you can see in the chart below. It has been 10 years since we last saw back-to-back annual growth for every major economy (2006-07). From 2008-2016 many of the world's largest economies experienced recessions, acting as a drag on corporate earnings growth and stock market performance.

Widespread growth among the world's largest 45 economies contrasts with the recessions of 2008-2016

Source: Charles Schwab & Co, OECD. *OECD forecasts for 2018, except 10 major non-OECD countries use Bloomberg consensus. As of 9/5/2017.

What you can also see in the chart above is that growth is actually accelerating in most of the world's largest economies in 2017. Leading indicators point to further acceleration in 2018, which should support continued stock market gains. These indicators include: the purchasing mangers' indexes (PMI), the OECD global composite leading indicator (CLI), and the developed market financial conditions index (FCI).

- PMI: 97% of countries have manufacturing PMIs above 50—the breakeven level between growth and contraction, as you can see in the chart below. The component of the global PMI that offers the best indication for future growth is the reading on new orders, which rose to a five-month high. The percentage of countries where new orders outpaced inventories rose to 100%, pointing to future growth.

Global growth is broad-based

Measures manufacturing purchasing manager indexes from 35 countries.

Source: FactSet, Markit, as of 9/8/2017.

- CLI: The OECD global Composite Leading Indicator, which includes 39 countries (33 OECD member countries and six major non-member countries), has increased on a month-over-month basis for 17 straight months.

Uptrend in leading indicator suggests growth continues

CLI measures OECD member economies plus major non-member economies (Brazil, China, India, Indonesia, Russia, and S. Africa).

Source: FactSet, OECD, as of 9/8/2017.

- FCI - Global financial conditions point to an improving backdrop for growth as they continue to improve in 2017, despite rate increases from the Fed, as you can see in the chart below. The FCI is not showing any of the signs of deterioration seen in 2007, the last time global growth was this strong.

*Morgan Stanley Developed Market Financial Conditions Index

Source: Charles Schwab, Bloomberg data as of 9/12/2017.

The stronger and broader pace of global economic growth is supporting faster earnings growth, a key support for stocks. In fact, earnings estimates for the MSCI AC World Index are poised to break through the $30 level, as described in our recent commentary Earnings May be About to do Something They’ve Never Done Before. While a pullback could happen at any time for any number of reasons, we believe the solid and improving backdrop of global growth would limit the extent of any pullback in both magnitude and duration as the global bull market continues.

September has historically been a tough time for stocks and there are multiple potential pitfalls to look out for this year as well. But economic and earnings growth—both domestic and global—continues to look healthy and we expect the bull market to continue. Remain globally diversified, but also disciplined around target asset allocations; and use any volatility for rebalancing purposes.

© Charles Schwab

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All