So where does that leave us? The term cautiously optimistic seems appropriate, although admittedly overused. With no shortage of pundits looking for a correction, it adds to the notion that the “wall of worry” stocks like to climb is still intact; notwithstanding the aforementioned bump up in optimism. Ultimately, we believe the next cyclical bear market will come when stocks begin sniffing out the next recession—likely still in the distance—and/or if the Fed is forced to tighten monetary policy more quickly than what’s currently baked into assumptions. In the meantime, our advice is to remain diversified and disciplined, and stay focused on long-term goals—not always exciting, but historically tends to be profitable.

Blame it on the weather

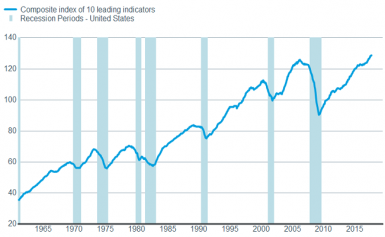

That focus on the longer-term is also good advice when dealing with some of the economic data that will be released over the next several months. Domestic data will likely be skewed to the downside over the next couple of months due to the triple threat of hurricanes; and then may get a temporary boost as the rebuilding and replacing cycle takes hold in the hurricane-damaged areas. Heading into hurricane season, the economy had been growing at decent clip, with second quarter real gross domestic product (GDP) recently getting revised up to 3.1%. And the leading economic indicators had been in a nearly-uninterrupted ascent.

Economy looked solid heading into the hurricanes

Source: FactSet, U.S. Conference Board. As of Sept. 25, 2017.

One issue that may impact the amount of positive influence we see from the rebuilding could be the tight labor market. The Job Openings and Labor Turnover Survey (JOLTS) report showed that job openings are at a record high of over six million; while the National Federation of Independent Business’ (NFIB’s) recent survey showed that their members’ second biggest concern was the quality of available workers, right behind taxes.

More workers needed?

Source: FactSet, U.S. Dept. of Labor. As of Sept. 25, 2017.

We will likely hear more about the effects of the hurricanes and the tightness of the labor market in the upcoming earning season. Key to watch will be whether traditional measures of wage inflation starts to take hold as some businesses try to lure away valuable employees with higher pay packages. In fact, less-traditional measures of wage inflation—like the Atlanta Fed’s Wage Tracker—already show more wage pressures building. More broadly, earnings season will be important for the bull market’s sustainability in light of the previously-mentioned high expectations bar, along with elevated valuations.

QT begins. Will fiscal stimulus take over?

As mentioned, stocks have been remarkable resilient, illustrated by the muted reaction to the announcement by the Federal Reserve of its start to shrinking its behemoth balance sheet. (Read more in Liz Ann Sonders article The Fed’s on the QT.) But that doesn’t mean that there won’t be some Fed-induced volatility in the fourth quarter. There remains the question of a potential December hike, which we believe is firmly on the table in light of the uptick in inflation along with the Fed’s stated intentions. And if inflation begins to kick in in earnest, it could push the Fed to be more aggressive than currently believed. The NY Fed recently released their new “Underlying Inflation Gauge” (UIG), which at 2.74%, is at least a full percentage point higher than either the Fed’s preferred core PCE measure of inflation or the core consumer price index (CPI).

On the other side of the Washington coin, expectations for positive action from Congress remain low, in spite of some enthusiasm emanating from the release of the tax reform blueprint. Remember, other than the first letter of both words, there is no comparison between a blueprint and an actual bill, and we don’t think a tax deal is likely this year. There was a great reminder from Politico upon the release of the blueprint: “Remember this: Six Republicans craft the tax blueprint behind closed doors. Now 535 lawmakers with opinions will have a say in the details. And thousands of lobbyists looking to protect their carve-outs will get in on the action.”

Market milestones

A resilient bull market is not just the United States’ claim. International stock markets are likely to reach three significant milestones in October:

- The 10th anniversary of the global stock market peak ahead of the global financial crisis.

- A potential breakout to a new all-time high for non-U.S. stocks after more than three years.

- A break of the previous record of 11 months in a row of gains for non-U.S. stocks.

In the weeks ahead we may see many articles published on this first milestone; but it may seem dated, since the 2007 global stock market peak was surpassed years ago. The second on our list is more timely, with non-U.S. stocks (measured by the MSCI All Country World ex-USA Index) now having rebounded to near their July 3, 2014 bear market peak, as you can see below.

Will non-U.S. stocks breakout to a new all-time high in October after recovering bear market losses?

Source: Charles Schwab, Bloomberg data as of 9/26/17. Past performance is no guarantee of future results.

The chart above reveals that the bear market and bull market both consisted of a similar number of index points and days; but the bull has not been a mirror image of the bear market. The oil-driven decline saw mixed economic growth with some energy-producing countries suffering recessions—such as Canada, Brazil, and Russia. In contrast, the more steady gains in 2017 have come amidst the broadest global economic growth in 10 years with no major economies in recession.

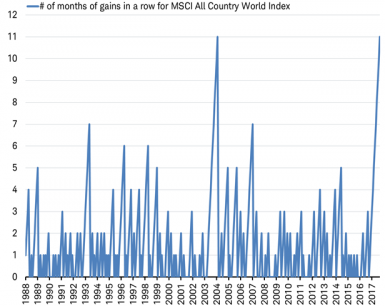

This steady rebound leads us to the third milestone. September marked 11 months in a row that global stocks have posted gains; tying the all-time record set as stocks first began to rebound from the "dotcom bust" in April 2003, as you can see below in the chart of the MSCI All Country World Index.

Will October break the record for consecutive monthly stock market gains?

Source: Charles Schwab, Bloomberg data as of 9/26/17.

With stocks approaching all of these market milestones at the same time, is October especially risky for investors? We don't think so. There is no reason markets would drop simply to mark a 10-year anniversary or end a streak only because a gain would set a new record. The truth is that milestones are often meaningless. In fact, plenty of milestones have come and gone without a change in the market's trend. For example, global stocks surpassed the peak of the 2011 bear market in early 2013, and then continued to post strong gains in the year that followed. Also, prior to the 11-month record of consecutive monthly gains, the longest streak was just seven months. There is nothing mystical about milestones.

While pullbacks are normal and can happen at any time, the fundamental trends that powered the steady rise in global stocks this year remain intact. The latest round of global leading economic indicators, including the preliminary readings of the September purchasing managers index for many countries around the world, point to continued economic strength that is lifting earnings and supporting the bull market.

So what?

The fourth quarter is typically an active one and we don’t think this one will be any different. Solid economic growth and good corporate earnings should allow the bull market to continue but we may experience bouts of volatility and/or pullbacks. Stay diversified and disciplined around your long-term objectives.

© Charles Schwab

www.schwab.com

© Charles Schwab

Read more commentaries by Charles Schwab