Key Points

-

U.S. business capital spending has already picked up; but an even sharper recovery could be in the cards for 2018.

-

Strong corporate profits and credit conditions are historically closely tied to the capital spending cycle.

-

Tax reform—if we get it—would be an additional kicker courtesy of the proposed 100% depreciation allowance.

It’s been referred to a period of secular stagnation, the post-debt supercycle, the new normal, among others. The U.S. recovery/expansion since the global financial crisis has left a lot to be desired with sub-par real gross domestic product (GDP) growth, disinflationary pressures, and anemic capital spending trends. Beneath the surface, there have been reasons for optimism that the stagnation was not a fait accompli; and now, those reasons for optimism have breached the surface. In particular, the pick-up in business capital spending (capex) is a relatively new bright spot for the U.S. economy; and in 2018 it will likely be a shining characteristic of the latter innings of an economic expansion.

Future capital spending plans surging

The official government-released measure for capex is “real nonresidential fixed investment,” which excludes residential housing from the mix (there is a separate “residential fixed investment” measure). As you can see in the blue line in the chart below, although it has turned up over the past year, it’s been largely range-bound since the initial surge out of the “great recession.” There are many leading and coincident indicators for capex, but one of the most closely-watched leading indicators—with a fairly tight historical correlation—is the Future Capital Spending Diffusion Index reported by the Federal Reserve Bank of Philadelphia.

Future capex plans surging

Source: FactSet. Fixed investment as of June 30, 2017. Future Capital Spending Diffusion Index (as of September 30, 2017) is part of the Federal Reserve Bank (FRB) of Philadelphia’s Manufacturing Business Outlook Survey and represents % of respondents indicating an increase minus those indicating a decrease in future capital expenditures over the next 6 months for reporting regional manufacturing firms.

Profits as prelude

Barring a breakdown in the historical ties between these two indicators, capex is set to pick up notably over the next year. Another important—and probably obvious—leading indicator for capex is corporate profitability. Over the past nearly 40 years, profit growth has led capex by about one year. Recall that U.S. corporate earnings—as measured by S&P 500 operating earnings—were in a (profits) recession for four consecutive quarters beginning in the third quarter of 2015 and ending after the second quarter of 2016. Since then, S&P 500 earnings have rebounded back into double-digit territory and look to remain there through 2018. Given the typical one-year lag, it’s a healthy set-up for a continued rebound in capex.

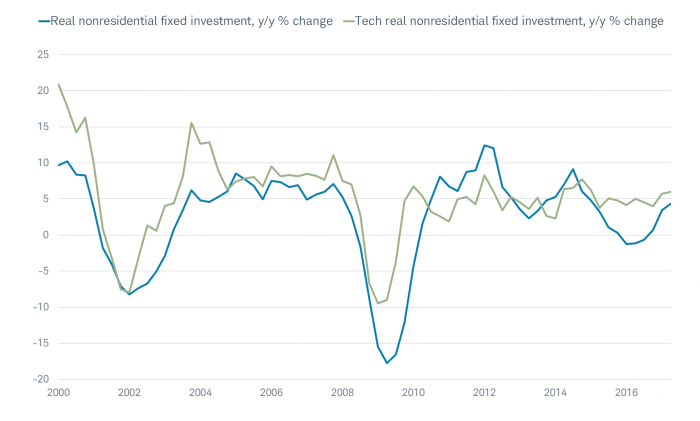

As highlighted in a recent BCA Research report on the subject, it would be unprecedented if the current business cycle ended without a visible capex upcycle. The past four recessions were all preceded by stock market-reported capex soaring to about a 20% annual growth rate. At the current juncture, capex is merely on the cusp of entering expansion territory. And, in keeping with the broad-based profits recession in 2015-2016, every S&P 500 sector went through a capex retrenchment period. In keeping with the outperform rating we have on the technology sector, we believe tech capex will be a particularly strong segment over the next year or so. As you can see in the chart below, whereas tech capex lagged overall capex for much of the 2010-2014 phase of the recovery, since then it’s been running stronger. We believe that is likely to continue.

Tech capex on top

Source: Bureau of Economic Analysis, FactSet, as of June 30, 2017. Tech fixed investment represents information processing equipment and software.

Global credit impulse

The credit cycle also favors a pick-up from today’s levels in capex. According to BCA, the reviving “global credit impulse”—courtesy of the Bank for International Settlements (BIS)—suggests that bankers will continue to extend credit and fulfill loan demand. This credit fuel should propel capex; or at the very least, remove a critical constraint to companies expanding their balance sheets. And the expected capex cycle is not just a U.S. phenomenon—synchronized growth among all 45 member countries of the Organization for Economic Cooperation and Development (OECD) should unleash a commensurately-synchronized global capex cycle.

Tax reform, please

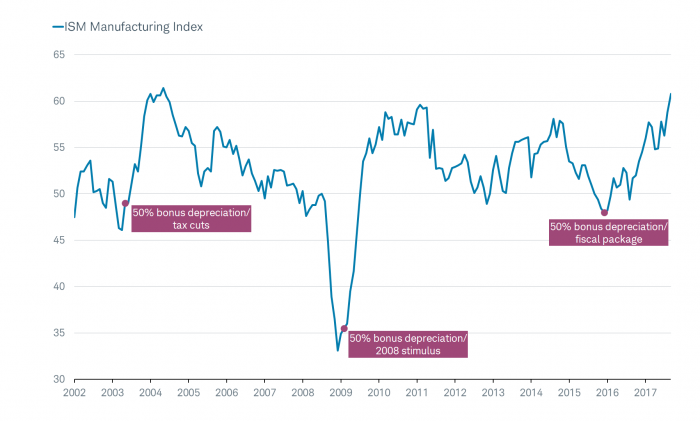

Finally, there is the tax reform framework—a component of which is the provision allowing companies to write off 100% of their capex purchases; which is likely to be a temporary provision, but retroactive to September 27, 2017. As highlighted by Strategas Research Partners, Congress passed 50% depreciation on a forward-looking basis three times in the past 15 years: May 2003, February 2009 (temporarily upped to 100% in 2010) and December 2015. As you can see in the chart below, after all three times, the ISM manufacturing index surged. Caveat: the ISM manufacturing index is already at a “boom” level, so I would not expect much more from this level.

Depreciation leads ISM

Source: FactSet, as of September 30, 2017.

More broadly, the Treasury Department looked at the impact of a 25% corporate tax rate, a 10% capital gains and dividends tax rate, and the expansion of tax-free accounts; all relative to 30% bonus depreciation, to see which encouraged more investment per dollar of revenue cost. Treasury found that 30% bonus depreciation produced the greatest impact; so full expensing should provide an even greater benefit. Caveat: this is provided the tax reform framework eventually becomes a bill—the runway between the two remains long. I served on President Bush’s nine-member bipartisan tax reform commission in 2005, so I learned firsthand that getting from a framework to a bill is not easy.

Long runway

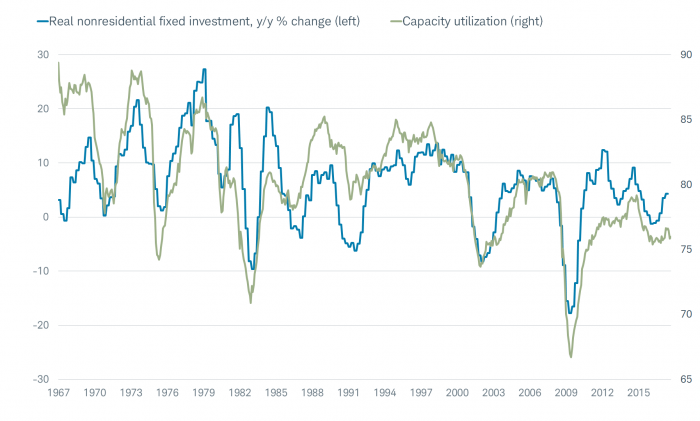

Speaking of runways, the runway for gains in capex remains fairly long. Capacity utilization remains fairly anemic, as you can see in the green line in the chart below. If you look at prior capex peaks, you’ll see a much higher average for capacity utilization—86.2% on average for the past five capex peaks. In other words, a lot more capex can be supported by capacity utilization and I expect the latter to start to play catch-up to the improvement in the former.

Still plenty of runway for capacity utilization

Source: FactSet. Fixed investment as of June 30, 2017. Capacity utilization as of September 30, 2017.

I still regularly get questions from investors about why this cycle’s capex trends have been sub-par to past expansions. Perhaps because it’s nascent, but it’s time for optimism about a significant capex cycle unfolding as we look ahead to 2018.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(1017-7WLO)

© 2017 Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab