Key Points

-

Global growth and earnings have been the market’s drivers; but tax reform has represented a more recent kicker.

-

Could we be setting up a “buy the rumor, sell the news” environment, especially if earnings forecasts don’t deliver?

-

Stocks, especially large caps, actually do well as the yield curve flattens.

Perhaps it’s premature (or even a jinx) to mention that if the S&P 500 ends December in the green, it will be the first time in history that U.S. stocks—as measured by that index—were up during every one of the 12 months. The only other year that came close was 1995, which saw a tiny drop of 0.4% in October. Incidentally, this year is most highly correlated to 1995 of all years since the S&P 500’s inception, according to Bespoke Investment Group (BIG). For what it’s worth, 1995 was followed by another strong year in 1996—up 23% for the S&P 500.

Growth the driver; tax reform the kicker

Two of the most important drivers of stocks’ ascent this year were synchronized global growth and strong corporate earnings. The prospects for tax reform have been a more recent kicker—and also the proximate cause for the sharper sector rotations we’ve seen lately. Following September’s tax reform hope-fueled surge, investors have been doing more homework with regard to the prospective winners and losers at the corporate level—rewarding those companies and industries which sit at the highest end of the effective tax rate spectrum.

In September, investors’ somewhat knee-jerk reaction to elevated expectations for tax reform was to buy up small-cap stocks—believing they were generally bigger beneficiaries (not necessarily the case). Since then though, small caps have experienced renewed underperformance as investors have been doing more precise homework on tax reform’s winners and losers. We are maintaining our bias toward large caps over small caps given the valuation premium at which the latter are still trading. In my mind, it begs the question of why investors would want to pay a premium for a weaker earnings profile. You can see distinctly weaker earnings growth as you move down the cap spectrum in the table below.

Source: The Leuthold Group.

Earnings boost ahead?

The data above is for earnings already in the book. As we have noted throughout the year, the vast majority of analysts and/or economists have not yet incorporated tax reform into either their corporate earnings or gross domestic product (GDP) forecasts. As such, one could claim that the best is yet to come as estimates for 2018 have yet to be adjusted upward. I don’t want to pull the punch bowl away before the year-end partying has even begun, but some detail is warranted.

The consensus estimate for the effective tax rate for S&P 500 companies, in aggregate, is somewhere between 26-27%. In theory then, a drop to 21% would be significant; and likely a major boost to corporate earnings. And the expensing provision should boost already-robust business capital spending next year. However, Ed Yardeni at Yardeni Research has been crunching the numbers in more detail lately and has some important findings.

The Fed’s data on nonfinancial corporations (NFCs) shows an average effective corporate tax rate of only 21.6% over the four quarters through this year’s third quarter. It’s been around 21% since early 2010, which is obviously well below the statutory rate of 35%. That is consistent with what the IRS has reported for corporate tax revenues. The Republicans’ tax plan lowers the statutory rate to 21%, while eliminating the deductions that have allowed companies to lower their effective rates.

But as Ed Yardeni opines, the “initiative might be to simplify tax accounting for NFCs and to give them a greater incentive to keep their headquarters and operations in the U.S. However, it might not boost after-tax corporate earnings as much as we and others have assumed.”

Buy the rumor, sell the news?

So, what if the assumed boost to earnings doesn’t materialize? Are valuations so stretched, and/or is investor sentiment so enthusiastic, that we might be in a “buy on the rumor, sell on the news” environment heading into 2018? The short answer is that we do think there is some risk of that in the near-term; however it would be in the context of an ongoing secular bull market.

We often try to educate investors about the relationship between valuation and stock market returns. When using traditional price/earnings (P/E) ratios, history shows that there is virtually no correlation between the market’s P/E and how the market performs over the subsequent year. The net is that it might be detrimental to your investment health to avoid stocks simply because they’re overvalued.

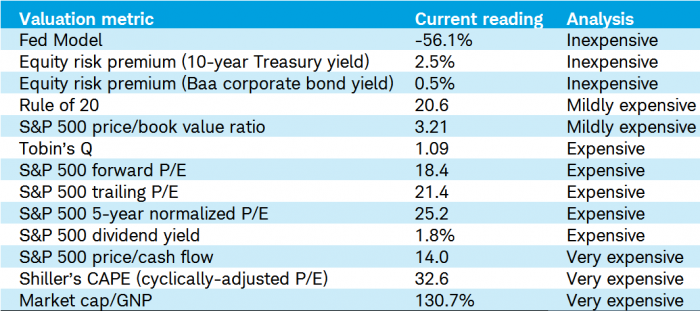

Valuation runs the gamut

There are myriad metrics which can be used to value stocks individually; or the market overall. It’s admittedly difficult to decide which valuation metrics are the most relevant at any point in time. I keep a running tab of 13 of them—some of which are quite common, and others likely less well-known. As you can see in the table below, I’ve arrayed them in descending order, from those which declare the market to be inexpensive to those which declare the market to be extremely over-valued. The metrics at the top are interest rate- and/or inflation-based; and given today’s still-easy financial conditions, stocks still look fairly reasonably-priced.

Source: FactSet, The Leuthold Group, Ned Davis Research, Inc. (Further distribution prohibited without prior permission. Copyright 2017© Ned Davis Research, Inc. All rights reserved.), Standard and Poor’s, as of December 15, 2017.

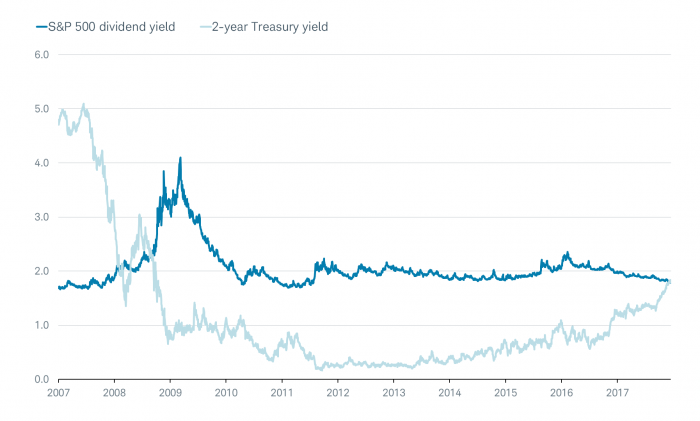

But I want to call out one metric in particular—the S&P 500 dividend yield. I was fooling around with a number of charts and data points last week, and had my research assistant put together a simple chart comparing the 2-year U.S. Treasury yield to the S&P 500’s dividend yield, as you can see below. Just last week, the former moved above the latter for the first time in about a decade. So I decided to Tweet the chart (@lizannsonders).

2y Yield > S&P Dividend Yield

Source: FactSet, as of December 15, 2017.

Twitter frenzy around yield comparison

Little did I know the attention the chart would generate on Twitter. It’s been retweeted and “liked” more than any other of the 3,730 tweets I’ve sent out since I got on Twitter a few years ago. My friend Jason Trennert at Strategas Research Partners wrote about this indirectly last week in a research post. He’s been calling the environment in which we’ve been investing since the financial crisis “TINA” (there is no alternative). What’s meant by that acronym is that investors have been forced out the risk spectrum and into equities due to the paltry yields offered on safer fixed income securities. Last week, Jason added an “A” to TINA; because “there is now an alternative” (TINAA), with even shorter-term government debt now yielding more than stocks.

This may not be a major game changer, but it does represent a shift in the landscape. As yields have been moving up on the short end of the curve, they’ve been “stickier” on the longer end; hence the flattening in the yield curve. My chart tweet elicited a number of replies about the perceived peril for equities of shorter-term yields moving up more quickly than longer-term yields. Not so fast.

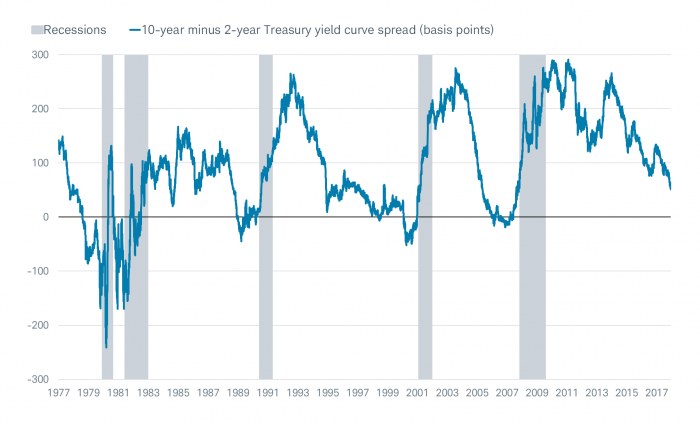

A simple chart of the “2/10” yield curve (spread between the 10-year and 2-year yields) is below.

2/10 Yield Spread

Source: FactSet, as of December 15, 2017.

Stocks like flatter yield curves … really, they do

Indeed, it is the case that every recession was preceded by an inversion of the yield curve (when the 2-year yield is higher than the 10-year yield). But lest you think that’s cause for worry at this stage, do note that there remains a decent amount of runway between the current spread (53 basis points) and an inversion. It’s also the case that there was typically a decent amount of runway between inversions and the beginning of recessions.

Importantly, it’s actually the case historically that the S&P 500 has performed best when the yield spread is between 0-50 basis points. According to BCA Research, since 1988, both the average and median return for the S&P 500 in that range is above 20%. So, a little more flattening in the curve would actually put us in the “sweet spot” for stock market returns.

And to tie that up with a little bow, a flat slope of the 2/10 curve has been a poor setting for small cap excess performance. Small caps underperformed large caps nearly 80% of the time when the curve was flat historically. In fact, a flat curve has been the least attractive climate for small cap excess returns—even poorer than when the curve inverted historically.

In sum

We believe we remain in a secular bull market and the runway between now and real trouble for either stocks or the economy remains relatively long. However, for reasons including the possibility of a “buy on the rumor, sell on the news” period around the likely passage of tax reform—and the possibility it doesn’t boost earnings growth significantly—some bumps along the runway should be expected.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

©2017 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab