Key Points

-

Stock markets have behaved much differently in the last two months as compared to the previous year. Increased volatility, however, doesn’t mean the end of the bull market, but it is becoming a more challenging environment.

-

The U.S. economy shows few signs of slowing down but risks to growth are rising as trade issues emerge and the Federal Reserve continues its tightening campaign.

-

The global wall of worry has a few more bricks in it, but positive news should help markets continue to climb that wall, although trade protectionism remains a threat to global growth.

Like flipping a switch

“A picture is worth a thousand words.”

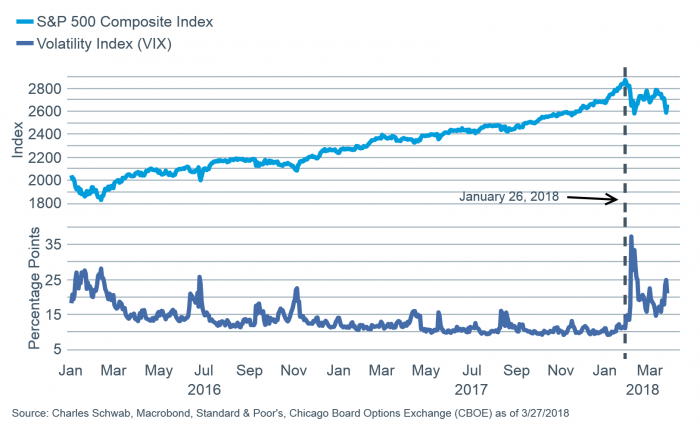

Changing environment

Past performance is no guarantee of future results.

Those two pictures show what’s happened better than words ever could—a swift change of market character since late-January. The market that let negative news just roll off its back is now more sensitive to ongoing political turmoil, White House personnel shakeups, tariff announcements, data breaches, etc. But as we’ve noted, last year was the exception; this year is closer to the norm. Sticking with a long-term plan is typically harder to do when the market isn’t going straight up. But, ironically, this is probably a healthier investing environment which could help keep the bull market alive. Valuations, which were quite extended as we entered 2018 have had the chance to retreat somewhat—courtesy of both the correction in prices, but also the strength in earnings. Additionally, sentiment conditions as measured by the NDR Crowd Sentiment Poll had gotten to record optimistic levels, but have now corrected back to the neutral level. Both of these developments are worth cheering, but unlikely to keep continued volatility at bay (with some bunny-like tendencies likely—discussed below).

Risks are rising

With the announcement of steel and aluminum tariffs and the more recent tariffs of up to $60 billion on Chinese imports, trade war concerns are elevated. At this point we believe the evidence suggests that the situation won’t deteriorate from a trade spat to a trade war, as both Canada and Mexico are exempted from the steel and aluminum tariffs; while FactSet is reporting that the United States is continuing to negotiate exemptions for the European Union and Australia—not exactly the mark of a trade war. But the risk is there that has clearly unnerved some investors (see Liz Ann’s Trade Mistakes: Will a Trade Spat Turn Into a Trade War article for more). Additionally, problems with personal data by Facebook brought forward the prospect of more government regulation on the tech sector in general and the social media space more specifically. While there is probably a place for some form of regulation, the tendency of government has often been to overreach and impact growth negatively, so it’s something to definitely watch in the coming weeks and months. The tech sector’s fundamentals still look quite good to us and we look at this pullback/correction as an opportunity to add to positions as needed. Finally, add on the Federal Reserve meeting that had a slightly more hawkish tone (see Kathy Jones’ article Fed’s March Meeting: Another Hike, More Hawkish Tone) and there are plenty of risks suddenly emerging to shake the confidence of investors. But another way to look at these increased risks is a rising Wall of Worry—which is often what stocks like to climb in a bull market.

But many positives remain

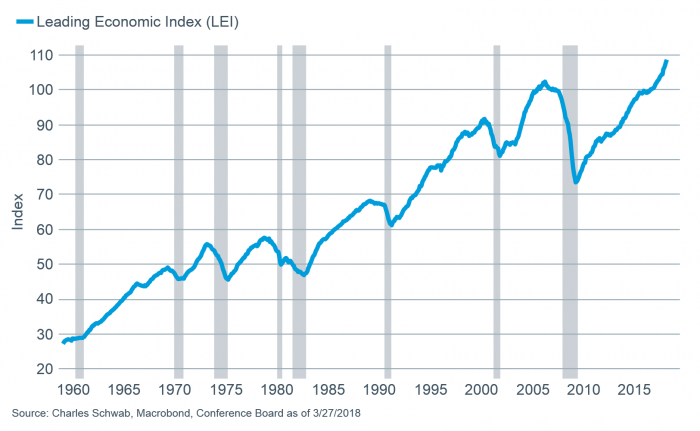

Corrections are always unnerving, especially because they tend to be processes over time as opposed to condensed moments in time. Traditional stock market fundamentals remain supportive of an ongoing bull market. The U.S. economy doesn’t look to be anywhere near a recession, which have historically accompanied bear markets. The Index of Leading Economic Indicators rose again in March, continuing a robust uptrend.

LEI indicates no near-term recession

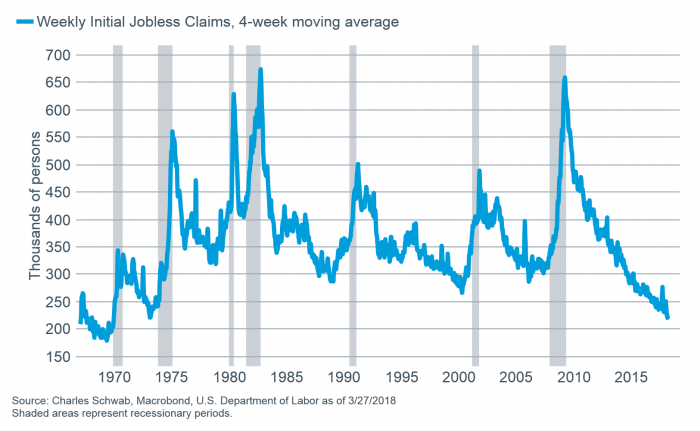

These leading indicators include initial unemployment claims, which recently hit a 45-year low.

Claims also indicate strength

But after all of the noise of the past several weeks, it may be the upcoming earnings season which represents the most important “tell” for investors. This publication coincides with the end of the first quarter and earnings season is just around the corner. According to Thomson Reuters, the estimated first quarter year-over-year growth rate for S&P 500 is 18.5%, which would be the highest rate of growth in seven years. That’s a pretty high bar to reach, but judging by the optimism shown in recent readings from the Institute of Supply Management, the National Federation of Independent Business, and The Conference Board’s CEO Confidence Survey, it should be a pretty optimistic tone coming from much of the corporate sector.

Don’t forget Washington—the positive side that is

It’s easy to focus on the negatives coming out of Washington, and for good reason, but at times we can lose sight of the positives. The U.S. economy should have a tailwind that is just beginning due to the tax cuts that the majority of Americans are just now incorporating into their budgets. Additionally, we can put worries of another government shutdown to bed, as a new spending bill—the merits of which can certainly be debated—passed , which should add to near-term economic growth. Down the street, the Federal Reserve continues to tighten policy, while the new Fed Chair Jerome Powell handled his first press conference with ease. The Federal Open Market Committee (FOMC) indicated a continued steady pace of hikes alongside an upward move in its summary of economic projections—all of which should be beneficial in the near term to stock markets. Caveat: the timing of fiscal stimulus—coming much later in the cycle than is typically the case—does elevate the risk that inflation heats up, which could push the FOMC to tighten more quickly.

Global Bunny Markets?

It’s not just the United States which is suddenly dealing with increased concerns. Stock markets around the world have reacted negatively to what is, for now, a small risk of a trade war—global companies making up the MSCI World Index earn more than half of their sales from international trade. Fortunately, we haven’t seen a trade war in over 90 years for a lot of good reasons, including:

- The legacy of economic destruction they caused in the 19th century

- Increasing globalization

- Longer supply chains

- The World Trade Organization (WTO) dispute resolution process.

The result has been that tariff changes in recent decades have been modest, narrowly-focused, and short-lived. As mentioned above, we believe the current trade spats are unlikely to develop into a trade war. However, the U.S.-China trade negotiations and announcements over the coming weeks may persist in causing volatility disruptions.

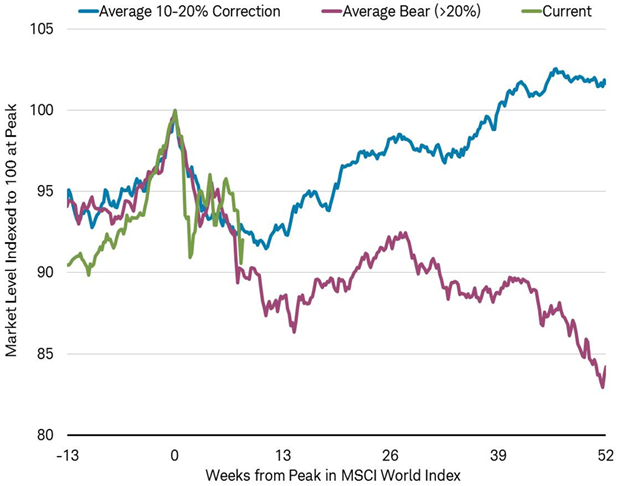

This probably isn’t the start of a bear market, but it doesn’t “feel” like a bull market right now—it’s more of a “bunny market,” as the jittery stock market hops up and down. But that behavior isn’t unusual after a pullback. In fact, based solely on prices, it’s too soon to tell if this is a cyclical/non-recession bear market or just a bull market correction. In either case, stocks tend to bounce around before re-establishing a trend, as you can see in the chart below of past bear markets and corrections in the MSCI World Index since 1979.

Too soon to tell?

Source: Charles Schwab. Bloomberg data as of 3/27/2018. Past performance is no indication of future results.

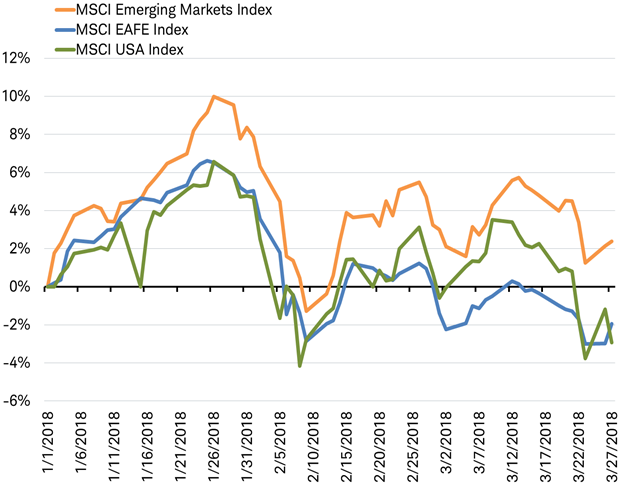

Of course, trade fears are not the only reason global stocks have been weak. If the concerns were just trade-related, it is likely that emerging market stocks would be underperforming developed market stocks, given their heightened sensitivity to trade growth. However, since the market peak on January 26 of this year, the MSCI Emerging Market Index has fared a little better than the basket of developed market companies that make up the MSCI USA and MSCI EAFE Indexes, holding onto a gain for 2018, as you can see in the chart below.

Emerging markets faring a little better than developed markets so far in 2018

Source: Charles Schwab, Bloomberg data as of 3/28/2018. Past performance is no indication of future results.

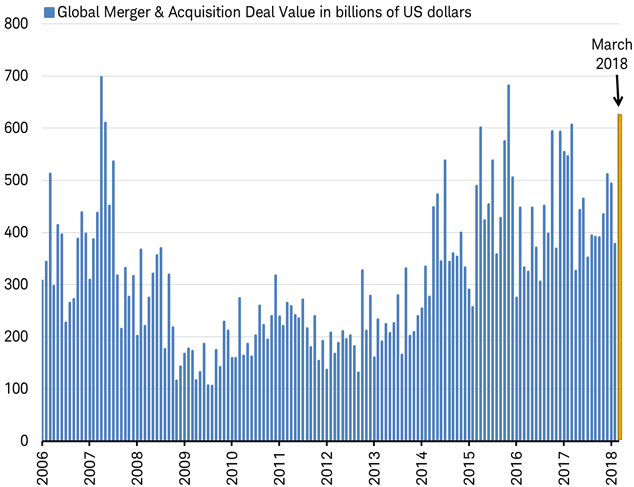

While buying by market participants seems to have pulled back in March, strategic corporate buyers have stepped up as deals have multiplied. As of March 27, announced global merger and acquisition deals totaled $626 billion for the month, making March 2018 the third-biggest month ever for M&A deals, as you can see in the chart below. While these deals were likely in the making for some time, market turbulence didn’t stop deals from being announced, implying that business leaders’ outlook remains positive as earnings continue to climb.

Corporate buying surged in March with M&A deal value for the month the third highest ever

Source: Charles Schwab, Bloomberg data as of 3/28/2018.

There are a variety of factors affecting the markets; including worries over global trade and the potential for increased regulation in the tech sector, balanced by the confidence seen in robust M&A activity and expectations for double-digit earnings growth for the first quarter. We expect the bunny market to continue hopping around in the weeks ahead, as it encounters these factors.

So what?

Sharp moves and stocks continuing to flirt with correction territory have been the hallmarks of the market lately. While unnerving at times, we continue to believe the economic and earnings environment should support a continuation of the bull market, albeit with more volatility, some elevated risks, and “bunny-like” behavior in the near term. We continue to espouse the benefits of periodic and disciplined rebalancing to take advantage of this volatility, along with reasonably long time horizons.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The S&P 500 Composite Index is a market capitalization-weighted index of 500 of the most widely-held U.S. companies in the industrial, transportation, utility, and financial sectors.

The Chicago Board of Exchange (CBOE) Volatility Index (VIX) is an index which provides a general indication on the expected level of implied volatility in the US market over the next 30 days

Leading Economic Index (Indicators) is an index that is a composite average of leading indicators and is designed to signal peaks and troughs in the business cycle.

Ned Davis Research (NDR) Sentiment Poll shows perspective on a composite sentiment indicator designed to highlight short- to intermediate-term swings in investor psychology.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Institute for Supply Management Non-manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms' purchasing and supply executives, within 60 sectors across the nation, by the Institute of Supply Management (ISM). The ISM Non-Manufacturing Index tracks economic data, like the ISM Non-Manufacturing Business Activity Index.

The NFIB small business optimism index is compiled from a survey that is conducted each month by the National Federation of Independent Business (NFIB) of its members,

CEO Confidence Survey is conducted, analyzed and reported by the Conference Board, and it seeks to gauge the economic outlook of CEOs, determining their concerns for their businesses, and their view on where the economy is headed.

MSCI World Index captures large and mid-cap representation across 23 Developed Markets (DM) countries. With 1,642 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country..

MSCI Emerging Markets (EM) Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.

MSCI USA Index is designed to measure the performance of the large and mid cap segments of the US market. With 626 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in the US.

MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Index consists of the following 22 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab