Key Points

-

With all the focus on tariffs, trade, and the FAANG stocks; lost among those headlines is perhaps a more important fundamental reversal in financial conditions.

-

The blowout in LIBOR-OIS is technical in nature; but higher funding costs and tighter liquidity conditions still have market implications.

-

Volatility is not leaving the building anytime soon.

The cost and availability of credit directly affects the supply and demand dynamics of the stock market. Tightening financial conditions alongside tighter monetary policy have been less-discussed reasons for heightened volatility and weakness in stocks this year; but they will remain an important fundamental backdrop for equities. This report will step away from the headlines around tariffs, trade, and the FAANG stocks; and look more broadly at the important change in the character of the economic environment as it relates to financial conditions and stocks.

Tighter credit, timeless implications

We live in a globalized world—more so now than ever before—and are emerging from an era of unprecedented global monetary policy intervention. This makes the cycle more complicated than ever before; however, tighter credit conditions have relatively timeless implications. One thing appears a certainty: U.S. total debt levels are at record highs, and as a result, it’s worth considering whether even a mild increase in interest rates will hurt the economy via increased debt service costs.

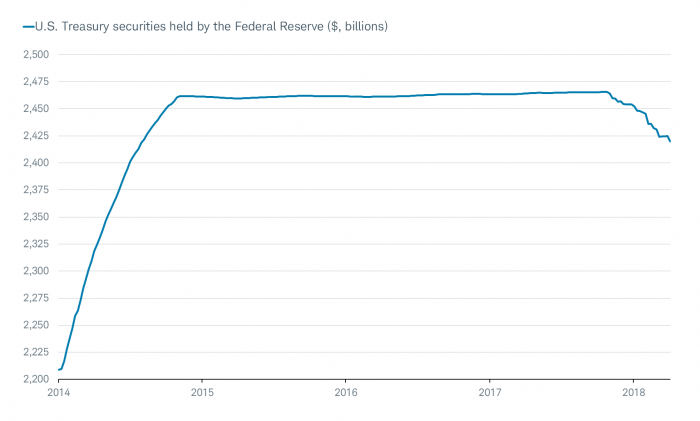

Not only are short-term interest rates on the rise courtesy of a Federal Reserve which has been hiking rates since December 2015; longer-term rates are generally rising as well. With the former rising faster than the latter, the yield curve has been flattening over the past year (more on that in a bit). But liquidity is tightening via other channels as well—including the shrinkage in the Fed’s balance sheet, which began last fall. The chart below shows the drain to-date for just the Fed’s Treasury holdings (excluding the drain also underway of its mortgage-backed securities).

The Great Balance Sheet Shrink

Source: Charles Schwab, FactSet, as of April 6, 2018.

The balance sheet shrinkage program is in its third quarter of operation, with the run-off in Treasuries currently capped at $18 billion/month. But in the first quarter of this year, according to TS Lombard, there were two weeks when the combined liquidity provision of the Fed and the European Central Bank (ECB) was negative, because the Fed’s balance sheet shrank more than the ECB’s expanded. And it’s expected that by the end of this year the ECB will finish its quantitative easing (QE) operations, making liquidity contraction the norm instead of the exception.

LIBOR-OIS blowout

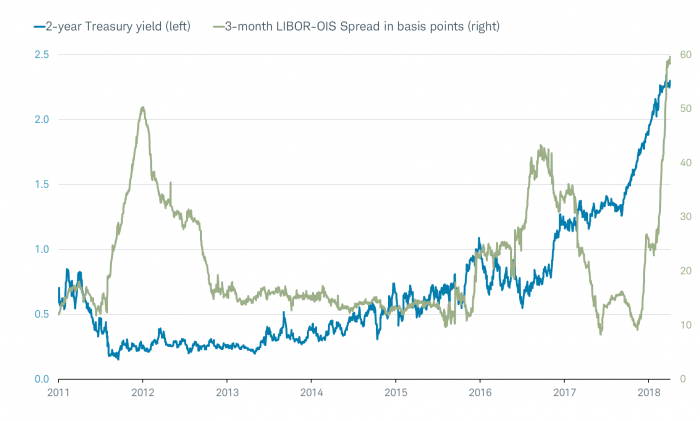

In direct relation to the Fed’s six increases in the fed funds rate so far this cycle, the 2-year Treasury yield has been rising. At the same time, the three-month London interbank offered rate (LIBOR) has been rising rapidly; with its premium above the overnight index swap (OIS) rate approaching 60 basis points (as you can see in the chart below)—the highest since the end of the last recession. The spread is a measure of how cheap or expensive it is for banks to borrow. It offers a look at how the market is viewing credit conditions, because it strips out the effects of underlying interest rate moves—which are affected by central bank policy, inflation and/or growth expectations.

LIBOR-OIS Blowout

Source: Charles Schwab, Bloomberg, as of April 6, 2018. LIBOR (London Interbank Offered Rate) is the interest rate at which banks offer to lend funds to one another in the international interbank market. OIS (overnight indexed swap) is a fixed/float interest rate swap where the floating leg is computed using a published overnight index rate.

The increase in the LIBOR-OIS spread is somewhat “technical” in nature—reflecting both increased Treasury issuance to fund the burgeoning deficit in the wake of fiscal stimulus; and the tax-related repatriation of funds by companies from overseas, which drains U.S. dollar funding that’s available among foreign banks. Although the spread was a leading indicator of previous funding crises—like during 2011’s Eurozone debt crisis—we are currently not seeing other spreads blow out, which is somewhat comforting.

Financial conditions are tightening

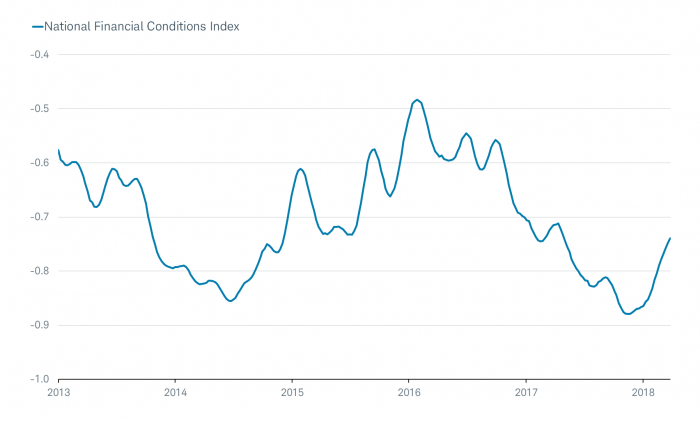

The blowout in LIBOR-OIS is yet another sign of tightening financial conditions—the Chicago Fed’s National Financial Conditions Index version of which is shown below. Tighter financial conditions, with a lag, do affect the equity market—while higher equity market volatility is also a contributor to tighter conditions. In the table below the chart you can see how the stock market has performed historically (since 1973) in three key zones of financial conditions. We have not yet broken out of the loosest zone, but the trend is important.

Financial Conditions Getting Tighter

Source: Charles Schwab, FactSet, NDR Research Inc., as of March 29, 2018. The Chicago Fed's National Financial Conditions Index (NFCI) provides a comprehensive weekly update on U.S. financial conditions in money markets, debt and equity markets and the traditional and “shadow” banking systems.

Interestingly, financial conditions were actually tightening heading into the Fed’s first rate hike in December 2015; since when (until recently) they’ve been loosening. One of the implications of tighter financial conditions is that investors generally become more discerning, which leads to more frequent sector rotations and lower sector correlations (which means diversification matters more).

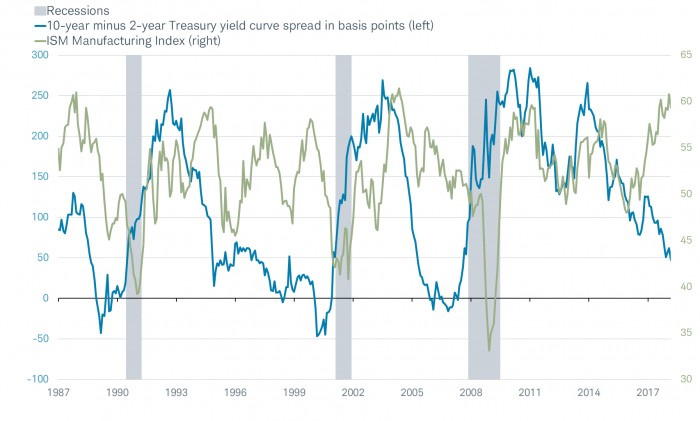

Yield curve signals?

Earlier in the report, I mentioned the flattening yield curve. With increasing frequency I’ve been hearing concerns from our investors about whether it is signaling slower growth ahead or even a heightened risk of a recession. The reality, at this stage, is that it more likely just reflects the ongoing “normalization” of policy by the Fed. As was the case in much of the 1990s, a flatter curve can persist for extended periods without causing serious trouble for either the economy or the stock market.

In fact, if you compare the direction of the yield curve (in this case the spread between the 10-year and 2-year Treasury yields) to one of the most important leading economic indicators—the ISM manufacturing survey—you will see an important divergence in the chart below. Not only is the yield curve still in positive territory, its flattening has not been accompanied by deterioration in the ISM survey. Notice divergences like this were fairly common during the expansion in the 1990s. The notion that the current flattening portends economic doom are misplaced—an inverted curve, not a flattening curve, tends to signal recession (and typically after the inversion). The near-record high still in the ISM survey supports this view.

Yield Curve and ISM Sending Divergent Signals

Source: Charles Schwab, FactSet, as of March 29, 2018.

That said, the strength in the ISM survey, along with other leading economic indicators, does point to the possibility that longer-term interest rates still have more room to run on the upside if they’re going “reconnect” with the trajectory of the economy (see chart below). Of course, economic skeptics might suggest the spread could narrow by the ISM and/or other leading indicators retreating.

Will 10y and ISM Reconnect?

Source: Charles Schwab, FactSet, as of April 6, 2018.

Speaking (ok, writing) of the 10-year Treasury yield, it’s worth noting that it’s up a bit since the stock market correction began in late-January; which is distinctly different than what occurred during the prior eight pullbacks/corrections of 7% or more during the current bull market. In fact, the last four stock market corrections of at least 10% were accompanied by bond yield declines ranging from 50 to 150 basis points.

Well put by The Leuthold Group: “To some extent, then, these corrections proved self-medicating: Falling stock prices forced yields to decline, providing another dose of stimulus to the economy while at the same time reducing an already-low hurdle rate for investors. Just beware that the bull’s secret medication for longevity (i.e., self-medication) is not currently available. And a bull that’s ‘off its meds’ sometimes exhibits not only change in character, but a change in species as well.”

In sum

Higher rates, tighter financial conditions and the blowout in the LIBOR-OIS spread likely don’t represent individually or collectively systemic risks to the economy or the stock market; but they are clearly a symptom—as is higher equity market volatility—of a wider rerating of credit. For now, more banks are actually seeing rising loan demand according to the Fed’s Senior Loan Officers Survey, while lending standards and terms remain favorable, including for small business loans. However, as has been our mantra since we put together our 2018 outlook late last year, volatility is likely to remain high this year and investment discipline remains essential.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

©2018 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab