Key Points

-

May has generally been good for U.S. stocks, although the major indexes still remain within recent ranges. We believe the bull market will continue, but the increased volatility seen earlier this year is likely to reemerge.

-

U.S. economic data has shown signs of rebounding from its first quarter weakness; and while the expansion is extended in terms of time, it’s less extended in terms of “temperature” (not over-heating).

-

Recent economic signals from international markets are less encouraging, but remain supportive of likely modest international stock market gains.

“A hero is someone who has given his or her life to something bigger than oneself.”

- Joseph Campbell

Summertime cheer?

Happy Memorial Day Weekend everyone. A relatively strong May for stocks may have investors wondering if they should shun the traditional “Sell in May and go away” mantra. Trying to time the market is rarely a winning strategy and we never advocate trying to catch a potential seasonal downturn. It’s also a midterm election year, and those have historically been accompanied by larger market swings and greater maximum drawdowns; not to mention the ongoing geopolitical uncertainties. Case in point would be the announcements by President Trump that the summit with North Korea has been cancelled and possible tariffs on imported cars and trucks being considered. In addition, the summer is vacation season, with overseas investors taking extended ones, which can lend itself to lower volumes and the potential for more pronounced swings.

The rally since the March lows has pushed investor sentiment higher, with the Ned Davis Research Crowd Sentiment Poll moving back into optimistic territory, a potential contrarian indicator. In addition, corporate earnings season has wound down, eliminating a tailwind of good news associated with tax and regulatory reform.

Economic expansion not on oxygen yet!

According to the National Bureau of Economic Research (NBER), the current economic expansion is now 106 months old—making it the second longest expansion in the past 100 years—and well above the average of 58 months—leading to much “latter innings” discussions But remember, expansions don’t die of old age alone—they typically die from excess; in the form of inflation, monetary policy, capacity utilization, etc. So, while the length of the current expansion is extended, economic gains haven’t been. According to Yardeni Research, real gross domestic product (GDP) has grown about 22% from the 2009 trough, well below the 50%-plus gain at the high end; and the second-lowest gain in any expansion since 1960.

After the typically-weaker first quarter growth rate for the economy, we’ve seen a pickup in the data for the second quarter. Regional manufacturing surveys such as the Empire and Philadelphia Fed surged in May, with the former moving from 15.8 to 20.1, while the latter spiked from 23.2 to 34.4. Additionally, retail sales staged a bit of a comeback, with the Census Bureau reporting that April sales rose 4.7% over the year ago period, with the previous two months being revised higher.

Retail sales looking good

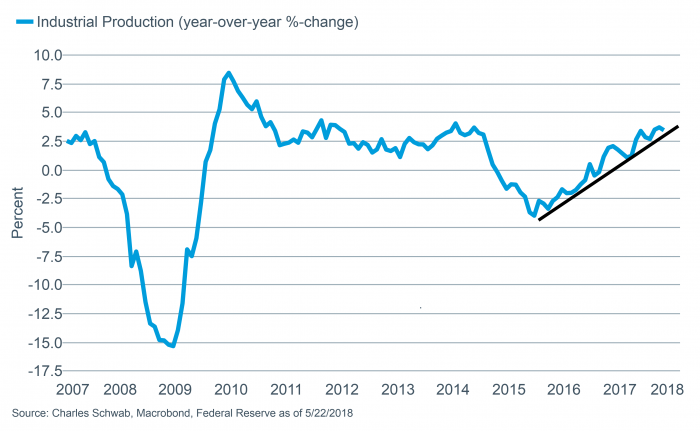

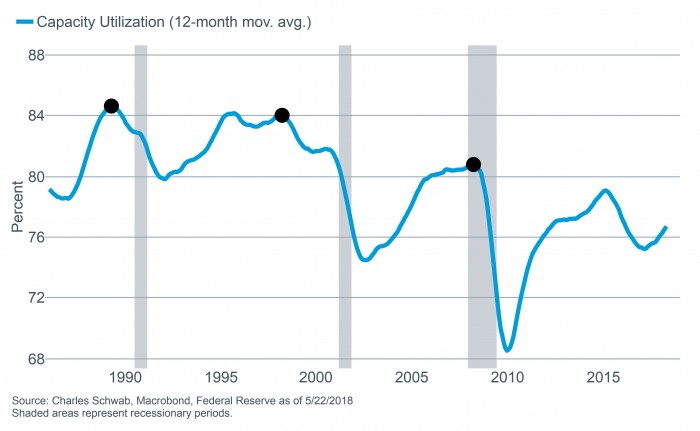

Industrial production also surprised on the upside, with the Federal Reserve reporting a 0.7% increase, while capacity utilization ticked higher to 78.0% from 77.6% (but notably remaining below the 80% level that both indicates capacity constraints and a level that has typically been reached in advance of a recession).

Industrial production continues to rise

While capacity utilization indicates expansion has room to run

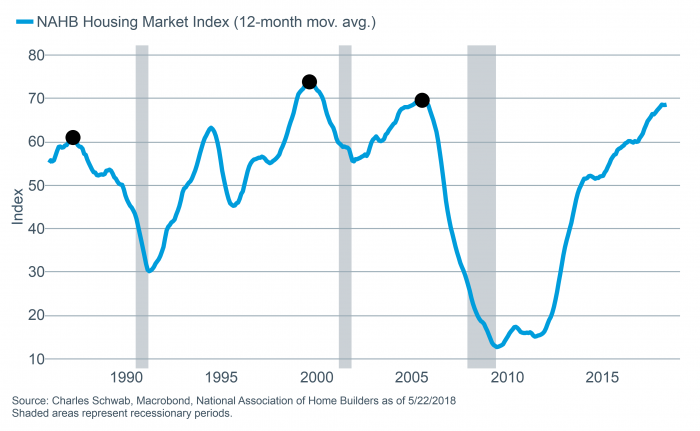

Likewise, housing has rebounded but not sharply and the National Association of Realtors continues to bemoan lack of inventory, while the National Association of Homebuilders Confidence Index rose to 70 from 68—showing no signs of the sharp declines seen in the advance of previous recessions. (For more see Liz Ann’s article Long Train Running: Leading Indicators Show Little Risk of Recession ).

Builder confidence remains high

But risks remain

The economic expansion appears to have some legs but there are certainly risks that could short-circuit continued growth. A possible trade war remains at the top of the list, with negotiations on multiple fronts ongoing. Some take comfort in ongoing talks, but we’re going to need to see some progress in the next several months or the risk of damaging trade policy being enacted could escalate. As far as the June “summit” between the United States and North Korea being called off, the market’s reaction was swift, but fairly mild at this stage.

On a more fundamental level, escalating inflation alongside tightening financial conditions remain more relevant risks to the bull market. Markets are taking some comfort from the recently-released Fed meeting minutes, which highlighted that the Federal Open Market Committee (FOMC) would be comfortable with a “temporary period of inflation modestly above 2%” in keeping with its view about “symmetry” (allowing for a somewhat symmetrical period of above-target inflation in light of how long inflation was below target). But there remains a risk that the Fed could end up behind the curve and having to tighten more quickly if inflation accelerates more sharply

Global stocks and economy reconnecting

The signals for a potential global economic acceleration aren’t quite as encouraging. The preliminary Purchasing Managers Indexes (PMI) from around the globe for May were released this week. They are the earliest read on May economic activity in a wide range of countries and are closely watched by investors following the economic soft spot seen earlier this year.

The global PMI (a combination of the PMIs of over 30 countries) slid in February and March due in part to some temporary factors, then stabilized in April with a slight rebound. May appears to have brought an erosion in that rebound based on the preliminary reports released this week. The current PMI reading points to a solid, but no longer accelerating, pace of global economic growth.

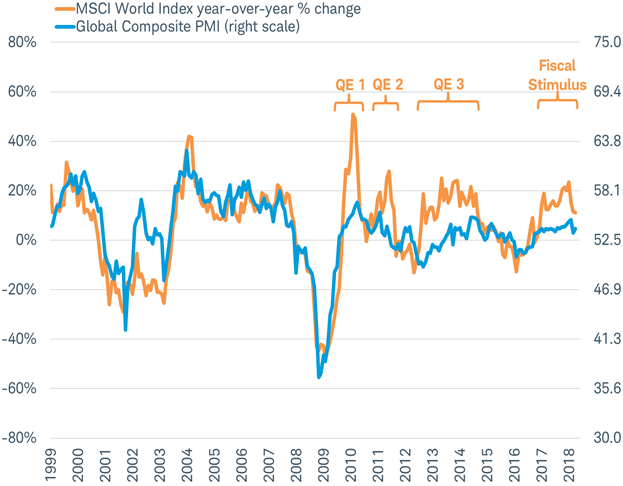

Why is the PMI so closely watched? As you can see in the chart below, stock market performance (in orange) and the global composite PMI (in blue) have generally tracked each other over the past 20 years since the inception of the PMI. Global stock market performance has rarely disconnected for long from the underlying trend in the global economy measured by the PMI.

Another temporary disconnect between global stocks and economy may be reconnecting

Source: Charles Schwab, Bloomberg data as of 5/21/2018. Past Performance is no guarantee of future results.

The orange and blue lines appear to be reconnecting, as they have done three times already this cycle. The three times the lines disconnected were after the Federal Reserve’s quantitative easing (QE) programs ended. Although those bond buying programs appeared to do little to lift global economic performance as measured by the PMI, the monetary stimulus did lift stocks resulting in temporary disconnects between the performance of stocks and the economy during the duration of those programs.

In 2017, rising expectations of fiscal stimulus bolstered investor optimism and pushed global stock markets higher. That wave of optimism seems to have waned with the enactment of fiscal stimulus (the tax cuts in the United States) in January. Since January, stocks again appear to be moving toward reconnecting with the economic growth environment measured by the PMI.

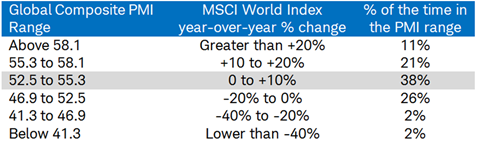

Historically, a reading on the global PMI of between 52.5 and 55.3 has been consistent with single-digit annualized global stock market gains, as you can see in the table below. The current reading is near the center of that range. If there was no change in stock prices or the PMI, the orange (stocks) and blue (PMI) lines would reconnect in September as year-over-year stock market performance would tend to moderate into the single digits. Alternatively, if the PMI rebounds or if stocks pullback 5%, the lines could reconnect more quickly.

PMI range and stock market performance

Grey shaded row marks current environment.

Source: Charles Schwab, Bloomberg data as of 5/21/2018. Past performance is no guarantee of future performance.

While it may seem disappointing to see a slide in the PMI, the global stock market correction since January accompanying the slide in the global PMI has meant that global stock market performance no longer appears to be widely disconnected from economic fundamentals. This suggests to us that while volatility is likely to persist, the economic environment would tend to support modest stock market gains rather than the correction turning into a bear market.

So what?

First and foremost, we remember and honor those who have paid the ultimate price for the freedom that we enjoy in the United States—and enable us to worry about such things as the market and not our survival. Second, summer and midterm elections can bring volatility, meaning investors should focus on discipline and diversification. The economy looks healthy and earnings growth has been stellar, but investors also need to be mindful of setting the expectations bar too high. Have a wonderful holiday weekend.

Important Disclosures

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date.

Diversification of a portfolio cannot assure a profit or protect against a loss in any given market environment.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Ned Davis Research (NDR) Sentiment Poll shows perspective on a composite sentiment indicator designed to highlight short- to intermediate-term swings in investor psychology.

The Empire Manufacturing State Index is a regional, seasonally-adjusted index published by the Federal Reserve Bank of New York distributed to roughly 175 manufacturing executives and asks questions intended to gauge business conditions for New York manufacturers.

The Philadelphia Fed survey is an indicator of trends in the manufacturing sector, and is correlated with the Institute for Supply Management (ISM) manufacturing index, as well as the industrial production index.

The National Association of Homebuilders (NAHB) – Wells Fargo Housing Market Index (HMI) is based on a monthly survey of NAHB members designed to measure homebuilder sentiment in the single-family housing market. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes. It is a weighted average of separate diffusion indices for these three key single-family series.

Purchasing Managers Index – The global PMI is an indicator of the economic health of the global manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment

The MSCI World Index captures large and mid-cap representation across 23 Developed Markets (DM) countries. With 1,648 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

© 2018 Charles Schwab & Co., Inc, All rights reserved.

© Charles Schwab

Read more commentaries by Charles Schwab