Key Points

-

Job growth remains strong and the unemployment rate ticked up for “good” reasons.

-

Historically, as the (lagging) unemployment rate has declined, so has the pace of returns for the (leading) stock market.

-

The skills gap remains wide; and qualified job switchers’ wage gains are outpacing job stayers’ wage gains.

“Quality is much better than quantity. One home run is much better than two doubles.” Said once by Apple’s Steve Jobs, it’s a quote with relevance to today’s employment market. There’s no question job growth has been on a tear. In fact, at 93 months and counting, this has been the longest stretch in history with consecutive positive monthly payroll growth, as you can see below.

Record-Breaking Run of Payroll Gains

Source: Charles Schwab, Department of Labor, FactSet, as of June 30, 2018.

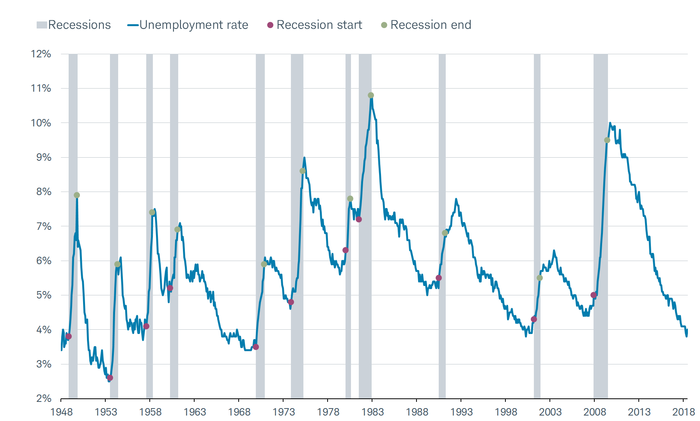

Courtesy of that exceptional string of job gains, the unemployment rate has plunged to depths rarely seen in history—other than, importantly, just before recessions. Notice the dots I placed on the unemployment rate in the chart below. They serve to illustrate the highly-lagging nature of the unemployment rate. Historically it was at extremely low unemployment rates that recessions began (conversely, extremely high unemployment rates accompanied the end of recessions and beginning of recoveries).

Unemployment Rate: Extremely Low (But Lagging)

Source: Charles Schwab, Department of Labor, FactSet, as of June 30, 2018.

The relationship between lagging and leading indicators is always crucial for investors to understand; and is tied to my oft-expressed view that “better or worse matters more than good or bad” when it comes to the connection between economic fundamentals and stock market behavior.

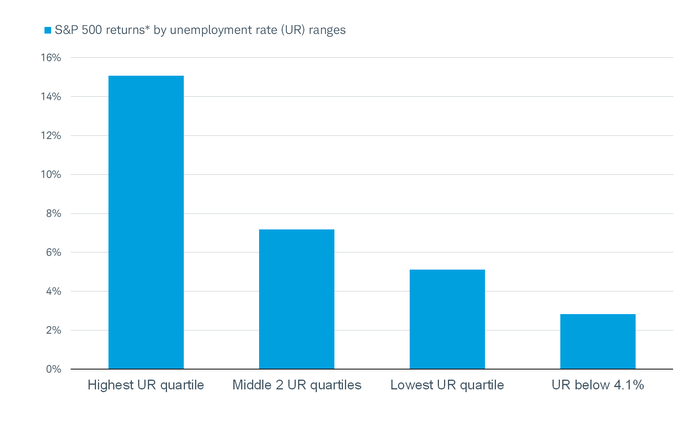

As noted, the unemployment rate is one of the most lagging of economic indicators. On the other hand, payroll growth is a coincident indicator (tends to move in line with the economy), and stocks are a leading indicator. So let’s connect the dots between the lagging unemployment rate and the leading stock market. As you can see in the chart below—against perhaps conventional wisdom—the stock market has historically performed best when the unemployment rate is in its highest quartile; while as the unemployment rate comes down, stocks have tended to behave progressively worse. In other words, there comes a time when Main Street is cheering, but Wall Street begins jeering.

Lower Unemployment Rates = Lower Market Returns

Source: Charles, Schwab. The Leuthold Group. *S&P 500 returns based on monthly data annualized from January 1950-June 2018. Annualized returns are inflation-adjusted by CPI.

The latest jobs report on July 6 brought an uptick in the unemployment rate to 4.0% from 3.8% the prior month. Lest you fear the unemployment rate has found its bottom, it’s important that the increase in the rate was for the “good” reason: the labor force participation rate rose as more people joined the workforce. That said keeping an eye on this going forward is crucial. There has never been a case in the post-World War II period when the three-month moving average of the unemployment rate has risen by more than one-third of a percentage point without a recession ensuing. We are not there (yet).

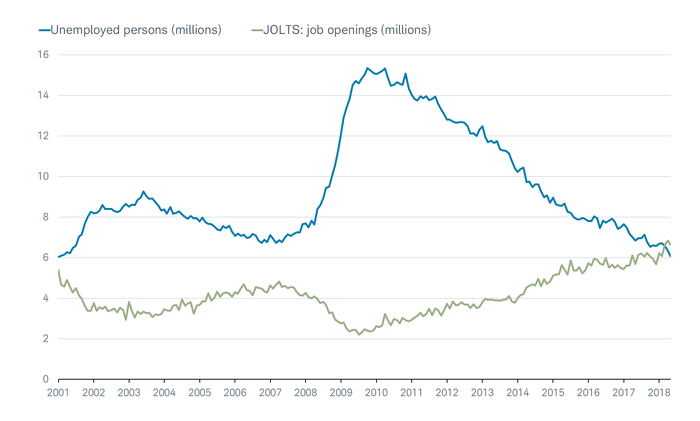

One reason for a pick-up in entrants to the labor pool has been the steady increase in job openings. In fact, as you can see below, for the first time in the history of the Job Openings and Labor Turnover Survey (JOLTS) survey, there are more job openings than there are people unemployed.

More Job Openings Than Unemployed

Source: Charles Schwab, Department of Labor, FactSet, as of May 31, 2018. JOLTS=Job Openings and Labor Turnover Survey.

This is corroborated by data from the National Federation of Independent Business (NFIB) measure of job openings which are hard to fill. We keep an even closer eye on the hiring trends of smaller businesses because they are the net job creators in the U.S. economy.

Record Small Business Job Openings

Source: Charles Schwab, FactSet, as of May 31, 2018. NFIB= National Federation of Independent Business.

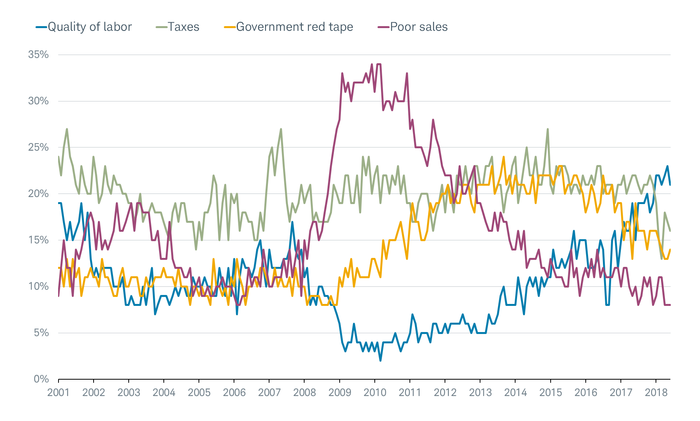

This is where we get to the aforementioned quality problem. The NFIB survey is chock full of questions to its members, including one about businesses’ “single most important problem.” As you can see in the chart below, “quality of labor” has overtaken “government red tape,” “taxes,” and “poor sales” and now sits in spot numero uno. The 21% of business owners citing the difficulty of finding qualifies workers as their biggest problem is only two points below the survey record.

NFIB’s Single Most Important Problem

Source: Charles Schwab, FactSet, as of June 30, 2018. NFIB= National Federation of Independent Business.

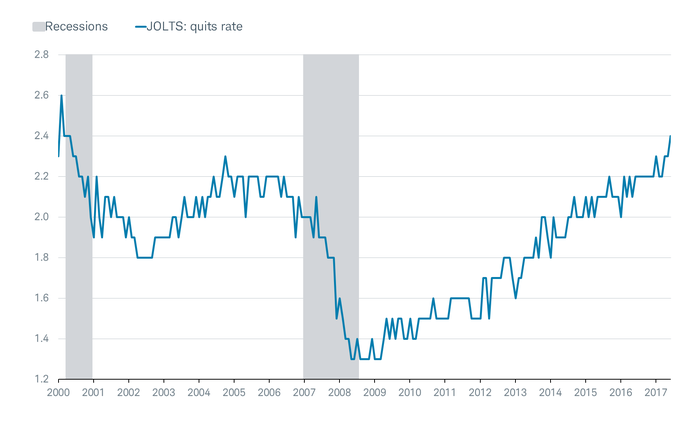

For workers with the right skills, this is an extremely healthy job market, and it’s reflected in compensation data as well. Within the JOLTS release are not only job openings data, but also data on the so-called “quits” rate, which measures the number of employed who have voluntarily left their job…ostensibly because of confidence in finding another job (or already having one offered).

Surge in Job Quitters

Source: Charles Schwab, Department of Labor, FactSet, as of May 31, 2018. JOLTS=Job Openings and Labor Turnover Survey.

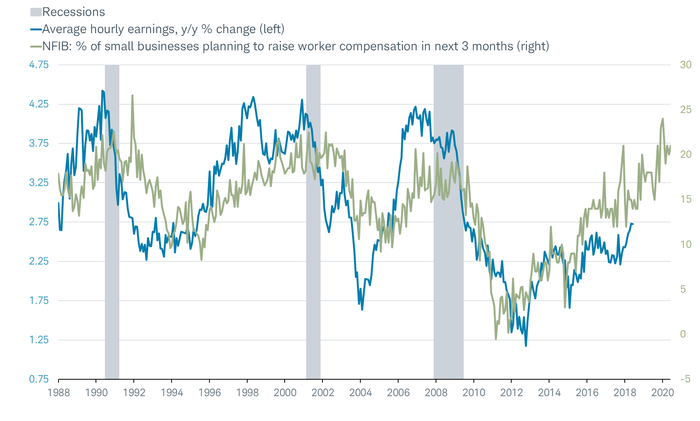

None of these stellar trends have yet to individually or collectively translated into sustainable higher wage growth; but I think we’re on the cusp of further improvement. The chart below compares the standard measure of wage growth—average hourly earnings (AHE)—with the NFIB-based percentage of companies planning to raise worker compensation. Unless we are disconnecting the historical relationship between these two, wage pressures should continue to rise.

Wage Pressures Increasing

Source: Charles Schwab, Bureau of Labor Statistics, FactSet, Strategas Research Partners LLC, as of June 30, 2108. NFIB (NFIB= National Federation of Independent Business) advanced 24 months.

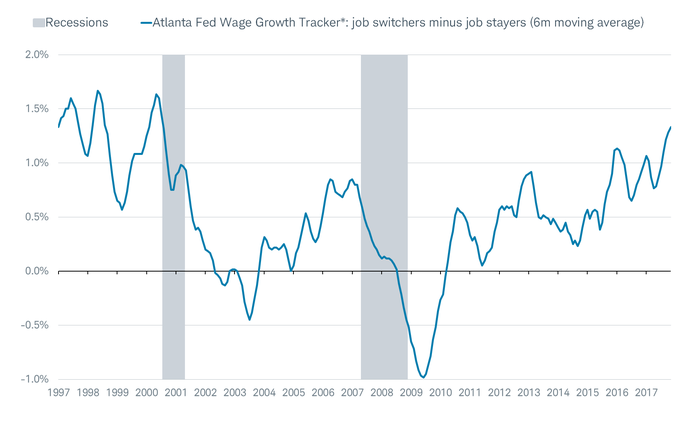

We are already seeing more significant upward pressure on wages among the “job switchers” set relative to the “job stayers.” The chart below looks at the difference between the two, with the rising line highlighting the increased wages that companies with open positions have to offer to entice folks into those positions.

Job Switchers’ Higher Wages

Source: Charles Schwab, Federal Reserve Bank of Atlanta, as of June 30, 2018. *Three-month moving average of median wage growth.

There are some chinks in the armor of healthy employment conditions. According to Challenger, Gray & Christmas, hiring announcements over the past six months fell from 468k to 233k over the same period last year; while over the past year, layoff announcement were up 8%. This is in keeping with The Conference Board’s data on help wanted online ads, which were down 9% in this year’s first half.

The net is that for the first time in more than a decade, the U.S. economy is essentially at full employment. Typically, fiscal policy would be getting tighter to prevent economic over-heating; but clearly that’s not the case in this cycle, with fiscal policy going full-out courtesy of tax cuts, regulatory reform and government spending. So the risk of over-heating is real—if not yet in our sights.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

©2018 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab