Higher Ground: Wage Growth Makes its Move

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Points

-

Friday’s jobs report was gangbusters, and finally included a wage growth jump to above 3% for the first time this cycle.

-

Is the tightness in the labor market and higher nominal growth enough to resurrect the Phillips Curve?

-

This year’s second market correction may be reinforcing that this year may have Main Street more joyous than Wall Street.

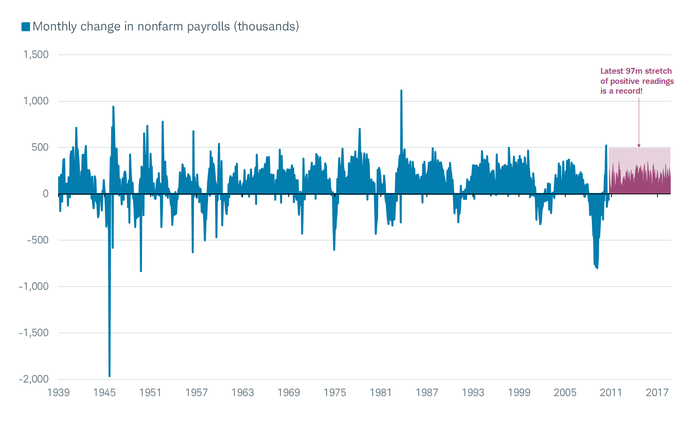

Friday brought another strong employment report, along with an end to a very volatile week for stocks. October’s non-farm payroll employment rose by 250k, well above expectations for 188k; albeit with at least 30k of that increase attributable to the recovery from Hurricane Florence. The U.S. economy has had positive payroll growth for a record 97 months, as you can see in the chart below.

Record String of Job Gains

Source: Charles Schwab, Department of Labor, FactSet, as of October 31, 2018.

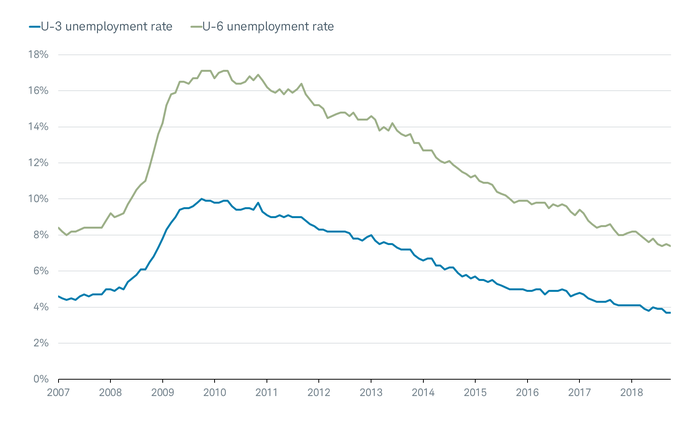

Household employment (the survey from which the unemployment rate is calculated) jumped 600k, following 420k in September. In spite of the surge in household employment, the unemployment rate remained steady at 3.7%, matching the lowest reading since the end of 1969. But that was for a good reason—the labor force participation rate (LFPR) rose 0.2% (+711k) to 62.9%. In addition, the broadest (U-6) did dip to 7.4% from 7.5%; while the teenage unemployment rate fell below 12%, for the first time since 1969.

Unemployment Rate(s) Remain Extremely Low

Source: Charles Schwab, Department of Labor, FactSet, as of October 31, 2018.

Private sector payrolls were up 246k, with gains broad-based across all industries: Services payrolls were +179k, led by leisure/hospitality +42k, health care +36k, professional/business services +35k, transportation/warehousing +25k; while goods-producing payrolls were +67k, led by manufacturing +32k.

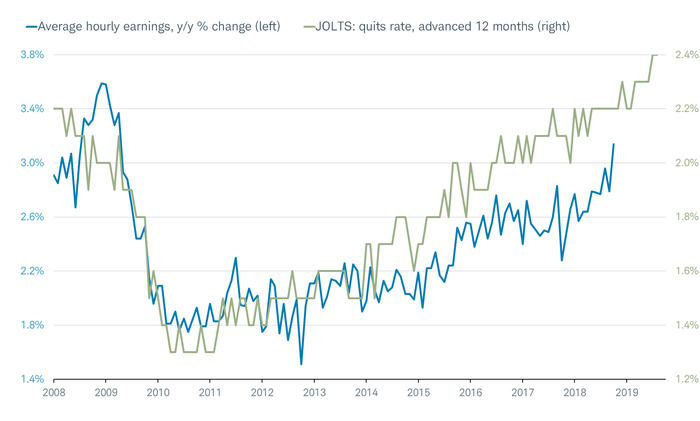

The number-within-the-numbers that appropriately received the most attention was average hourly earnings (AHE), which were +0.18% quarter/quarter; putting the year/year at +3.14%—the first move above 3% in this expansion to-date. Historically, once wage growth jumps above 3%, it typically accelerates further to at least 4%.

The chart below shows AHE in this cycle to-date, tracked against a 12-month advanced “quits rate,” which comes from the monthly Job Openings and Labor Turnover Survey (JOLTS). The impressive strength in the latter suggests further upward pressure on AHE.

Quits Rate Leads Wage Growth

Source: Charles Schwab, Department of Labor, FactSet. Hourly earnings as of October 31, 2018. JOLTS (Job Openings and Labor Turnover Survey) as of August 31, 2018.

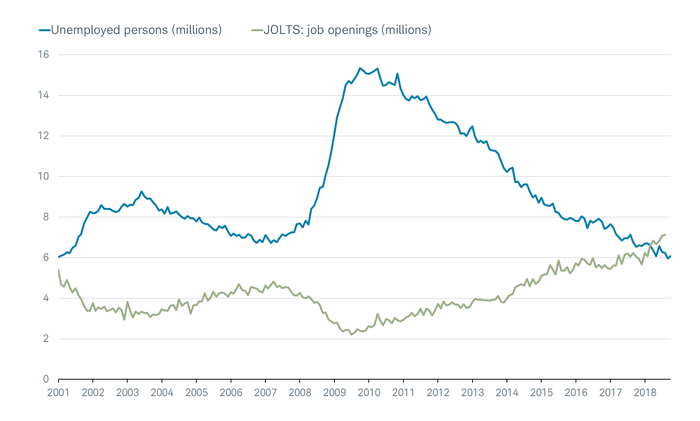

The jump in AHE reflects a tightening in the labor market that may have moved into a sharper trajectory. The headline from JOLTS is job openings, which have exceeded the number of unemployed people for six consecutive months, as seen in the chart below. This is the first time in the history of the data that there are not enough workers to fill the jobs available. Related to that is the survey data from the National Federation of Independent Business—its members now express more concern about finding appropriate-skilled workers than any other factor affecting their business.

Not Enough Workers for Jobs Available

Source: Charles Schwab, Department of Labor, FactSet. Hourly earnings as of October 31, 2018. JOLTS (Job Openings and Labor Turnover Survey) as of August 31, 2018.

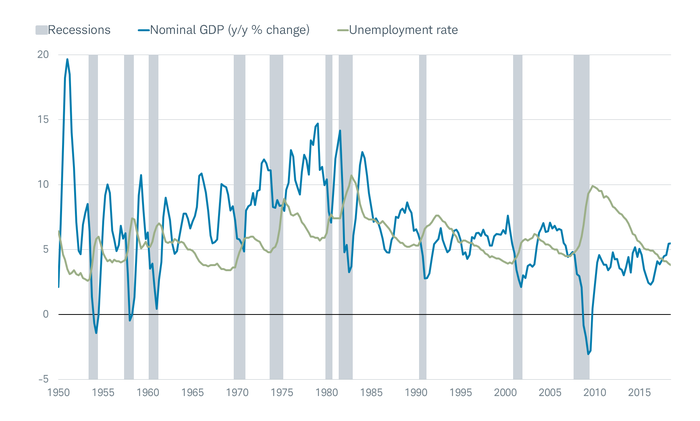

Another indication of higher wage pressures to come is the level of nominal economic growth relative to the unemployment rate. The chart below shows that, until earlier this year, the unemployment rate was above nominal gross domestic product (GDP) growth since before the financial crisis. Courtesy of both the improvement in growth, and the persistent decline in the unemployment rate, nominal growth is now comfortably above the unemployment rate.

Nominal Growth Finally Exceeds Unemployment Rate

Source: Charles Schwab, FactSet, as of September 30, 2018.

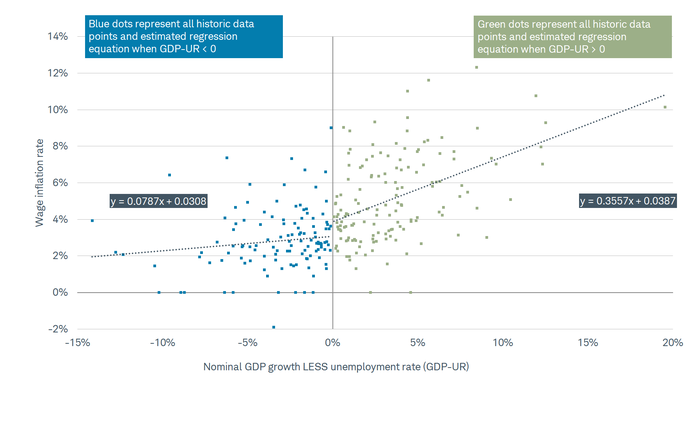

Why should we care about the relationship shown above? It turns out it may explain why the “Phillips Curve” has gone missing in this cycle, until perhaps now. For readers not aware, the Phillips Curve—named after William Phillips, but popularized by Milton Friedman—shows a historical inverse relationship between changes in the rate of unemployment and changes in the rate of wage growth.

But the Phillips Curve has been MIA, and many economists, Federal Reserve watchers (and even some Fed members themselves) have questioned whether it should be left for dead. I’m not so sure.

The Leuthold Group scattergram chart below is a tale of two sides of the coin. The blue dots on the left, and corresponding regression line, represent the relationship between wage inflation and the unemployment rate—when the unemployment rate has been above nominal GDP. As you can see, the regression line is fairly flat; i.e., no Phillips Curve in evidence. However, the green dots on the right, and corresponding regression line, represent the relationship between wage inflation and the unemployment rate—when nominal GDP has been above the unemployment rate. As you can see, the regression line is much steeper; i.e., Phillips Curve is back!

Phillips Curve Kicking Back In?

Source: Charles Schwab, The Leuthold Group. June 30, 1952-September 30, 2018.

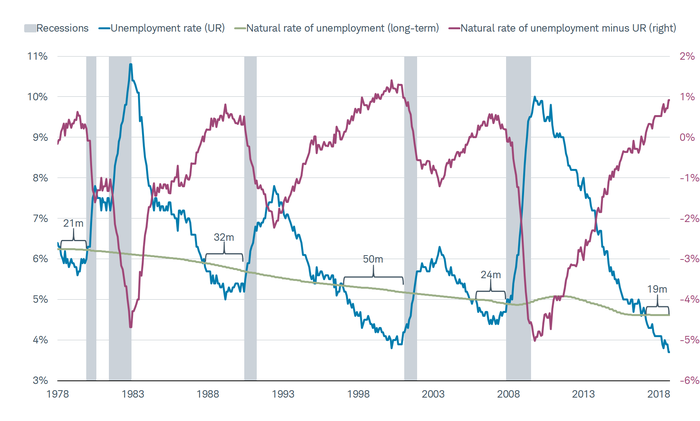

Another useful comparison associated with labor market tightness is between the unemployment rate and the “natural rate” of unemployment. The latter, developed by Milton Friedman and Edmund Phelps, for which they received the Nobel Prize in economics, represents the steady state of “full” employment (distinct from “zero” unemployment). It represents the hypothetical unemployment rate consistent with aggregate production being at the long-run level.

As you can see in the chart below, nineteen months ago, the unemployment rate (blue line) crossed below the natural rate (green line), with the difference between the two (maroon line) now at-or-above historical peaks. Those historical peaks, as you can see, tended to “warn” that the runway to the next recession (gray bars) was shortening.

Unemployment Rate Well Above Natural Rate

Source: Charles Schwab, Department of Labor, FactSet, U.S. Congressional Budget Office, as of October 31, 2018.

With all this “winning” seen in labor market statistics, one might wonder about heightened stock market volatility and the recent correction—the second this year. The explanation is fairly simple. The tightness in the labor market is a classic late-cycle characteristic, as are tightening monetary/financial conditions.

Since the beginning of this year, the 10-year real Treasury yield is up about 70 basis points (115 basis points over the past two years); while the 10-year breakeven inflation expectations are up about 7 basis points this year, and about 45 basis points over the past two years. The difference between the two is seen as a measure of monetary tightness, and although monetary conditions may not yet be tight in an absolute sense, but they are at their tightest level in more than two-and-a-half years.

Specific to Friday’s jobs report, expectations for a December Fed rate hike moved from 71% to 74%. For those who wonder why the futures market-based odds are not higher, do note that there is a more than 15% probability that the Fed hikes rates at its meeting this month (which also moved higher after the jobs report).

Tighter monetary/financial conditions are both a trigger for (and a result of) higher equity market volatility. For those who wonder why stock market weakness often accompanies a low and still-falling unemployment rate, it’s as simple as understanding the relationship between lagging economic indicators (like the unemployment rate) and leading economic indicators (like the stock market).

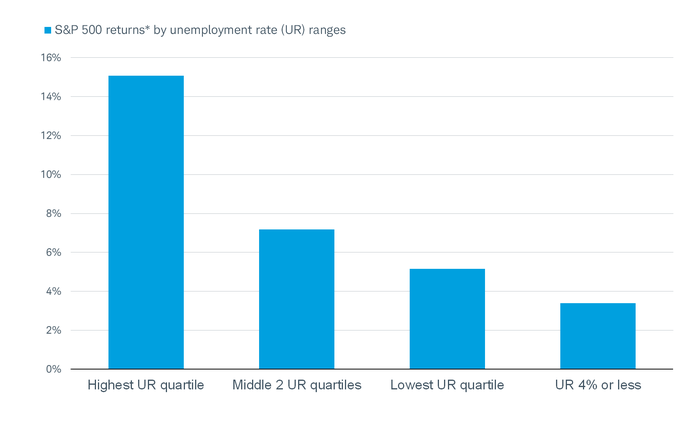

Illustrative of this relationship is the historical nature of stock market returns during the phases of the unemployment rate. Because the stock market is a leading indicator, it tends to launch out of bear markets at the point the unemployment rate is high (and in some cases, still rising, like in March of 2009).

Stocks tend to anticipate the coming improvement—they don’t “wait” until the improvement is already underway. Conversely, when the unemployment rate is low (and in many cases, still falling, like today), stocks’ gains tend to fade; reflecting that the best is no longer yet to come. This is why, as you can see in the chart below (with data courtesy of The Leuthold Group), the best returns for stocks historically came when the unemployment rate was in its highest quartile; while returns were significantly more subdued when the unemployment rate was below 4%, like today.

Market “Likes” Higher Unemployment

Source: Charles Schwab, The Leuthold Group. *S&P 500 returns based on monthly data annualized from September 30, 1950-September 30, 2018. Annualized returns are inflation-adjusted by CPI.

In sum, Main Street has much to cheer with the ongoing strength in the labor market—especially given that it’s finally accruing to workers in wage growth terms. But as is typical later in economic cycles, the tightness in the labor market brings with it commensurate tightness in monetary/financial conditions, which tend to bring with it higher equity market volatility. Right on cue, we recently experienced yet another bout this year of “Main Street” feeling better than “Wall Street.”

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

©2018 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All