Stocks have taken a beating over the past few months in what we’ve been describing as a rolling bear market, but we don’t see a repeat of 2008 likely developing.

U.S. economic growth continues, but at a slower pace; and we expect more slowing this year. The threat of recession has increased as a decline in confidence among consumers and businesses risks becoming a self-fulfilling prophecy, with the Fed and the trade war with China continuing to hold keys to the degree of slowing and the timing of the next recession.

Political problems aren’t only in the U.S. as developments around the world could impact market performance.

“I have learned that peace is not the absence of trial, trouble, or torment but the presence of calm in the midst of them.” - Don Meyer

Happy New Year?

Few investors were sorry to see 2018 go—with the worst December for stocks since the Great Depression wrapping up a tough year, although marginally salvaged by a decent final week. But the S&P 500 did end the year in the red for the first time since the end of the global financial crisis. Will the New Year bring in a different path? Almost certainly—years don’t tend to repeat themselves and although past performance is certainly no guarantee of future results, history is somewhat in the bulls’ favor, with the S&P 500 declining in back-to-back years four times since 1929. Uncertainty on the monetary, fiscal, and trade fronts have all contributed to the recent decline, which helped feed growing recession fears—with The Wall Street Journal reporting that Google searches for “recession” spiked in December. However, although recession fears among consumers have risen, the recent holiday shopping season looks like it was a robust one. Mastercard said it was the best season in six years, with a 5.1% year-over-year gain (CNBC).

In addition, the labor market remains strong, with the December nonfarm payrolls report showing 312k jobs created—well above the 176k consensus expectation, while the previous two months were revised higher by 58,000 jobs. However, the unemployment rate rose from 3.7% to 3.9%; importantly though for the “right” reason as 419k new workers entered the workforce (the labor force participation rate increased to 63.1%), but some are still looking for jobs—resulting in an uptick in the unemployment rate. In addition to the ample payroll gain, average hourly earnings (AHE) jumped 0.4% last month with the year-over-year rate moving from 3.0% to 3.2%. That gain is tied with October for the strongest wage gain since April 2009. The better data could help alleviate some of the concern that has crept in regarding the labor market courtesy of the uptick in initial unemployment claims—a leading indicator. That remains an area of focus, although some of the recent uptick was partly tied to weather/hurricanes.

Claims still indicate healthy labor market

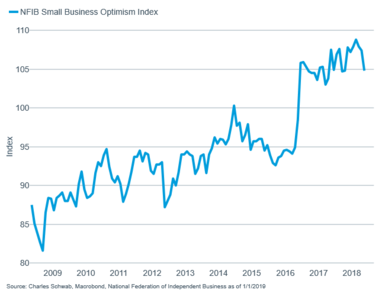

While job growth remains strong and the consumer continues to spend, there has been a downtick in business confidence, which can feed through to the consumer at some point. We may be seeing some of that already as consumer confidence dipped in the most recent reading from The Conference Board. This was to be expected as there is a fairly high correlation between the stock market and consumer confidence.

But businesses are expressing decreased optimism

Planning for the future can become quite difficult for businesses in an environment of heightened uncertainty. For now, the forward earnings yield over 10-year Treasures has historically tended to be a positive sign for stocks, with the S&P 500 returning more than 10% annually during such occurrences per Strategas Research.

Earnings spread over Treasuries typically positive signal

In addition, valuations have improved courtesy of the market’s correction, with the S&P forward price-to-earnings ratio standing at roughly 14.3 according to FactSet. However, estimates for 2019 continue to be ratcheted down and an earnings recession (if not an economic recession) is a possibility this year—similar to what occurred from the second half of 2015 through the first half of 2016.

2008 Redux?

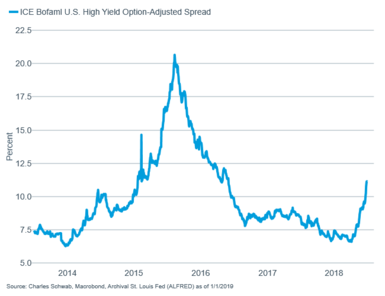

The problem with valuation is that it has not proven to be a successful market timing tool (not that there are any consistently successful market timing tools). While we are seeing a slowdown in activity, and the possibility of a (mild?) recession, it appears there is still some “muscle memory” from the 2008 financial crisis, with many clients worried about another 2008. Jeff Kleintop addresses this issue in his article “Where will the next crisis come from”, but to summarize…we don’t think so. The 2008 financial crisis was a function of a massive housing debt bubble, derivatives tied to that debt, and a heavily over-leveraged global financial system; which ultimately took the entire global economy down with it. We don’t see the extreme of excesses that had built up back then. Banks, according to the Federal Reserve and their stress tests, are much better capitalized and prepared this time around. There are risks—the high yield market and the precipitous drop in oil prices are both showing some signs of increased economic stress, which should not be ignored.

Fixed income market showing stress

While the drop in oil is concerning

So what’s an investor to do? Although we never try to time the market with any kind of precision, we do recommend tactical shifts around strategic allocations. We moved to a more defensive posture beginning in the second half of 2017, having downgraded equities (with a large cap over small cap bias within U.S. equities); followed by key sector downgrades in August of last year (when we lowered our rating on technology and financials). We continue to think a defensive stance is warranted as we begin 2019, believing heightened volatility and often-dramatic swings will characterize at least the first part of the year.

Don’t fight the Fed…or trade…or the shutdown?

So what should investors be watching for signs that the coast may be clearing? First, the government “shutdown” is a bit of a misnomer as over 75% of the government continues to be funded, notwithstanding the pain for the decent percentage of government workers not receiving a paycheck. A reopening of the full government should ease some of the present uncertainty. Second, the Federal Reserve, after disappointing the market by not appearing dovish enough following the December rate increase, appears to have made an effort to reiterate its data dependence, with Fed Vice Chairman Richard Clarida reiterating its data dependent nature on CNBC recently. Fed Chair Jerome Powell also noted that there is no present path and that the Fed will be patient and flexible—potentially a positive signal that the Fed could be open to pausing its rate hike campaign. Likewise, the trade dispute with China has shown fledgling signs of hope as both the United States and China are facing struggling markets and weakening economies—these forces could keep pressure on negotiators to work diligently on a deal. Whether a deal getting done is sufficient to turn the market around is yet to be seen. Other factors affecting the path of least resistance for stocks, which remains down, are financial conditions and earnings expectations heading into fourth quarter earnings season.

Given the uncertainty that still exists, we continue to recommend a more defensive position with regard to equities, both domestic and global. But we never recommend an all-or-nothing position and believe investors should make limited tactical shifts around longer-term strategic allocations; while remaining disciplined around diversification and more frequent rebalancing.

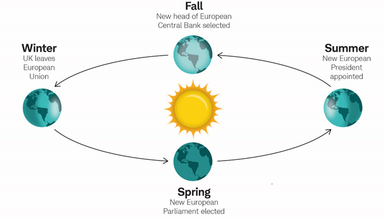

Record year for European political changes set for 2019

Things aren’t just interesting in the U.S. political world! In addition to slowing global growth and the increasing drag from worsening financial conditions, combined with full employment and rising prices, stock markets around the world will still have to contend with political developments in the New Year. In 2018, the trade tensions and mid-term elections kept investors largely focused on political developments in the United States. This continues into early 2019 with the ongoing partial U.S. government shutdown and pending U.S. trade talks with China on January 7. However, Europe may vie for the spotlight when it comes to political events in 2019.

This year is a major year of political change for the European Union. The United Kingdom is currently scheduled to leave the EU in March as winter ends. The EU will elect a new Parliament in the spring, and next summer will bring the appointment of a new President. In the fall, a new head of the European Central Bank (ECB) will be selected. This will be the first time in EU history that so many key institutions will see changes within the same year, and it may result in some uncertainty over the future direction of fiscal and monetary policy as the global economy slows.

Political changes for all seasons

Spring: New Parliament elected

Why it matters: The European Parliament shares with the Council of the European Union the responsibility of amending or rejecting legislation; determining the laws for the EU. The outcome could influence the direction and effectiveness of fiscal policy.

What to watch: Polls suggest that the mainstream center-right and center-left parties will fail to get a majority of seats as populist parties rise in influence in the May 23-26 vote. A strong showing by populist parties may make progress on reforms unlikely and would contribute to increasing political fragmentation and make decision-making harder to do. If the willingness or ability of the European government to mount an effective response to an economic or financial shock is impaired, it could lead to a crisis.

Summer: New President appointed

Why it matters: Following the parliamentary elections, the next president of the European Commission—the EU’s executive branch that proposes legislation and implements decisions—will be appointed to a five-year term. The current President, Jean-Claude Juncker, has said he will not seek a second term. His five-year term did include an economic recovery, but also bitter Brexit negotiations and an immigration crisis tied to the war in Syria. The next five years will likely hold new challenges for the incoming President.

What to watch: The President is chosen by a vote of member countries, and then ratified by the European Parliament. Increasing political fragmentation may make it hard to confirm a new President that has broad enough support to effectively negotiate trade agreements and other contentious issues that may affect markets.

Fall: New Head of the European Central Bank selected

Why it matters: The eight-year term of Mario Draghi as president of the European Central Bank (ECB) ends on October 31. Mario Draghi’s term was characterized by the introduction of the quantitative easing (QE) bond-buying program and record low interest rates, with a major impact on markets. Most notably, he committed the central bank to do "whatever it takes" to preserve the euro during the 2012 European debt crisis; proposing a program designed to buy bonds issued by distressed Eurozone countries. Although the ECB never ended up using the controversial program, the pledge was enough to calm the markets.

What to watch: The vote/negotiation could result in a more conservative president. In its 20 years the ECB has had Dutch, French and Italian presidents. Germany may now push for one of its own, Jens Weidmann, the current president of the German central bank, to lead the ECB starting November 1. Jens Weidmann, or someone like him who opposed many of Mario Draghi’s policies, may take a more aggressive approach to ending the ECB's expansionary monetary policies.

There are also smaller political events in the European Union this year, such as the November election of the President of the European Council. While they do add to the political change in Europe this year, these roles are generally not nearly as influential on policy or markets as those discussed above.

Political events themselves aren't likely to be driving the economic and earnings results most important to investors. However, because policymakers may be called upon by the market to respond to any deterioration in economic and earnings growth, the political changes the year may bring could result in challenges for investors in 2019.

So what?

It can be difficult to remain calm in the midst of stock market action like we’ve seen over the past couple of months—but discipline is necessary during more tumultuous times. Although we do see rising risk of a recession, we don’t see a repeat of 2008 in the cards. Absent a recession—even if we enter a “formal” bear market (at its recent closing low, the S&P was down 19.8%)—additional weakness may be somewhat limited. Recession-related bears tend to be longer and grizzlier than non-recession bears. Until we get more clarity on the health of the economy, we continue to suggest investors remain defensive.