U.S. equities have rebounded as some macro concerns have eased. However, risks remain and we don’t believe that stocks are yet fully in the clear—volatility will likely persist and our tactical recommendations remain modestly defensive.

Recession concerns have receded somewhat, alongside waning worries that the Federal Reserve will go too far. That said economic growth is slowing and the Fed still has a difficult road to navigate—especially given its dual mandate of price stability and full employment.

Brexit drama continues but the need for investors to worry may be limited.

“When events change, I change my mind. What do you do?” - Paul Samuelson

Changing dynamics

Stocks have staged a nice rebound following the sharp selling that culminated on Christmas Eve. It seems clear that market dynamics have changed somewhat, from the “sell first, ask questions later” attitude that dominated last year’s final quarter; with the tenor of the post-Christmas rally fairly healthy from a breadth standpoint (read more at Every Rose Has its Thorn: Healthy Rally but Risks Linger). Many individual stocks are still getting punished for genuinely bad news—such as a few retailers recently on weaker-than-expected holiday results—but for now those concerns have not translated into broader economic or stock market carnage. While more positive, all is not clear in our view and obstacles to a sustainable uptrend remain in place. There have been some positive developments in the China/U.S. trade dispute but a deal remains elusive; the Federal Reserve has backed off some of the more hawkish rhetoric, but the risk of a monetary mistake remains; Brexit remains a major uncertainty (more on that below); and the U.S. government hasn’t done a lot to inspire confidence recently, with its record-breaking shutdown.

Trade, economic, monetary policy, and earnings risks are what led us to move to a modestly defensive investment posture last year, reducing our rating on emerging markets, while moving to a slightly defensive posture with our Sector Views. But our view that volatility would bring sharp moves in both directions is why we didn’t go to a more drastic defensive stance. We continue to believe that the odds of a U.S. recession in the near-term are fairly low; however, trade (and the government shutdown) will likely provide guidance as to the length of runway between now and the next (inevitable) recession.

Economic growth slowing, but not drastically…yet

There is little doubt economic growth is downshifting as 2019 gets underway. Both the manufacturing and services Institute for Supply Management (ISM) surveys declined over the past month, with the New Orders component of the Manufacturing Index (a forward looking indicator) falling sharply to 51.1—dangerously close to the 50 dividing line between expansion and contraction.

ISMs show economic growth slowing

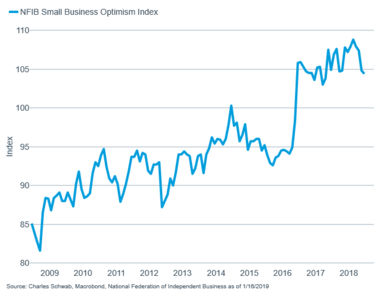

Coinciding with these declines, we’ve seen small business optimism weaken, alongside weakening larger company CFO optimism.

As does the NFIB Optimism Index

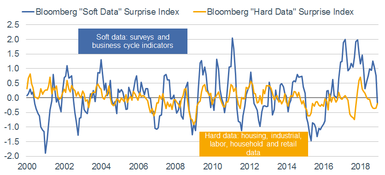

These reading are concerning as a loss of business confidence can lead to a self-fulfilling prophecy. If businesses are nervous and pull in the reins, they don’t spend or hire, which leads to economic slowing; and can lead to a possible recession if the caution goes too far. In fact, we have seen a remarkable convergence recently between “soft” (confidence/survey-based) and “hard” economic data. The chart below shows that the soft data has been coming in much worse relative to expectations; as such, it’s been catching down to the hard data.

Soft data is catching down to hard data

Source: Bloomberg. Soft data: surveys and business cycle indicators. Hard data: housing, industrial, labor household and retail data. As of 01/15/19.

For now though, labor conditions remain healthy, evidenced by the blowout December jobs report. According to the Bureau of Labor Statistics, 312,000 non-farm payrolls were created, while the unemployment rate ticked up for the “right” reason (a pick-up in the labor force participation rate). Wage growth continues to be boosted by the tight labor market, with average hourly earnings hitting a cycle-high of 3.2% year-over-year growth. And, a more forward-looking indicator, initial jobless claims, while buffeted by a hurricane and most recently the partial government shutdown, remain near historic lows.

But the labor market continues to look healthy

Earnings season on deck

We’ll get more information on this mixed economic picture in the next few weeks as fourth quarter 2018 earnings season ramps up. Consensus expectations have been cut over the past couple of months according to Thomson Reuters, but the “beat rate” is expected to be much less than the norm. Forward guidance will be important as well given the slashing that’s been done to 2019 estimates relative to 2018’s tax cut-related growth. Commentary on capital expenditure plans, consumer behavior, and trade impacts will all be of interest—both in how they are affecting actual results, but also sentiment as we look to future quarters.

Fed changes tack…but not the Federal government

The decline in business confidence, combined with the sharp fourth quarter 2018 drop in equities, appears to have pushed the Federal Reserve to “clarify” its position on the rate outlook. The statement accompanying the Fed’s December meeting was received as relatively hawkish; but when the minutes from that meeting were released last week, the tone was read as more dovish. Fed speakers as of late, including Chairman Jerome Powell, appear to have gone out of their way to emphasize that they have no preset course and that patience is warranted. However, expectations for no additional rate hikes may need to be adjusted if we get another couple of strong jobs reports; especially if they include hotter wage growth.

The Fed represents only one part of the drama emanating out of D.C. Investor angst over the ongoing partial government shutdown has been rising, with estimates of the damage moving up. In fact, a few economists recently have suggested a shutdown lasting the entire first quarter could wipe out most or all of the quarter’s gross domestic product (GDP) growth (Wall Street Journal).

Brexit: what’s next?

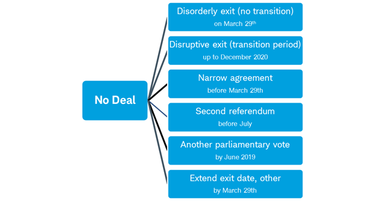

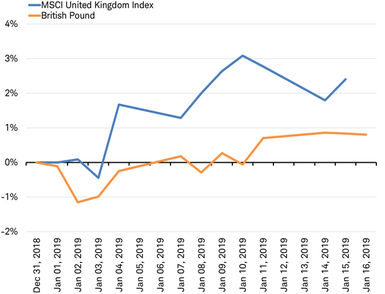

Americans can perhaps be comforted by looking at the political situation across the pond. There remains a range of Brexit-related paths for the United Kingdom (UK), as seen in the graphic below. While it is unclear what members of Parliament would support—and what the European Union (EU) would allow)—it is clear what they do not support: 1) Prime Minister May’s plan and 2) the default option of a disorderly exit of the EU on March 29 with no agreement with the EU or period of transition. Both the British pound and the UK stock market have posted modest gains so far this year. These markets seem to be encouraged that while this may eliminate the “best” case outcome, it may also eliminate the worst.

Potential next steps in the Brexit process

Source: Charles Schwab as of 1/16/2019. For illustrative purposes only.

What are the risks in the worst case of a disorderly exit? If the UK leaves abruptly, without a transition period, it would risk a painful UK recession and a potential bear market for UK stocks—reasons politicians are reluctant to allow this outcome to happen. However, the spillover to the rest of the world may be limited. The greatest business disruption from Brexit may be to UK financial services companies; yet we believe financial contagion from the UK banking system seems unlikely. According to the Financial Times, under the direction from regulators , banks are already implementing contingency plans with a March 29 completion date.

What’s next? After surviving both a challenge to her role as Prime Minister and to her government, Theresa May has until Monday (January 21) to come up with an alternative plan. Next steps continue to evolve. It seems increasingly likely the March 29 exit date may be extended, giving the UK more time to allow for outcomes such as another plan to be put to a parliamentary vote, a narrow deal that covers the settlement of the divorce but leaves a period until December 2020 to define the future trade relationship; or even a second referendum, among others. However, the extension is likely to be short in duration due to European Parliamentary elections scheduled in May.

UK stocks and currency have posted gains year-to-date

Source: Charles Schwab, Bloomberg data as of 1/16/2019. Past performance is not indication of future results.

What does this mean for investors? The UK constitutes 6% of the MSCI World Index and 17% of the MSCI EAFE Index; while the British pound is 12% of the Dollar Index. Some Brexit pessimism had been priced in to both UK stocks and the pound over the past six months; but the gain in the pound in the weeks ahead of the vote (shown in the chart above) may imply some hope that the worst case of a disorderly Brexit may be avoided. If the exit date is extended past March 29, to allow for outcomes that avoid a disorderly Brexit, markets could continue to rebound. But that could succumb to further volatility as the way ahead seems unlikely to be straightforward. After all, Brexit has been characterized by the unexpected since the referendum in June 2016.

So what?

U.S. stocks have staged a nice rally to start the year but we don’t believe it reflects an all-clear sign. We continue to recommend investors adopt a highly-disciplined approach to asset allocation, especially around diversification and rebalancing. Risks to both the U.S. and global markets/economy remain, and we expect continued bouts of volatility.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may

International investments are subject to additional risks such as currency fluctuations, political instability and the potential for illiquid markets. Investing in emerging markets can accentuate these risks.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. This content was created as of the specific date indicated and reflects the author’s views as of that date.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment. Rebalancing may cause investors to incur transaction costs and, when rebalancing a non-retirement account, taxable events may be created that may affect your tax liability

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. The policy analysis provided does not constitute and should not be interpreted as an endorsement of any political party.

The Institute for Supply Management (ISM) Manufacturing Index is an index based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries.

The Institute for Supply Management Non-manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms' purchasing and supply executives, within 60 sectors across the nation, by the Institute of Supply Management (ISM). The ISM Non-Manufacturing Index tracks economic data, like the ISM Non-Manufacturing Business Activity Index.

The Small Business Optimism Index is compiled from a survey that is conducted each month by the National Federation of Independent Business (NFIB) of its members.

The MSCI United Kingdom Index is designed to measure the performance of the large and mid-cap segments of the UK market. With 102 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in the UK.

The MSCI World Index is a stock market index of 1,642[1] 'world' stocks. It is maintained by MSCI Inc., formerly Morgan Stanley Capital International, and is used as a common benchmark for 'world' or 'global' stock funds. The index includes a collection of stocks of all the developed markets in the world, as defined by MSCI. The index includes securities from 23 countries.

The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The MSCI EAFE Index consists of the following 22 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.

The US Dollar Index (USDX) is a measure of the value of the U.S dollar by the IntercontinentalExchange (ICE) relative to a basket of foreign currencies, particularly the Euro, the Japanese yen, the UK (British) pound sterling, the Canadian dollar, the Swedish krona, and the Swiss franc.

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.