Three Technology Titans Reshaping Retail

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPowerful retailing disruptors are reshaping expectations about shopping and shipping by digitizing retail markets across the globe. New conveniences such as ordering groceries with a simple voice command are upending the old-world order. In this excerpt from the latest edition of FT Thinks: “Three Technology Titans Reshaping Retail,” senior equity analysts across our Growth, Value and Emerging Markets teams compare how three retailing giants tailor technology to fit local customs, lifestyles and payment abilities.

Reshaping Retail on the Global Stage

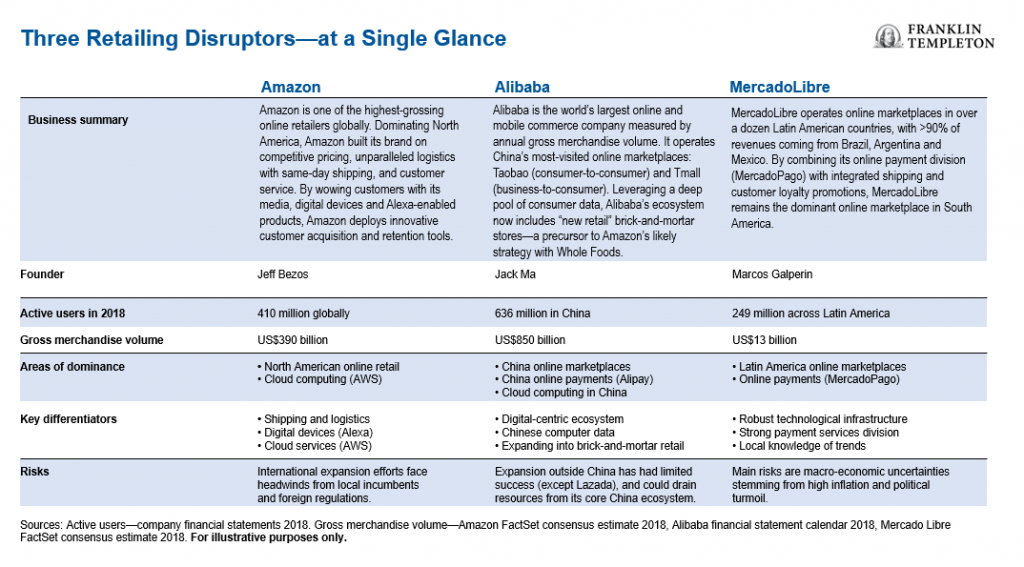

To say that Amazon has shaken up US retailing is almost a cliché at this point. Looking globally, we see powerful tremors from seismic shifts in retailing driven by Alibaba in China and MercadoLibre in South America. These firms, however, aren’t cookie-cutter versions of Amazon. Whereas Amazon spent years building state-of-the-art warehouses and logistics infrastructure, Alibaba and MercadoLibre didn’t need to because they didn’t own inventory. Both firms initially had more in common with eBay, allowing merchants to sell goods on their online marketplaces.

Over time, these distinctions have blurred. Alibaba and MercadoLibre have been investing in logistics infrastructure to help ensure deliveries reach customers on time. Meanwhile, over half of Amazon’s online sales now come from higher margin third-party sellers, which list their products directly alongside Amazon’s own warehouse inventory.

Amazon—an Advertising Powerhouse

Amazon is big, and its disruptive impacts are far-reaching—just as its name implies. But it has only recently become a profitable disruptor. That change has been driven, in part, by becoming a powerhouse in online advertising. At the core of Amazon’s advertising services is a rich pool of data it keeps on the shopping habits of its estimated 410 million active users globally.

Amazon knows what customers browse for and buy and what they are willing to pay, giving them an information advantage over platforms that don’t facilitate transactions themselves. And because Amazon visitors are primarily there to make a purchase, Amazon ads convert to sales at 3.5x higher rate than Google ads.1 Going forward, our US Growth team believes Amazon’s ad revenues will remain a significant profit stream.

Amazon hasn’t had a straight line to success since going public in 1997. And that’s perfectly fine with Jeff Bezos, chief executive officer (CEO) and founder of Amazon. In his view, being a game changer requires experimentation, a willingness to fail, and a long-term orientation that means capital investments can take five to seven years to bear fruit.2 This approach has led to some surprising breakthroughs, like Amazon’s Echo smart speakers, powered by Alexa, the cloud-based voice assistant. But it’s also produced disappointments that unnerved shareholders, like the Fire Phone, and mounting losses from failed efforts to compete in China.

Alibaba’s Retailing Ecosystem

Two years after Amazon went public in 1997, China’s Alibaba launched a business-to-business (B2B) website for small manufacturers looking to export overseas. Alibaba’s birth as an online retailing giant, however, didn’t really happen until four years later in 2003, the year eBay acquired China’s Eachnet.com. Countering eBay’s move, Alibaba quickly launched an online marketplace called Taobao, connecting fledgling merchants and small entrepreneurs with Chinese shoppers.

In just two years, Taobao’s share of China’s market of small businesses selling to consumers approached 60%, forcing eBay to close down Eachnet.com in 2006.3

Most shoppers in China didn’t own credit cards, and many were suspicious that online products might arrive as something less than advertised. Alibaba developed Alipay to resolve both issues. It creates an escrow service in which cash received for a sale isn’t released until the product arrives in satisfactory condition.

Alipay was quite lucrative as a standalone business, but it also gave Taobao a leg up over eBay, which didn’t offer an Alipay-like service. Today, Alipay processes 80% of all transactions across Alibaba’s ecosystem of online marketplaces and 60% of China’s total mobile transactions.4

Taobao’s rapid growth and ability to outmaneuver eBay were extraordinary by any yardstick, and it became hugely profitable. Like eBay, Taobao didn’t own or hold inventory in expensive warehouses.

Taobao’s strong operating margins come from consumer data, and the advertising services it sells to merchants eager to stand out from the online crowd. Long before Amazon bought Whole Foods, Alibaba was investing in retail chains, including a Costco-like market called Sun Art, department-store operator Intime, electronics retailer Suning, and its own homegrown grocery chain named Hema Xiansheng.

By integrating offline and online retail, Alibaba wants to deliver products to shoppers by whatever route they prefer—ordered online and delivered home, pre-sorted for in-store pick up, or neatly displayed so consumers can touch and experience new brands in person.

Behind the scenes, Alibaba’s new retail strategy aims to digitize the entire supply chain, both online and offline, and collect more detailed consumer data. The ability to follow and analyze vast quantities of product and consumer data helps Alibaba eliminate inefficiencies with smart logistics, digital inventory management, anticipating evolving consumer trends and personalized shopper experiences.

MercadoLibre’s Evolution from eBay to Amazon

Ten years ago when investors called MercadoLibre the eBay of South America, they were halfway correct. CEO Marcos Galperin started the company in eBay’s image with his Stanford business school classmates in1999. They’ve since transformed the company from an internet auction site into Latin America’s leading online marketplace on par with Amazon.

Our Global Growth team sees two key ingredients to MercadoLibre’s early success: 1) a heavy emphasis on advanced technological infrastructure and, 2) tailoring its websites and payments services to fit South America. Understanding Latin America’s specific local context was key to avoiding the missteps eBay and Amazon made in China.

In its early days, MercadoLibre gave merchants the option of listing products at fixed or auction prices. It quickly discovered the majority preferred fixed prices. MercadoLibre also changed the way merchants interacted with buyers.

Shoppers couldn’t interact directly with sellers the way eBay allowed, because MercadoLibre rightly understood that would likely cut it out of the transaction entirely. Instead, it developed Q&A message boards, which buyers found helpful.

Over time, to attract more merchants to its busiest online marketplaces in Argentina, Brazil and Mexico, MercadoLibre developed logistical shipping solutions through its MercadoEnvios division, helping ensure merchant deliveries arrived on time for a better shopping experience. It also generated powerful synergies through MercadoPago, a payment services division.

It’s MercadoLibre’s push into new financial technologies that holds significant promise in our Global Growth team’s eyes. Half of Latin America’s population remains without bank accounts (or credit cards), and its economies are still largely cash-based. One side effect for cash-based entrepreneurs is that banks won’t issue working capital without a history of verified bank transactions.

MercadoLibre, on the other hand, has the data to determine creditworthiness by tapping into its online sales history and customer reviews. Spurned by banks, more merchants are turning to MercadoLibre for loans. Interest-free loans offer tremendous value to shoppers, given high interest rates in Latin America. This ease of doing business also increases customer loyalty.

These new approaches to financial services are one of the reasons our Global Growth team thinks MercadoLibre offers an efficient way to gain exposure to online retailing in South America. As more internet users migrate to online and mobile commerce in Latin America, we believe MercadoLibre has the opportunity to capture a majority of these shoppers.

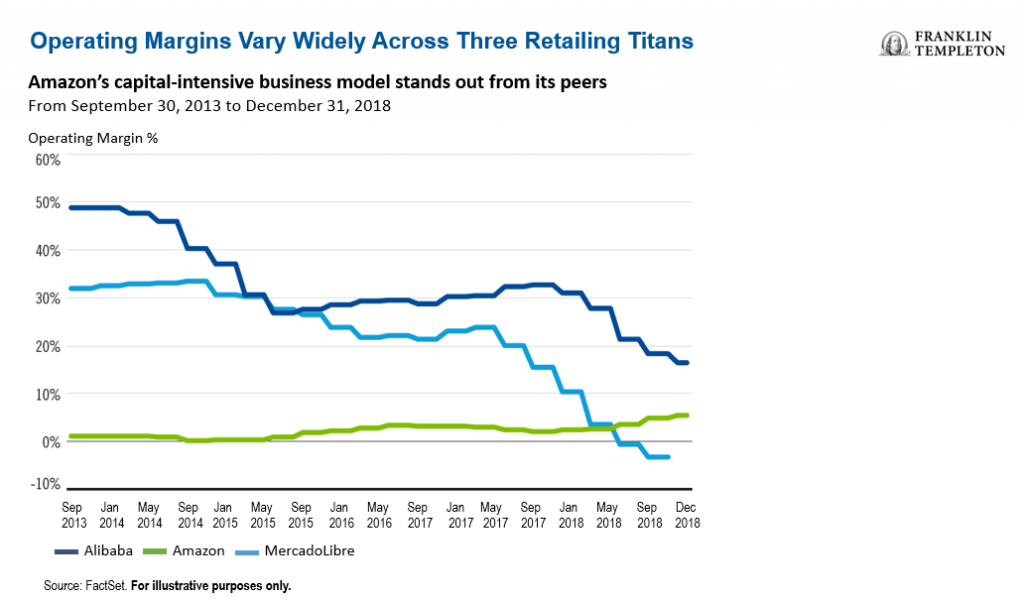

Pathways to Sustainable Cash Flows

Across our equity teams, we evaluated recent company operating margins side-by-side so we could compare and contrast each firm’s accomplishments from growth and value perspectives. What struck us right away was the impact Amazon’s capital-intensive business model has long had on its profit margins. Compared with Alibaba, Amazon looks anemic. Also noticeable are Alibaba’s declining margins and recent negative margins for MercadoLibre.

Amazon’s Profits Gain Momentum

Since going public, Amazon’s heavy investments in technology, logistics and new products have long dampened its operating income. Bezos must constantly balance between deploying capital to build future growth and holding back to boost near-term profits.

It’s for this reason our US Growth analysts think traditional valuation metrics like price-to-earnings and enterprise value/EBITDA aren’t good yardsticks for Amazon.5Simply put, these metrics aren’t a reliable snapshot of Amazon’s long-term profit potential, in our analysts’ views. Our US Growth analysts think Amazon’s margin expansion story is finally taking root.

Alibaba’s Data-Centric Ecosystem

Unlike Amazon’s recent positive profit momentum, Alibaba’s operating profits have faced headwinds from spending on businesses outside its core China retail marketplace. Agile competitors with deep pockets mean Alibaba needs to spend to keep existing customers happy and to lure new ones.

So how does Alibaba steer margins back in an expanding direction? Our Emerging Markets team sees a couple of avenues, starting with growing its cloud computing business in China. Alibaba also aims to help more brick-and-mortar retailers digitize their own back office supply chains through smart logistics, and by boosting front-end traffic by tapping into Alibaba’s deep pool of consumer data and cloud analytics. We see Alibaba less as a collection of e-commerce marketplaces and offline retail hubs, and more as a data-centric ecosystem that drives profits through digitization and technology, while generating better customer experiences.

MercadoLibre: Building Warehouses to Stay on Top

MercadoLibre is investing in shipping logistics and consumer incentives to shore up its commanding lead over competitors like Amazon. Taking a page out of Amazon’s playbook, MercadoLibre is building new warehouses to serve as cross-docking locations.

Costs to build these fulfillment centers, plus free shipping incentives, have taken a noticeable bite out of profit margins in the past year. Nevertheless, our Global Growth team is confident these investments can pay off by improving the customer experience and by attracting more merchants.

The Retail Revolution is Accelerating

The reality of today’s digitized marketplace means that not only has shopping changed dramatically in just a decade, the rate of change also continues to accelerate.

It’s now easier for shoppers to get tailored items and access products more quickly and conveniently than ever before. Technology pioneers like Amazon, Alibaba and MercadoLibre are largely responsible for setting new standards in the world’s biggest markets—continually improving customer experiences by anticipating their preferences, lowering prices and delivering items faster.

Plowing vast amounts of capital into new innovations (sometimes to the detriment of near-term profits), these companies are raising the bar for everyone by reshaping customer expectations. We believe each company bears close watching to understand where the retail landscape is heading next.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size and lesser liquidity. Investments in fast-growing industries like the technology sector (which historically has been volatile) could result in increased price fluctuation, especially over the short term, due to the rapid pace of product change and development and changes in government regulation of companies emphasizing scientific or technological advancement or regulatory approval for new drugs and medical instruments.

Important Legal Information

This commentary reflects the analysis and opinions of the authors as of February 14, 2019, and may differ from the opinions of other portfolio managers, investment teams or platforms at Franklin Templeton Investments. Because market and economic conditions are subject to rapid change, the analysis and opinions provided are valid only as of February 14, 2019, and may change without notice. Statements of fact are from sources considered reliable, but no representation or warranty is made as to their completeness or accuracy.

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The companies and case studies shown herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton Investments. The opinions are intended solely to provide insight into how securities are analyzed. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio. This is not a complete analysis of every material fact regarding any industry, security or investment and should not be viewed as an investment recommendation. This is intended to provide insight into the portfolio selection and research process. Factual statements are taken from sources considered reliable, but have not been independently verified for completeness or accuracy. These opinions may not be relied upon as investment advice or as an offer for any particular security. Past performance does not guarantee future results.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute. CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

1. Source: Varma N. “Amazon Versus Google Search: Who is Winning the Battle and How?” Marketing Technology Insights July 2018.

2. Source: The Guardian, “Jeff Bezos: I’ve made billions of dollars of failures at Amazon,” December 2014.

3. Source: Analysys International August 2007.

4. Sources: “China 3rd Party Mobile Payment Report.” iResearch 2017.

5. Price-to-earnings is a ratio for valuing a company that measures its current share price relative to its per-share earnings. Enterprise value is a measure of a company‘s total value, often used as a more comprehensive alternative to equity market capitalization. EBITDA, or earnings before interest, taxes, depreciation and amortization, is a measure of a company‘s overall financial performance and is used as an alternative to simple earnings or net income in some circumstances.

© Franklin Templeton Investments

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits