Let me start out by saying that I am all for any piece of advice which suggest individuals should save more. Saving money is a huge problem for the bulk of American’s as noted by numerous statistics. To wit:

“American have an average of $6,506 in credit card debt, according to a new Experian report out this week. But which expenses are adding to that balance the most? A full 23% of Americans say that paying for basic necessities such as rent, utilities and food contributes the most to their credit card debt. Another 12% say medical bills are the biggest portion of their debt.”

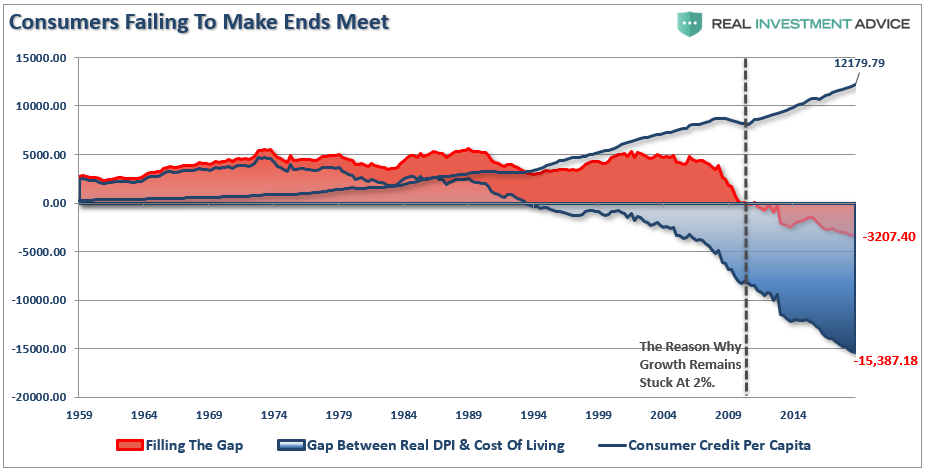

That $6500 credit card balance is something we have addressed previously as it relates to the ability of an average family of four in the U.S. to just cover basic living expenses.

“The ‘gap’ between the ‘standard of living’ and real disposable incomes is more clearly shown below. Beginning in 1990, incomes alone were no longer able to meet the standard of living so consumers turned to debt to fill the ‘gap.’ However, following the ‘financial crisis,’ even the combined levels of income and debt no longer fill the gap. Currently, there is a $3200 annual deficit that cannot be filled.”

This is why we continue to see consumer credit hitting all-time records despite an economic boom, rising wage growth, historically low unemployment rates.

Flawed Advice

The media loves to put out “feel good” information like the following:

“If you start at age 23, for instance, you only have to save about $14 a day to be a millionaire by age 67. That’s assuming a 6% average annual investment return.”

Or this one from IBD:

“If you’re earning $75,000, by age 40 you need 2.4 times your income, or $180,000, in retirement savings. Simple as that.” (Assumes 10% annual savings rate and a 6% annual rate of return)

See, it’s easy.

Unfortunately, it doesn’t work that way.

Let’s start with return assumptions.

Markets Don’t Compound

I have written numerous times about this in the past.

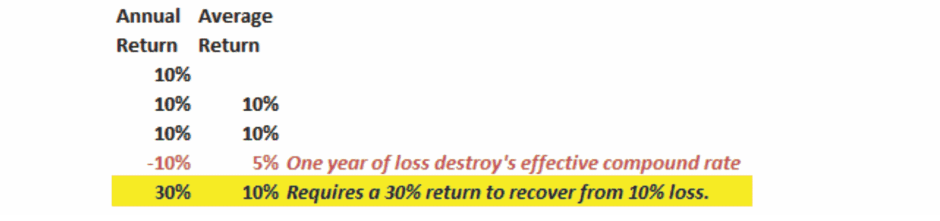

“Let’s assume an investor wants to compound their investments by 10% a year over a 5-year period.

The ‘power of compounding’ ONLY WORKS when you do not lose money. As shown, after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required. In reality, chasing returns is much less important to your long-term investment success than most believe.”

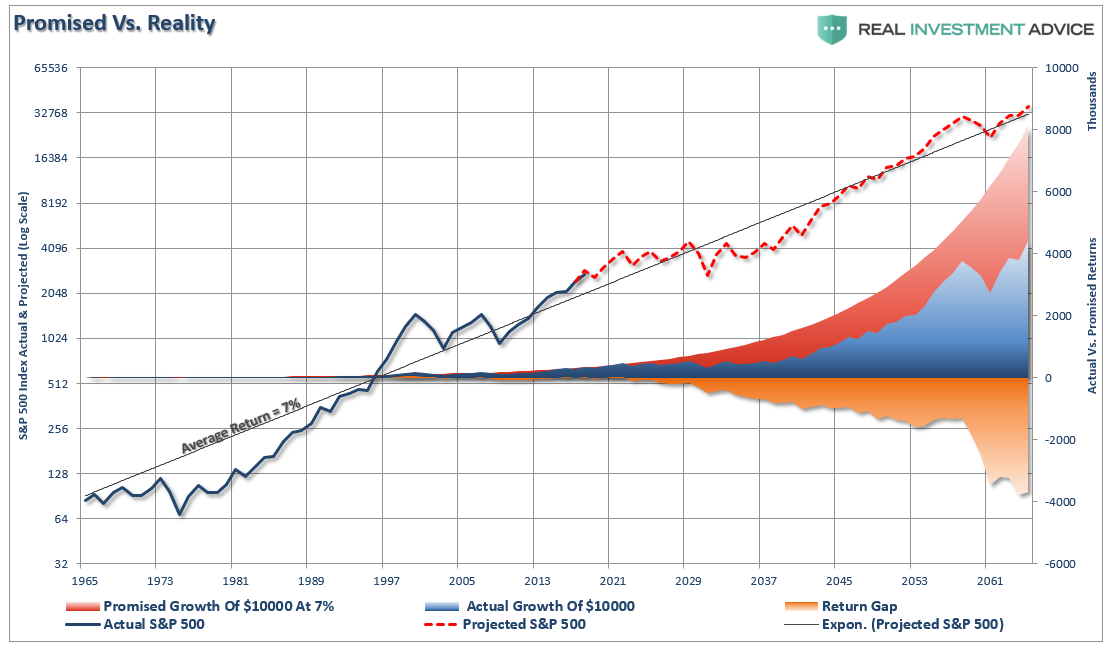

When imputing volatility into returns, the differential between what investors were promised (and this is a huge flaw in financial planning) and what actually happened to their money is substantial over long-term time frames.

Here is another way to look at it.

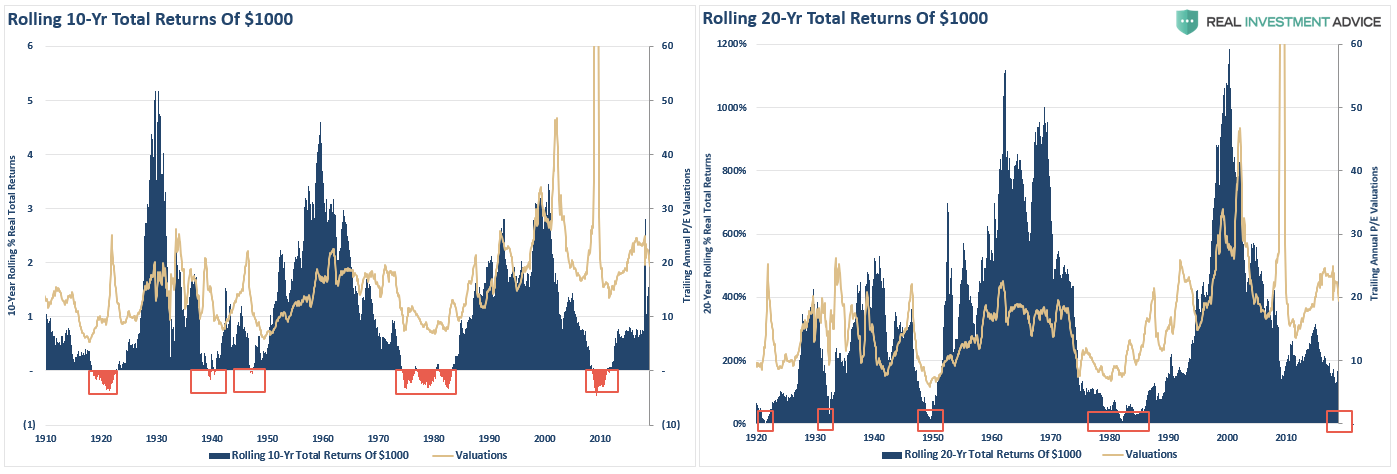

If you could simply just stick money in the market and it grew by 6% every year, then how is it possible to have 10 and 20-year periods of near ZERO to negative returns?

The level of valuations when you start your investing journey is all you need to know about where you are going to wind up.

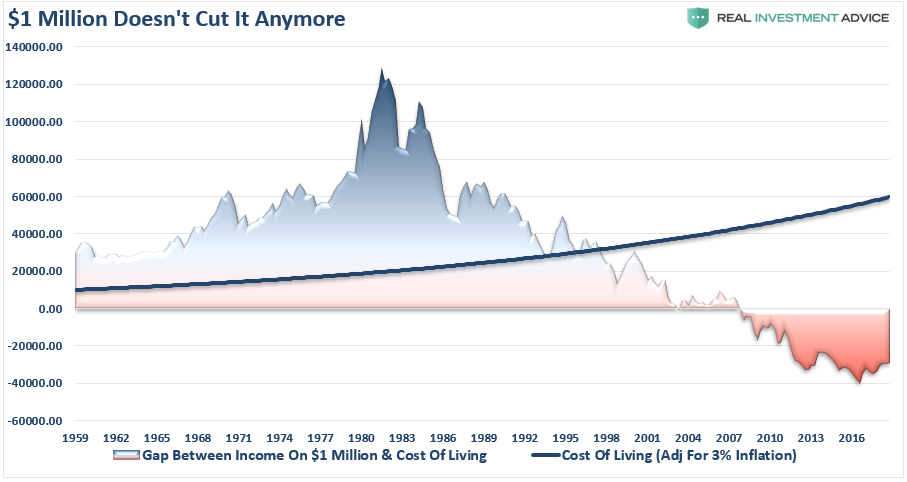

$1 Million Sounds Like A Lot – It’s Not

I get it.

$1 million sounds like a whole lot of money. It’s a nice, big, round number with lot’s of zeros.

In 1980, $1 million would generate between $100,000 and $120,000 per year while the cost of living for a family of four in the U.S. was approximately $20,000/year.

Today, there is about a $40,000 shortfall between the income $1 million will generate and the cost of living.

This is just a rough calculation based on historical averages. However, the amount of money you need in retirement is based on what you think your income needs will be when you get there and how long you have to reach that goal.

If you are part of the F.I.R.E. movement and want to live in a tiny house, sacrifice luxuries, and eat lots of rice and beans, like this couple, that is certainly an option.

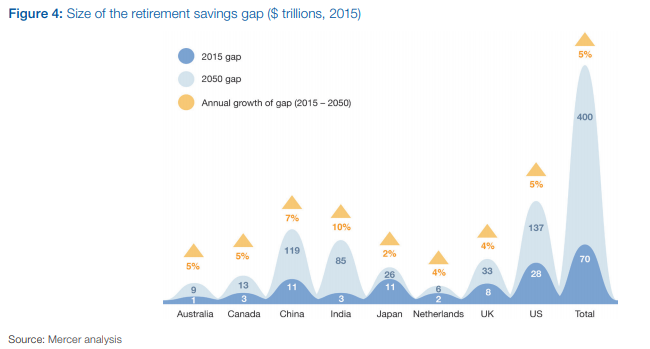

For most there is a desire to live a similar, or better, lifestyle in retirement. However, over time our standard of living will increase with respect to our life-cycle stages. Children, bigger houses to accommodate those children, education, travel, etc. all require higher incomes. (Which is the reason the U.S. has the largest retirement savings gap in the world.)

If you are in the latter camp, like me, a “million dollars ain’t gonna cut it.”

Don’t Forget The Inflation

The problem with all of these “It’s so simple a cave man could do it” articles about “save and invest your way to wealth” is not only the variable rates of returns discussed above, but impact of inflation on future living standards.

Let’s set up an example.

- John is 23 years old and earns $40,000 a year.

- He saves $14 a day

- At 67 he will have $1 million saved up (assuming he actually gets that 6% annual rate of return)

- He then withdraws 4% of the balance to live on matching his $40,000 annual income.

That pretty straightforward math.

IT’S ENTIRELY WRONG.

The living requirement in 44 years is based on today’s income level, not the future income level required to maintain the current living standard.

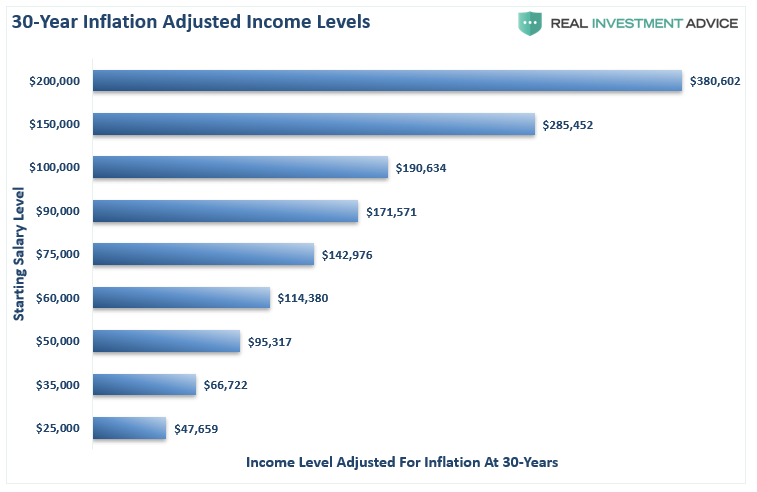

Look at the chart below and select your current level of income. The number on the left is your income level today and the number on the right is the amount of income you will need in 30-years to live the same lifestyle you are living today.

This is based on the average inflation rate over the last two decades of 2.1%. However, if inflation runs hotter in the future, these numbers become materially larger.

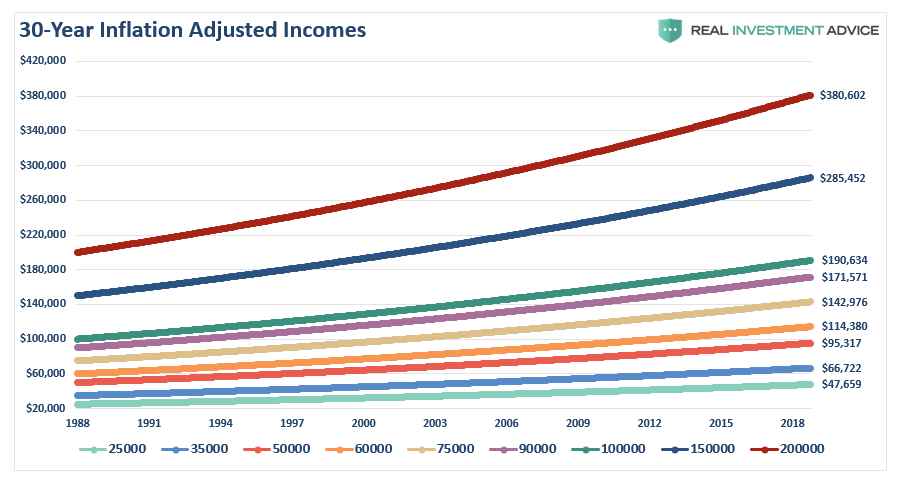

Here is the same chart lined out.

The chart above exposes two problems with the entire premise:

- The required income is not adjusted for inflation over the savings time-frame, and;

- The shortfall between the levels of current income and what is actually required at 4% to generate the income level needed.

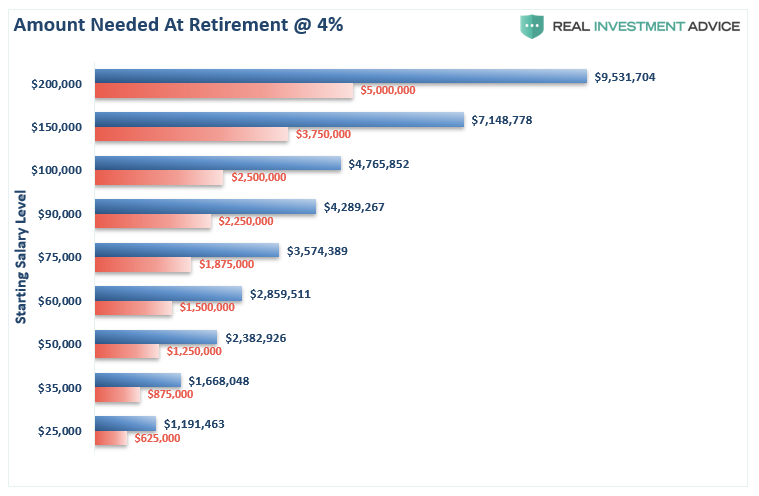

The chart below takes the inflation-adjusted level of income for each brackets and calculates the asset level necessary to generate that income assuming a 4% withdrawal rate. This is compared to common recommendations of 25x current income.

If you need to fund a lifestyle of $100,000 or more today. You are going to need $5 million at retirement in 30-years.

Not accounting for the future cost of living is going to leave most individuals living in tiny houses and eating lots of rice and beans.

Things You Can Do To Succeed

The analysis reveals the important points young investors should consider given current valuation levels and the reality of investing over the long-term:

-

Pay yourself first, aggressively. Saving money is how you pay yourself for working. 30% is the real magic number.

- It’s all about “cash flow.” – you can’t save if you spend more than you make and rack up debt. #Logic

-

Budget – it’s a four-letter word for most Americans, but you can’t have positive cash flow without it.

- Get off social media – one of the biggest impacts to over-spending is “social media” and “keeping up with the friends.” If advertisers were not getting your money from social media ads they wouldn’t advertise there. (Side benefit is that you will be mentally healthier and more productive by doing so.)

-

Pick up a side hustle, or two, or three – Once you drop social media it will free up 4-6 hours a week, or more, with which you can increase your income. There are tons of apps today to let you earn extra money and “No” it’s not beneath you to do so.

- Get out of debt and stay that way. No, you do not need a credit card to build credit.

-

If you can’t pay cash for it, you can’t afford it. Do I really need to explain that?

- Future inflation expectations must be carefully considered.

- Expectations for compounded annual rates of returns should be dismissed

Don’t misunderstand me….I love ANY program that encourages individuals to get out of debt, save money, and invest.

Period. No caveats.

There is one sure-fire way to go from “being broke” to being “rich” – write a book on how to do it and sell it to broke people. (See “Broke Millennial” and “Millennial Money.”– but hey that’s capitalism and you can do it too.)

But, if investing were as easy as just sticking your money in the market, wouldn’t “everyone” be rich?

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

© Real Investment Advice

© Real Investment Advice

More Factor-Based Investing Topics >