Real Investment Advice

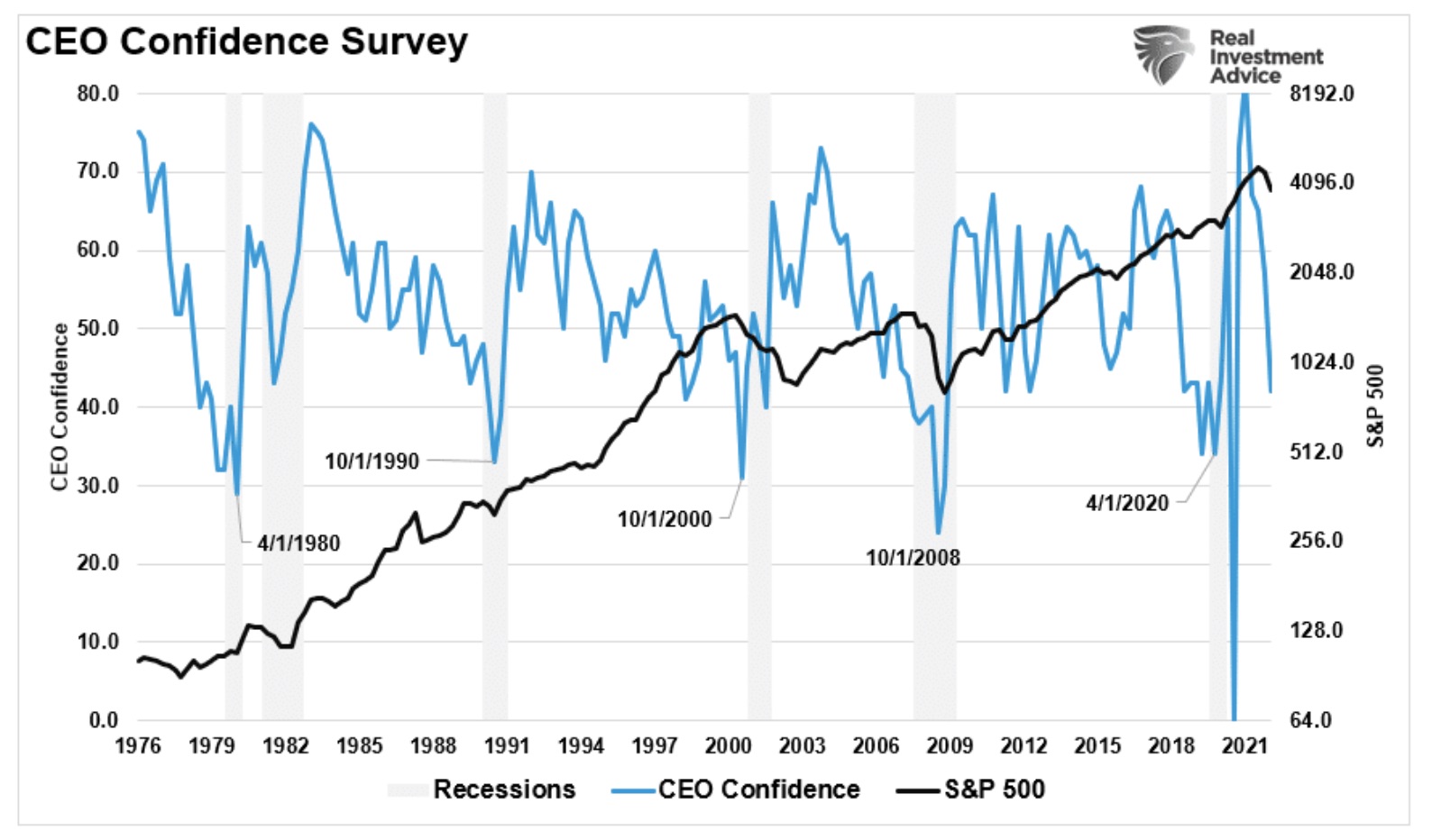

Spotting Market Bubbles: Why History Says It’s Nearly Impossible

If you knew you were standing inside a stock market bubble, you wouldn’t be standing in it for long. You’d sell. So would I, and so would everyone reading this. And if spotting market bubbles was something everyone could do in real time, the bubble couldn’t form in the first place.

AI Capex Risk Cuts Both Ways In The American Economy

The AI capex risk profile has gotten sharper since then, and the argument needs tightening in a few places. The bull case and the tail risk are now the same buildout, but they are running in different directions.

Margin Debt Risk: The Ratios That Mislead Investors

Rising prices increase the value of collateral in every margin account, which automatically increases how much each investor can borrow under Reg T. Debt rises BECAUSE the market rose, not the reverse. That single fact is what breaks the ratios we’re about to examine, and it lies at the core of why margin debt risk is so often misjudged.

Wage Growth As A Leading Inflation Indicator

Wage growth peaked four years ago. Since 1985, it has led CPI by three to seventeen months in every single cycle. The May 4.2% inflation print is the noise. Watch the wages.

Record Retail Inflows: Where Is All The Money Coming From?

The money is REAL. The question was never whether it exists. It’s who’s spending it, and what they borrowed to do it. When the wall of cash and the bottom half finally commit to risk at the same moment the Fed turns hawkish, that’s not the start of something. That’s the part of the cycle where the careful investor gets paid to be careful.

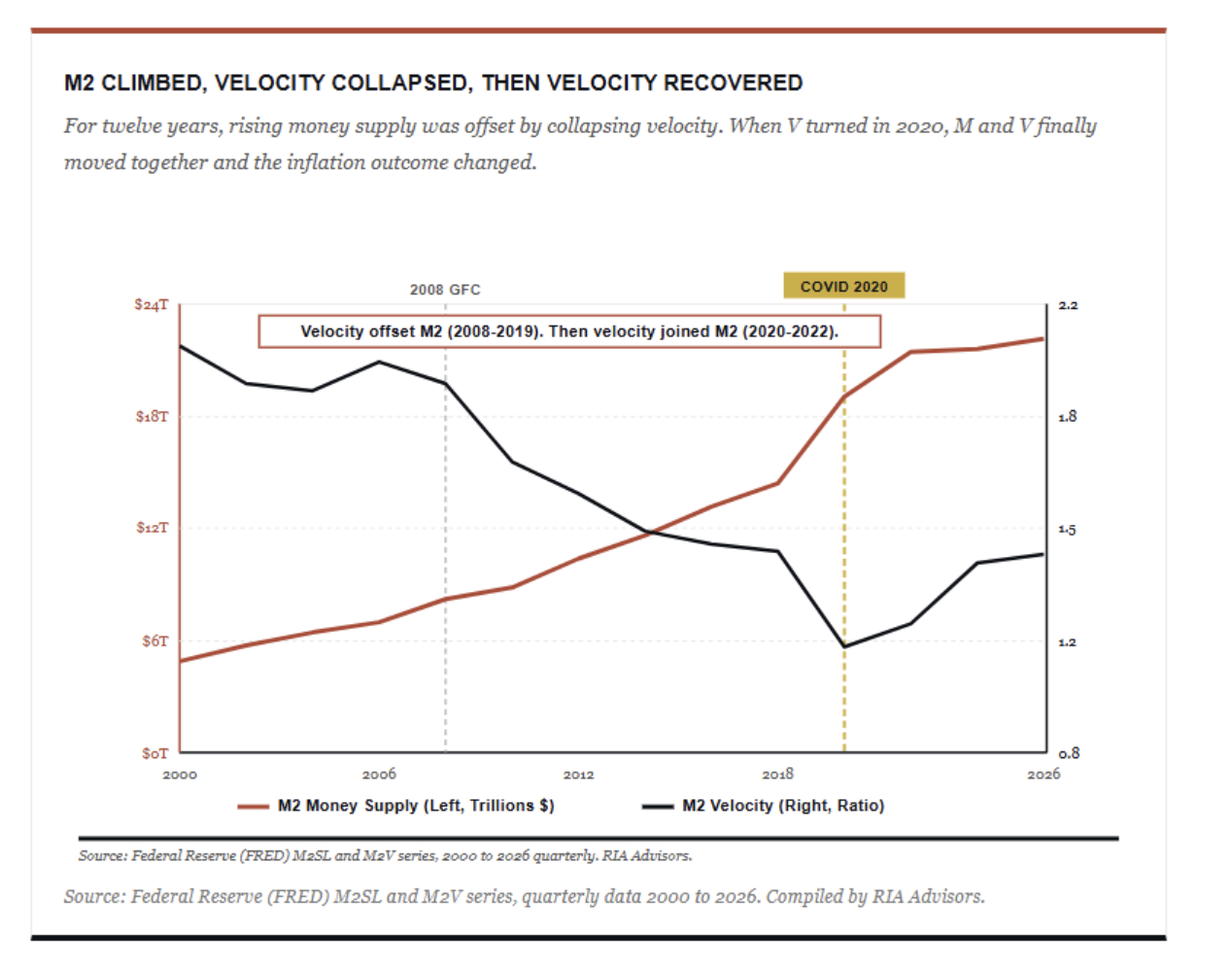

Friedman Was Right, Just Mostly Misquoted.

Friedman was reasoning from the equation of exchange, MV = PQ. Money times velocity equals prices times real output. It’s an identity, not a theory. Where it gets interesting is when you ask which variable does the work.

When Flows Meet a Hawkish Fed

Here’s the setup most investors are underrating right now. Over the next two weeks, the tape will trade on plumbing rather than fundamentals. We just cleared the largest options expiration in history. Quarter-end pension selling comes next, and then July 1 reopens the passive-money firehose into a market that already routes forty cents of every S&P 500 dollar into ten stocks.

The Consumer Sentiment Disconnect From Economic Reality

Start with the disconnect itself. If you only looked at the Michigan headline, you’d assume the country was in a depression. However, when you look at what people are actually doing, the picture changes completely.

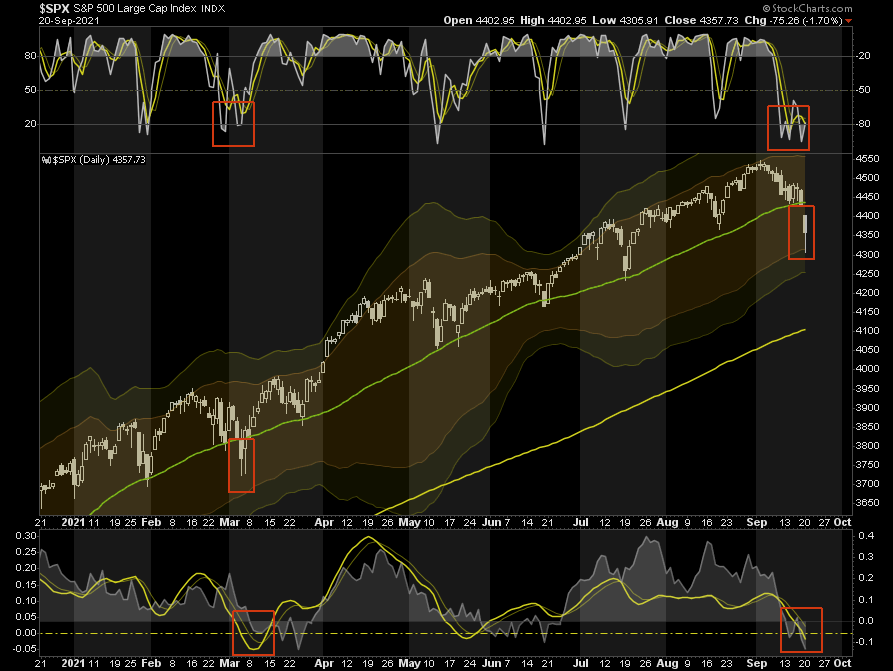

Bull Market Pullback: Why The 4.5% Dip Held The 50-DMA

The catalyst that turns a healthy pullback into something deeper won’t be a single oil-soaked CPI print. It’ll be the moment forward earnings expectations start to roll over while valuations sit at the high end of history. We aren’t there yet.

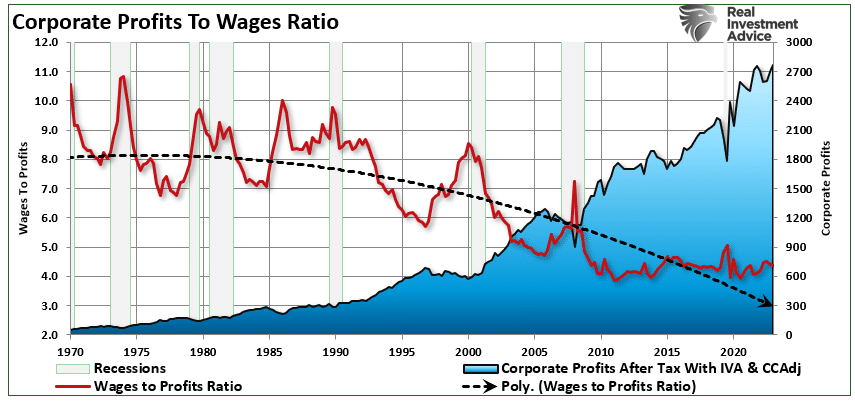

The K-Shaped Economy: Why The Middle Class Moved Up.

The K-shaped economy has become shorthand for a tidy story. The rich pull away while everyone else falls behind. It fits the mood, and it makes for a sharp headline. The problem is that it’s mostly wrong.

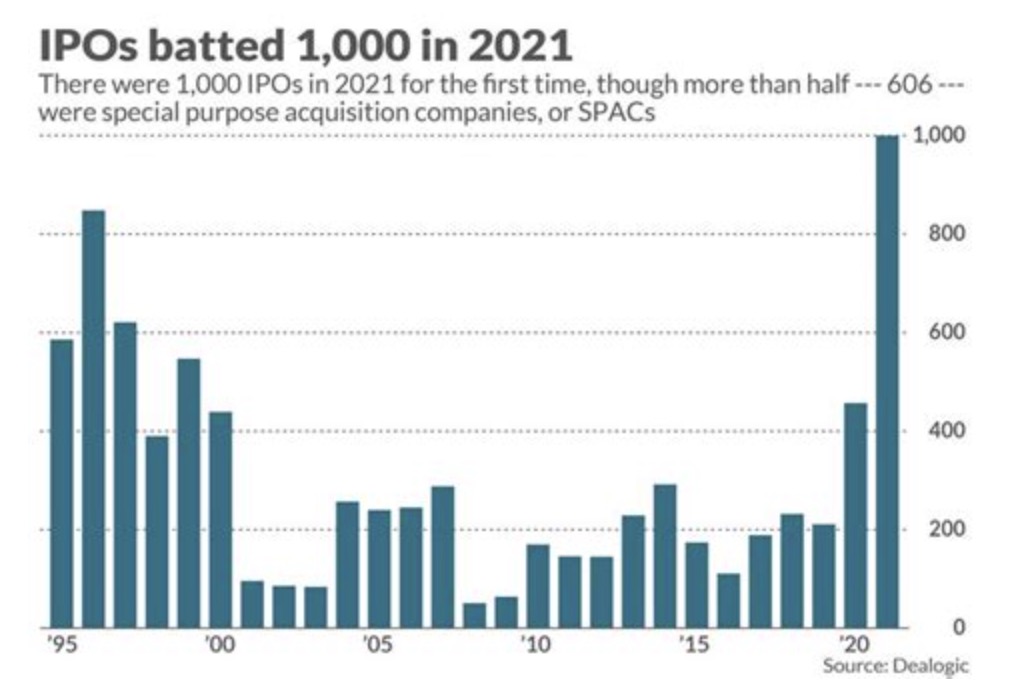

Equity Supply Surge: What Historically Comes Next

This past week, the market hit an all-time high. At the same time, Alphabet (GOOG) told investors it would raise $80 billion by selling stock to fund its AI buildout, and the shares fell about 4% on the news.

Stronger Dollar Trade: The Most Unexpected Macro Bet (Part 2)

In Part 1, we explored why Dollar Dominance Remains Alive and Well. Today, we will explore the stronger-dollar trade, the one macro trade that nobody is sized for.

Risk Management For Retirees: When To Reduce Exposure

Reducing equity exposure during periods of elevated risk is not the same as market timing. The financial industry has spend decades blurring that distinction.

Dollar Dominance Remains Alive And Well (Part 1)

The dollar is supposed to be dying. We’ve heard that argument for the better part of a decade, and it’s getting louder, not quieter. Dollar dominance isn’t fading. In fact, the events of late April 2026 just delivered the loudest counter-signal in years.

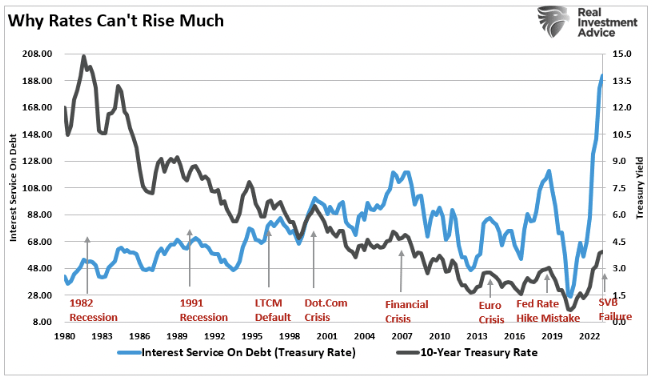

Rising Interest Rates: Why The Narrative Fails Against The Data

Last Friday closed with the 10-year Treasury yield at 4.60%, a one-year high, and the doom commentary about rising interest rates was waiting before the bell even rang. Hyperinflation. Bond market breakdown. Paradigm shift. A 1981 fair-value retest.

Buffett Cash Hoard: Why $397 Billion Sits On The Sidelines

That Buffett cash hoard has also created a lot of speculation, innuendo, and assumptions, which is what I want to walk through in today’s discussion. Primarily, what that cash hoard actually represents, the popular theories explaining it, and what it really costs shareholders to hold.

The Stagflation Narrative: What Doomers Get Wrong – Part II

The stagflation narrative dominating financial social media isn’t completely wrong. That’s what makes it so dangerous. After more than 30 years of managing client portfolios through actual inflationary cycles, not watching them on YouTube, I’ve learned that the most damaging investment advice isn’t built on outright lies.

Parabolic Semiconductor Rally Is Pricing In 2028 Already

A real fundamental story doesn’t require a parabolic chart to validate it. In fact, fundamentals tend to drag prices up the trend line, not push them through the ceiling. When a “shortage” narrative arrives at the same moment that the worst-quality names in the sector are leading the index higher, that’s not fundamentals at work.

Commodity Supercycle: The Enemy Of The Bull Thesis (Part 1)

That skepticism isn’t contrarianism for its own sake, but rather the recognition that when a thesis achieves consensus, the crowd has usually already priced the easy part of the move, and the hard part is what comes next.

Market Correction Risk: Why Summer 2026 Looks Risky

The S&P 500 hit a fresh record high last week. The median stock in the index is sitting 13% below its 52-week peak. That divergence is not a footnote or a curiosity.

A Robot Economy: Who Gets Rich, Who Gets Left Behind

Robots are coming to the economy. It is inevitable, really, and there is nothing that will stop it. At some point in the not-so-distant future, robots will infiltrate every aspect of our lives, from office work and manufacturing to service work and trade skills, and even your home. Here are some numbers for you.

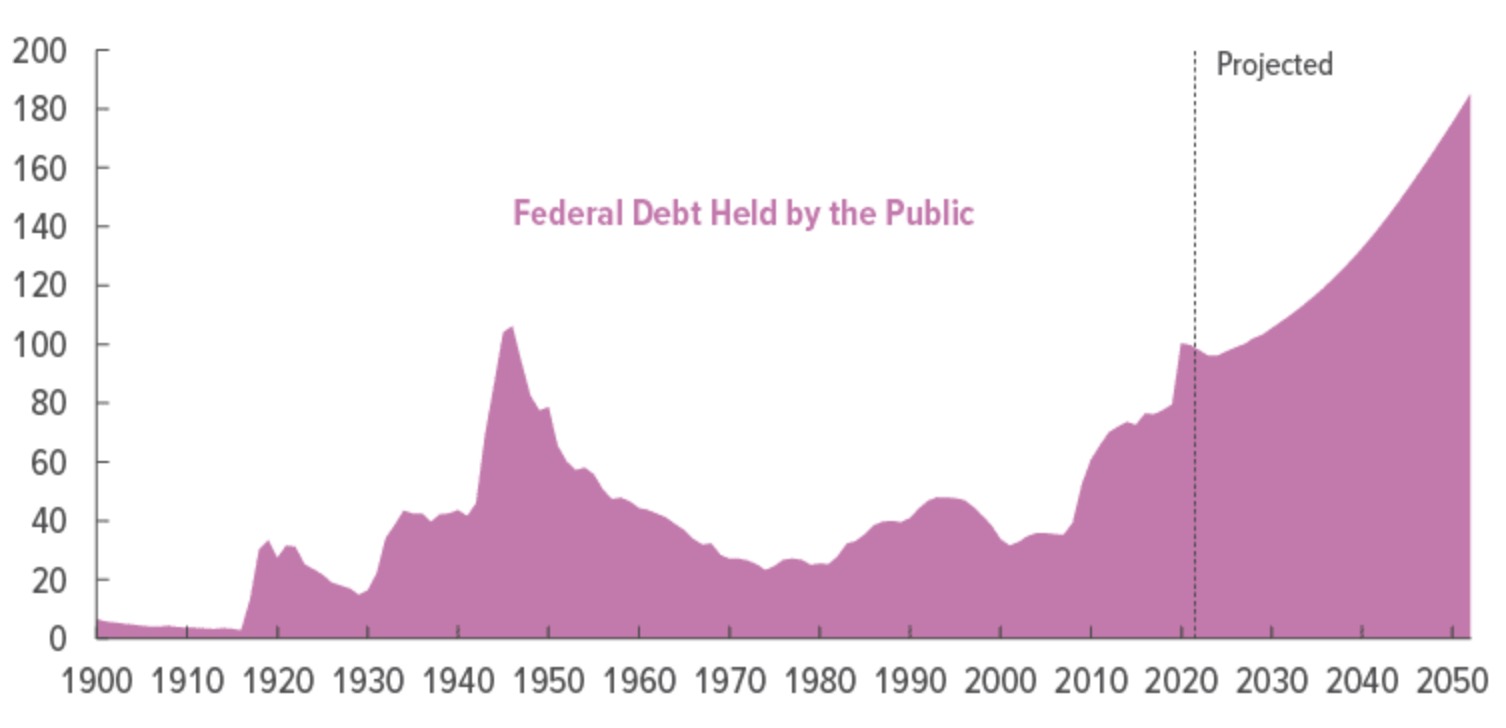

Government Debt: Not What The Doom Crowd Thinks It Is

Here’s where I want to start, because this is the point that almost every government debt analysis, including the article we’re responding to, completely ignores. Government debt doesn’t disappear into a void. By definition, if the Government borrows capital from someone, that capital must flow somewhere.

Hormuz: Why Markets Are Shrugging Off The Oil Shock

As of this writing, the Strait of Hormuz remains effectively closed since February 28. Roughly 20% of the world’s seaborne oil stopped moving through the chokepoint. T

Why Panic is a Costly Mistake

The stock market selloff between February 28 and April 14 produced one of the more instructive market lessons in recent memory. It isn’t because of what the market did, but because of what investors did in response.

BLS Jobs Report Is Broken. Is There A Better Measure?

The BLS jobs report has become so distorted that it often tells us almost nothing reliable about the actual state of employment. I realize that is a serious claim, but let me back it up with the data. I want to show you what I believe is a simpler, more honest alternative.

S&P 500 Outlook: The 8.2% Rally & What Comes Next

Over the last few weeks, we have published real-time market commentary as the correction proceeded. The goal was to help investors navigate the more dire outcomes promoted on social media. A largely unexpected outcome was that the S&P 500 outlook changed dramatically in a matter of days.

Oil Shock: Will The Fed Intervene (Part 2)

That article digs into the plumbing behind oil shocks and recession, and exposes why, over the years, I’ve learned to distrust the loudest voices in the room.

The Stock Market Rally: Buy Or Fade It?

Last week, the stock market rally was one of the best performances in nearly a year. The S&P 500 surged 3.4%, the Nasdaq climbed 4.4%, and the bulls declared the correction over. As I have stated before, having watched markets for more than 35 years, I have come to recognize the difference between a relief rally and the end of a corrective cycle.

Rubino: Fiat Currencies Are In A Death Spiral

The fiat currency collapse narrative is one of the most emotionally satisfying arguments in all of financial punditry. It feels intellectually rigorous, draws on genuine history, and speaks to deep and legitimate anxieties about government overreach, monetary recklessness, and the long-term consequences of unlimited debt creation.

Stock Market Breadth: Warning Or Opportunity?

What’s unusual today is the degree of divergence between individual stocks and the cap-weighted index. When a handful of stocks carry enough weight to paper over widespread internal damage, investors holding diversified portfolios feel the pain long before the headlines acknowledge it.

The Dollar’s Plumbing: Conspiracy vs. Data

Every few months, a headline appears declaring that the U.S. dollar’s reign as the world’s reserve currency is over. China is dumping Treasuries. Central banks are hoarding gold.

The 200-DMA Just Broke: What Every Investor Should Know

Last week, on March 19th, the S&P 500 closed below its 200-DMA for the first time since May 2025. The first instinct is to panic as media headlines talk about bear markets and financial crisis events. However, as we will explore today, the data says it depends entirely on the type of break: sustained or brief.

Treasury Bond Yields Don’t Lie: But Wars Don’t Drive Them

This past weekend, Adam Taggart and I discussed what happens to Treasury bond yields when the United States enters a military conflict. The conventional wisdom is reflexive and tidy.

Soros CEO & CIO Warns of a Reckoning

The private equity (PE) business is huge. When I say huge, I mean $4.4 trillion huge. However, as we warned then, the risks have come home to roost. The private equity and private credit industry is heading into a gut-wrenching period of consolidation.

USD Stable Coins And The Rebasement Of The US Dollar

The “fiat is dying” argument has become a catchphrase narrative among digital asset bulls, gold bugs, and cryptocurrency advocates. That narrative’s core is that central banks have printed vast amounts of money.

Technical Deterioration: Risk Management Is Key

The S&P 500 closed at 6,740 on Friday, its lowest level since mid-December, as technical deterioration, collapsing payrolls, and $100 oil converged on the charts. Every major moving average has broken. Here’s what comes next.

SaaS: Is There Opportunity In The Destruction?

If the SaaSpocalypse narrative proves to be more panic than prophecy, the critical task becomes identifying which companies will emerge stronger.

Economic Sentiment Belies Strong Economic Estimates

Economic growth metrics for the United States have recently shown surprising resilience; however, consumers’ economic sentiment has not. According to the Bureau of Economic Analysis’s advance estimate, real Gross Domestic Product expanded at an annualized rate of just 1.4%.

Money: The 10 Immutable Laws Of Building Wealth

Money – everybody wants it, but few actually have it. As shown in recent financial statistics, the “wealth gap” in America continues to grow between the “haves” and the “have-nots.”

Is China Really Dumping US Treasuries?

“China is dumping US Treasuries to get out of the dollar.” This claim has been circulating the mainstream feeds lately, with the narrative that the “end of the dollar is near,” or “the US will lose its funding base,” and “bond yields will surge.” But are those claims valid? Such is what we will explore in more detail.

Financial Nihilism & The Trap Young Investors Are Walking Into

The article from the Wall Street Journal titled “Why My Generation Is Turning to Financial Nihilism” by Kyla Scanlon argues that Gen Z is embracing high-risk financial behavior out of despair and detachment, but the data shows something very different.

Market Sector Review: Extreme Market Bifurcation

Since the beginning of the year, we have discussed the “reflation trade” and its impact on specific market sectors. This past weekend’s newsletter also showed some of these more extreme returns in various market sectors since the beginning of the yea

The Reflation Narrative

The market got off to a strong start in 2026, with investors chasing industrials, materials, and commodity-related stocks as the reflation narrative gained traction. The “reflation narrative” is the belief that a range of policies will boost the rate of economic growth in the U.S. without triggering inflation.

Speculative Narrative Unwinds

For nearly two years, markets were driven by the same speculative narrative that “this time is different.” Speculative narratives are not only seductive but also contribute to investment behaviors that obscure reality. Speculation disguised as investing is a losing proposition.

The Market Cycles Potentially Driving 2026 Returns

Market cycles are once again at the center of the investment narrative as we head into 2026. The optimism is familiar as earnings held up in 2025, the economy avoided recession, and big tech lifted the indexes. However, those victories are already reflected in the price.

Mainstream Expectations: Hope Vs. Potential Risk

Mainstream expectations, those from Wall Street, economists, and corporate strategists, have congealed around a bullish economic outlook for 2026. Most forecasts project stronger economic growth, with contained inflation, and continued investment in technology and capital expenditure.

The Bullish And Bearish Case For 2026

By assessing the macro and market drivers that shape each outlook, we can lay out clear, practical tactics to prepare your portfolio for either path. Whether the bullish or bearish case prevails in 2026, your edge will come from disciplined risk management, not from guessing the future.

The South Park Market Of 2026

It is critical to understand that 2026 will not deliver certainty. Instead, investors should focus and make decisions based on probabilities backed by data, earnings trends, policy shifts, and macro signals.

AI Productivity, Employment and UBI

AI productivity gains will demand active solutions, not government gifts. Skill development, apprenticeships, employer-based training, wage insurance, and mobility support. These tools address displacement directly, while UBI does not.

2026 Earnings Outlook: Another Year of Optimism

The Wall Street consensus forecast for 2026 earnings growth is strong by historical standards. Analysts are giddy and projecting another year of double-digit growth in S&P 500 earnings per share (EPS).

New Year’s Resolutions For 2026 – Investor Version

The goal isn’t to be perfect; it’s to make fewer mistakes than last year because investing success doesn’t come from reading motivational quotes or watching market TikToks at midnight.

Precious Metals Aren’t Predicting Economic Collapse

In 2025, the prices of precious metals rose sharply, with silver prices recently surging past $80 per ounce. Of course, when precious metals rise, there is always the same group of commentators (mostly paid newsletter writers and physical metal dealers) to declare that a financial analysis is underway.

The Market Risk in 2026 if Growth Projections Fail

There is a rising market risk in 2026 that is largely overlooked as we wrap up this year. Optimism about 2026 is running high. Currently, investors are pricing in strong economic growth, robust earnings, and a smooth path of disinflation. Notably, Wall Street estimates suggest a significant acceleration in corporate profits...

2026 Market Outlook Based On Valuations

It’s that time of year when Wall Street polishes up its crystal balls and begins predicting returns for 2026. Since Wall Street never predicts a down year, which would be unwise for fee-based product revenues, these forecasts are often inaccurate and sometimes significantly wrong. Let’s review some previous years.

What Inflation Alarmists Missed In Their Warnings

Over the last couple of years, inflation alarmists such as Paul Tudor Jones, James Grant, and Jeff Gundlach have all said that inflation is returning with force. In different ways, they each stated that they would not own Treasury bonds due to the expectation that inflation would rise as the dollar declined due to the ongoing deficits.

Bull Market Genius Is A Dangerous Thing

During extended upward-trending markets that reward risk-takers and punish caution, everyone is a “bull market genius.” That dynamic flips investor psychology and, over time, creates a false sense of control.

Does AI Capex Spending Lead To Positive Outcomes?

As someone who views corporate finance through a pragmatic lens, I’ve been closely watching the current surge in capital expenditures (capex) tied to artificial intelligence (AI). When a company spends massive amounts of free cash flow and takes on increasing debt, does that lead to a positive outcome for investors?

Jobs Data From Alternative Sources May Drive Fed’s Next Move

Due to the federal government shutdown, official jobs data remains incomplete, forcing the Federal Reserve to rely on alternative private-sector reports to gauge the labor market. These alternative data sources, such as the ADP report and Revelio Labs estimates, indicate a widespread and concerning slowdown in employment, with job creation stalling, openings shrinking, and layoffs rising across many sectors.

A Bear Market is a Good Thing

In today’s markets, mentioning the “B-word” will get you thrown into the “permabear” camp, and everyone immediately assumes you mean the end of the world: death, disaster, and destruction. Yes, bear markets have terrible short-term impacts, but they also allow the system to reset for healthier growth in the future.

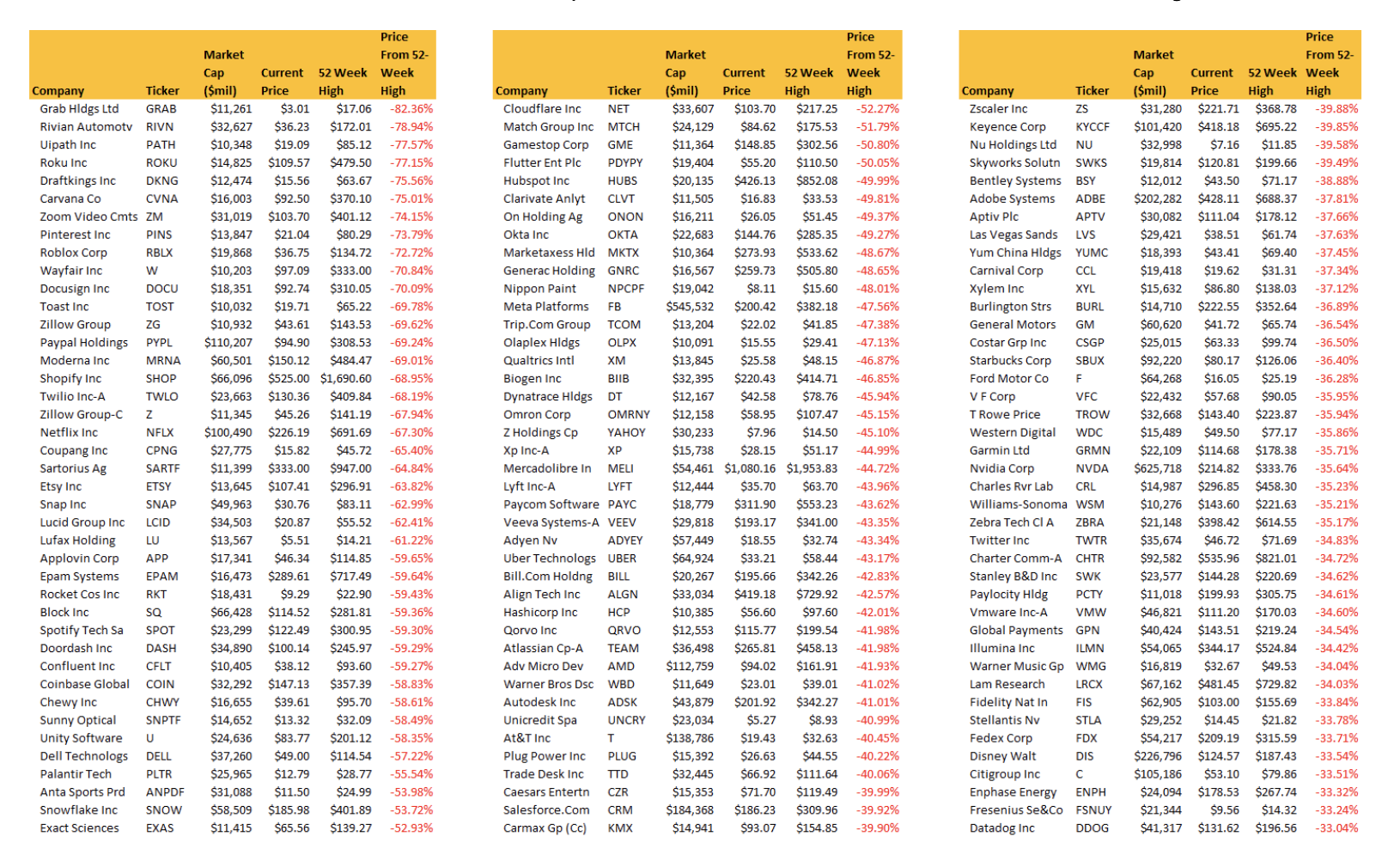

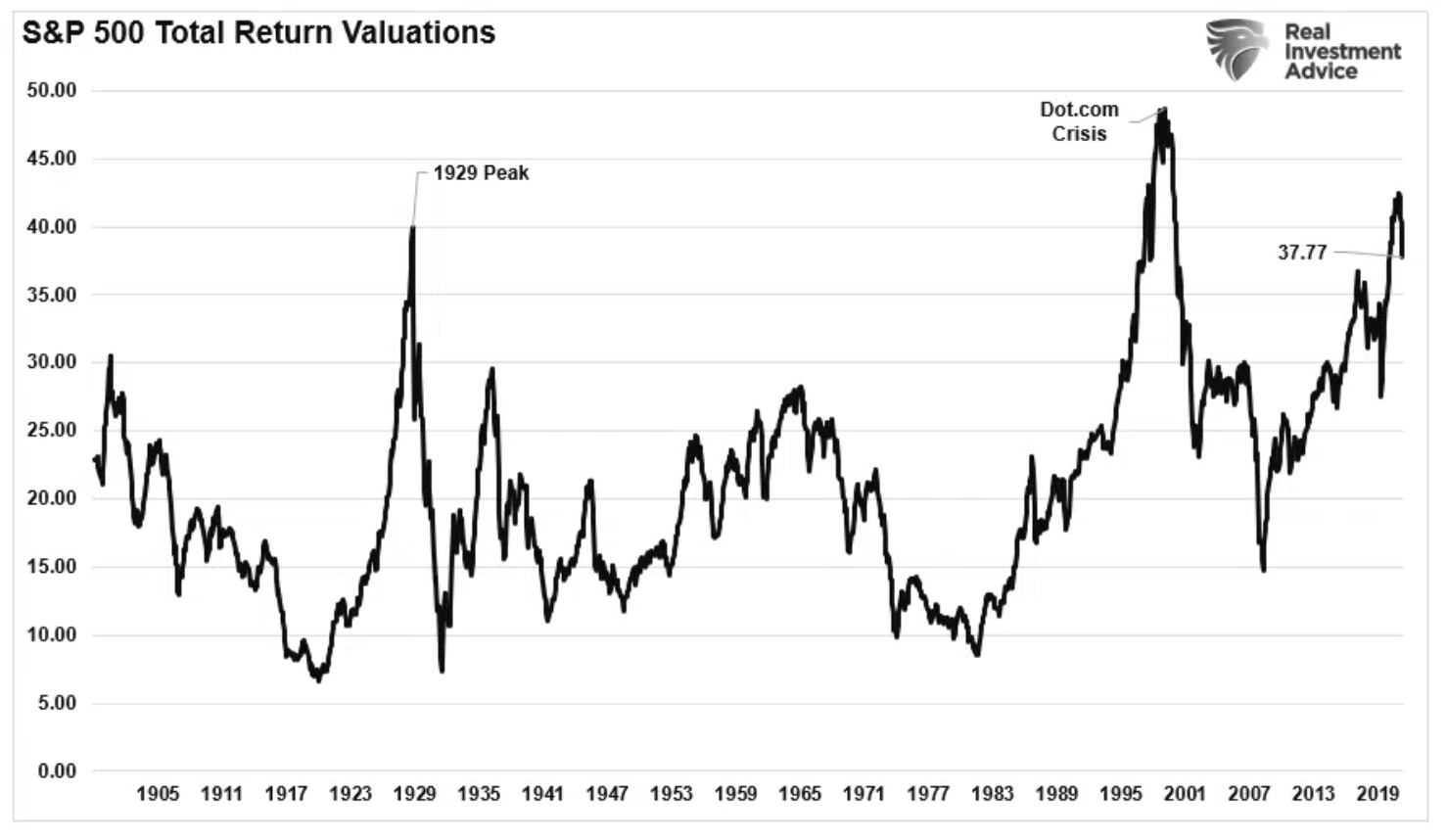

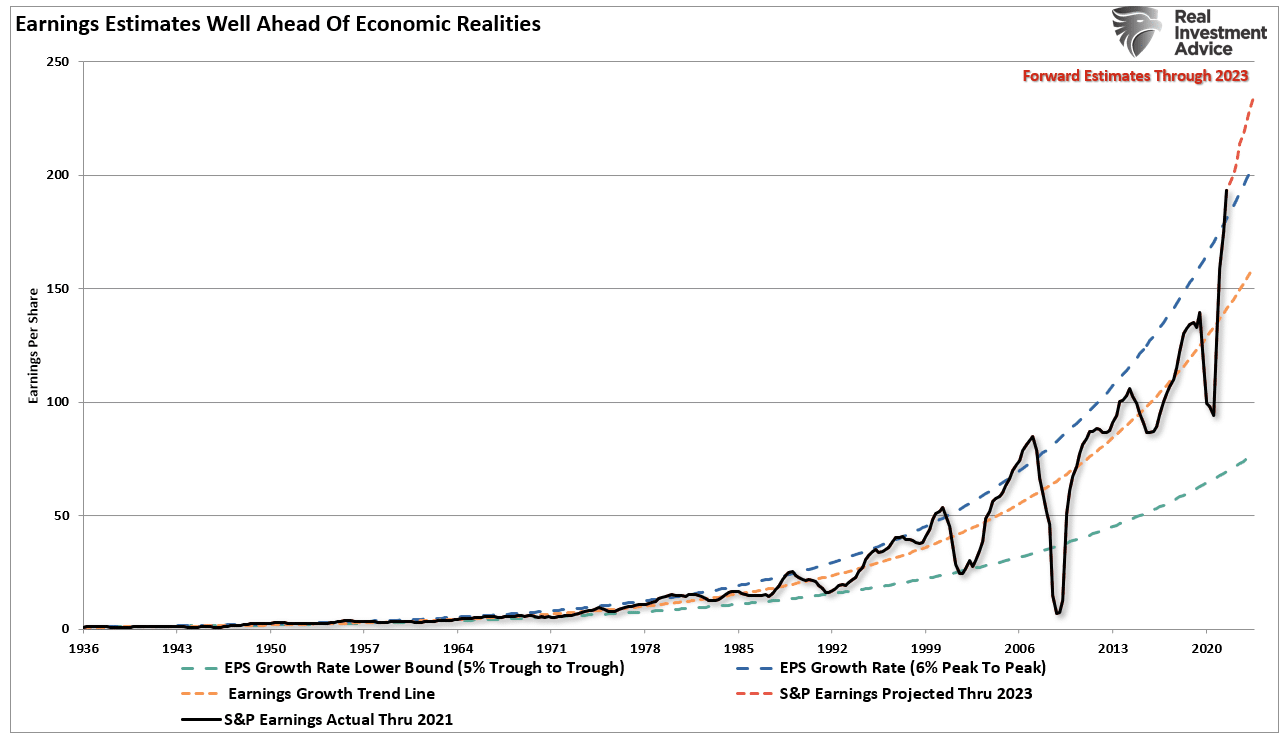

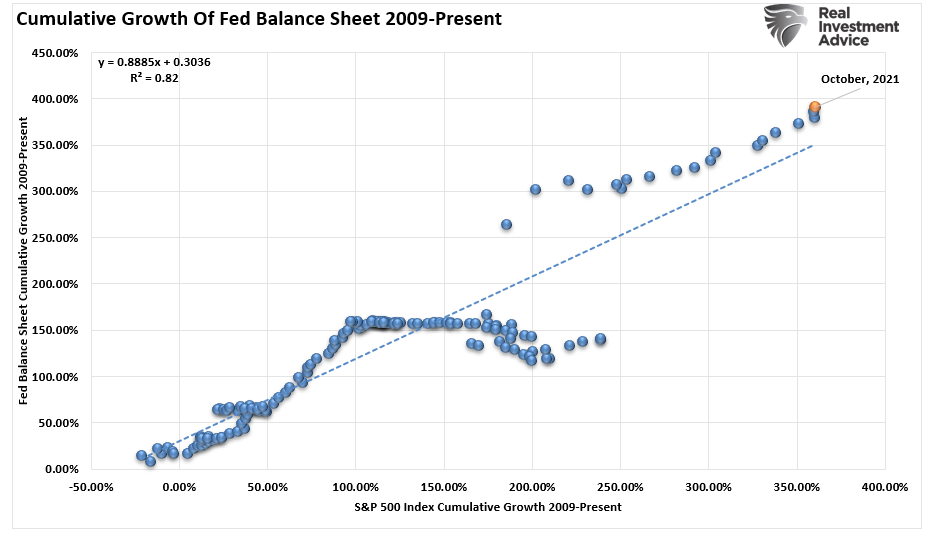

Market Bubbles: A Rational Guide To An Irrational Market

Yes, we may be in the second market bubble of this century. Alternatively, the market may be pricing in a shift as fundamental as the transition to either electricity or the internet. Either way, investors must think clearly, act deliberately, and avoid the kind of blind speculation that turned past booms into bloodbaths.

Capex Spending On AI Is Masking Economic Weakness

The U.S. economy’s recent growth has a distinctive engine: large‑scale capital expenditures (capex) tied to artificial intelligence (AI). Firms such as Microsoft, Alphabet (Google), Meta Platforms, and Amazon have announced massive investments in data centers, servers, networking equipment, and AI infrastructure.

Full Market Cycles: Half Bull and Half Bear

In the end, it does not matter if you are “bullish” or “bearish.” However, what is grossly important in achieving long-term investment success is not necessarily being “right” during the first half of the cycle, but by not being “wrong” during the second half.

Economic Reacceleration: A Contrarian View

While consensus remains cautious, there is a case, however tenuous, for economic reacceleration. This isn’t about ignoring risks. It’s about acknowledging that conditions aligning could drive a shift from stagnation to renewed growth.

Forward Return And The Importance Of Math

The math on forward return expectations, given current valuation levels, does not hold up. The assumption that valuations can fall without the price of the markets being negatively impacted is also grossly flawed.

“Money Printing” By The Fed: Fact Or Fiction?

I recently penned an article on “Money Supply Growth,” which elicited a very thoughtful response from Garrett Baldwin via Substack. He argued that labeling Federal Reserve operations as “money printing” is not rhetoric, but rather a reality. He points to Ben Bernanke’s 2010 interview, where Bernanke described how the Fed marks up digital accounts.

Investor Dilemma: Pavlov Rings The Bell

Classical conditioning teaches us a valuable lesson regarding the current investor dilemma. Pavlov’s research discovered a basic psychological rule: when a neutral stimulus is repeatedly paired with a reward‑stimulus, eventually it will trigger the same response even when the reward is absent.

Gold Myths Luring Investors Into Risk

Gold is not immune to market cycles. It’s a volatile asset driven by shifting narratives and capital flows. If you’re buying gold today, understand what’s supporting the price, and what could shake that support loose. Treat gold as a hedge, not a core growth asset.

The Most Dangerous Era In History

We live in what Brett Arends claimed as“The Dumbest Stock Market In History,” but I believe it is potentially the most dangerous era. That phrase is not hyperbole as it reflects structural distortion, extreme valuations, and an investor base intoxicated by momentum and narrative.

Money Supply Growth: A Thesis With A Fatal Flaw

Bold calls to “run to gold, silver, and bitcoin” make for strong headlines, but they oversimplify the reality of modern finance. As we’ve seen, money supply growth is not inherently a sign of debasement but reflects economic expansion. Far from being destructive, government deficits flow directly into private-sector savings and stabilize household balance sheets.

Speculative Bull Runs and the Value of a Bearish Tilt

I want to discuss a different approach to portfolio management with you today. Rather, how to think like a “bear,” so you see the risks of the speculative bull run. However, to act like a “bull” to capture the gains while available. But that is a difficult skill to master.

ChatGPT Gives Financial Advice On Volatile Markets

Following Friday’s selloff amid the resurgence of tariff threats on China, I asked ChatGPT a simple question: ”How to Stay Calm In The Stock Market?” In this week’s post, I thought it would be helpful to review ChatGPT’s advice and discuss it in more detail.

Bear Market Losses – A Dangerous Illusion

When bear market losses occur, headlines talk in percentages: “The market dropped 20 %.” Investors nod. A 20 % decline sounds manageable, historical, and expected.

Promised Recession…So Where Is It?

Over the past three years, the economic conversation has been a “promised recession.” If you read the headlines, tracked economist surveys, or even listened to Wall Street strategists, you would have assumed a downturn was imminent. And yet, here we are, late into 2025, and the U.S. economy is still standing.

RSI (Relative Strength Index): Timing The Next Correction

While it may seem that way at extremes, momentum tends to exhaust, and reversals or corrections become more probable. The RSI gives us a real-time gauge of when a trend may be vulnerable to a pullback or turn.

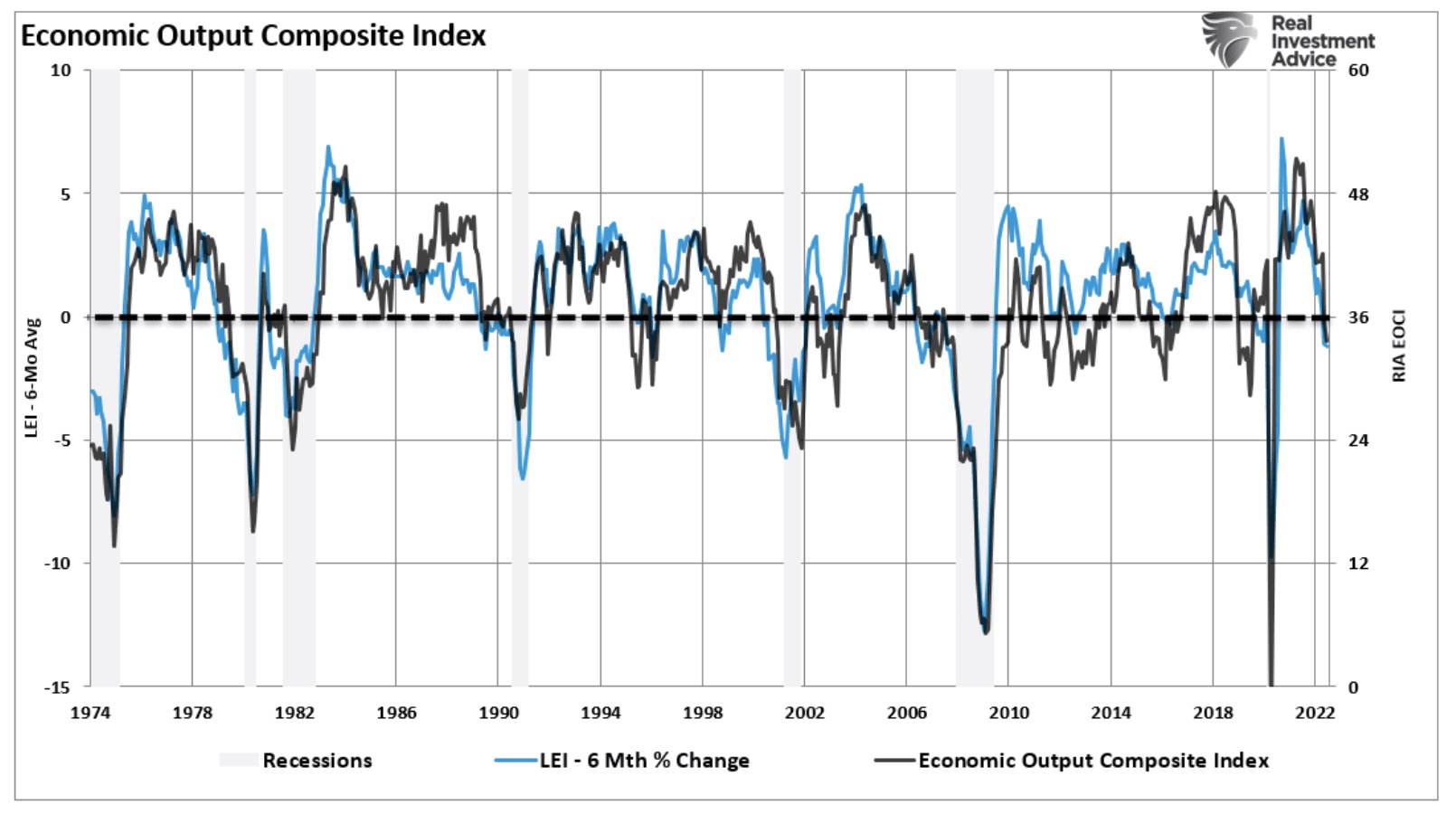

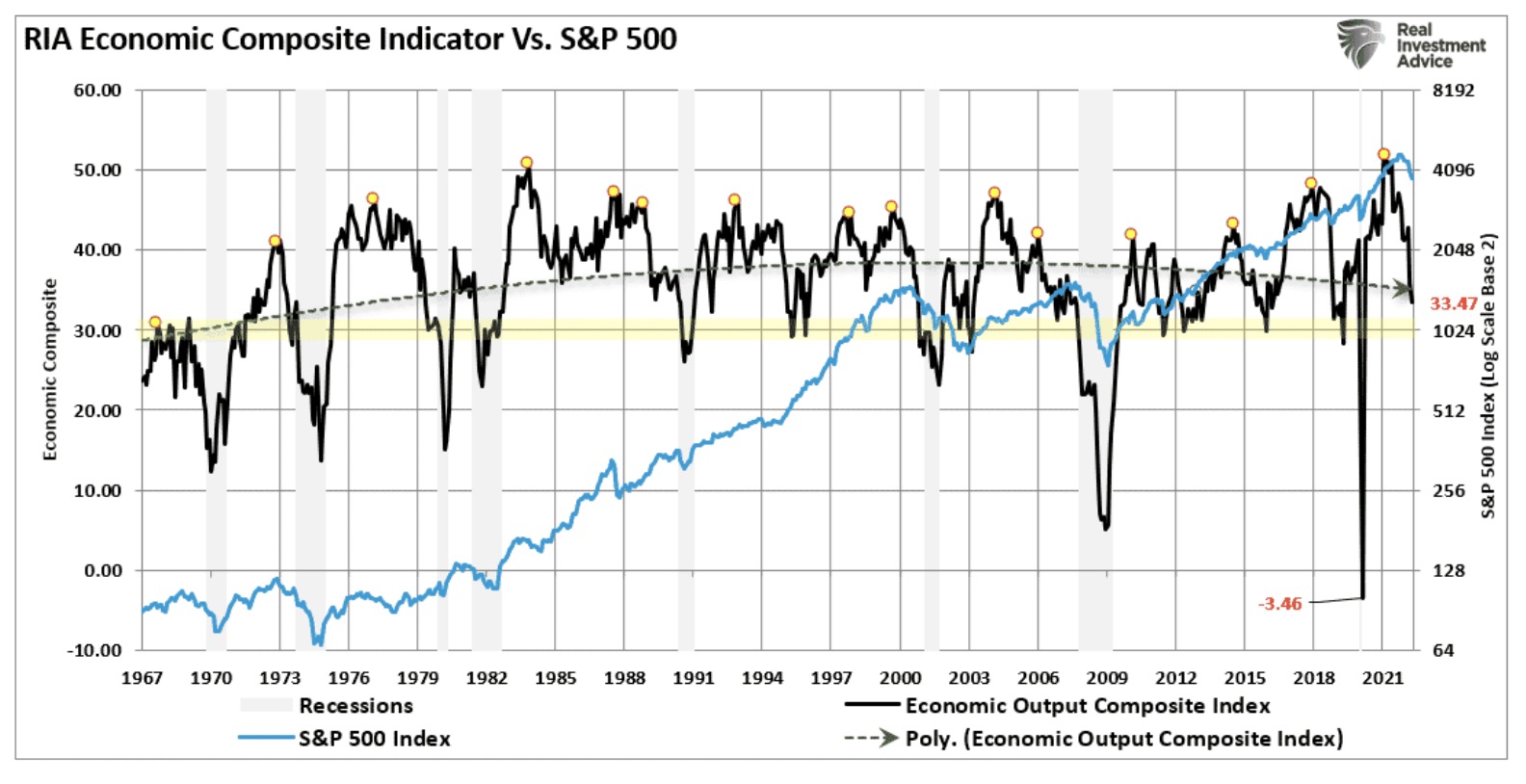

Slowdown Signals: Are Leading Indicators Flashing Red?

While the market is betting on an economic revival to support current valuation levels, the real economy is suggesting things are slowing down. Notably, the evidence isn’t coming from obscure corners. It’s showing up in the indicators designed to give us a heads-up before a storm arrives.

Data Centers And The Power Grid: A Path To Debt Relief?

The buildout of data centers and the power grid may offer the best opportunity to generate sustained growth. The scale of investment is large enough to matter, the economic multipliers are high, and the timeline aligns with when fiscal pressure will peak.

Markets: Bullish vs Bearish Case

To understand where the market might go, you need to weigh both the bull case and bear case in light of what is actually priced and what risks remain unacknowledged. The data support the bull momentum case, but many components are already baked into current prices.

Invest Or Index – Exploring 5-Different Strategies

We will examine five major investment strategies: value, growth, momentum, dividend, and index investing. Each comes with strengths and weaknesses. More importantly, each offers lessons from history’s greatest investors, including Benjamin Graham and Warren Buffett.

Corporate Earnings Slowdown Signaled By Employment Data

Despite the slowdown, the Federal Reserve remains hesitant. Chair Powell noted softening labor conditions at Jackson Hole and suggested the door is open to rate cuts. But no concrete shift in policy has occurred.

Why Diversification Is Failing In The Age Of Passive Investing

Surface-level diversification is no longer enough in a market increasingly driven by passive flows and dominated by a few mega-cap names. Owning multiple funds or asset classes does not guarantee protection if the underlying exposures overlap. Investors must go deeper and look beyond labels and into the actual drivers of risk and return.

Why Keynes’ Economic Theories Failed In Reality

The failures aren’t isolated miscalculations but the predictable result of a flawed framework that policymakers have clung to for decades. Keynesian economics didn’t just “get it wrong” in 2025, but has repeatedly failed to deliver on its promises for over forty years. And the consequences are becoming impossible to ignore.

Portfolio Risk Management: Accepting The Hard Truth

Here is the hard truth you must learn. Your real edge comes from limiting damage when you’re wrong and maximizing gains when you’re right, which is the very foundation of any risk plan. You will lose. You must build your system around that fact.

Energy Price As An Economic Indicator

Energy prices indicate economic strength, or, in this case, weakness. If the global economy grew strongly, the need for oil consumption would rise, absorbing the current production levels, causing energy prices to rise.

“Buy Every Dip” Remains The Winning Strategy…For Now

“Buy Every Dip” has lately been the “Siren’s Song” for this market. Such is seen in the flows into ETFs over the course of this year. Retail investors treat pullbacks as temporary noise, and their behavior borders on mechanical. Every sell-off is seen as an opportunity, not a warning.

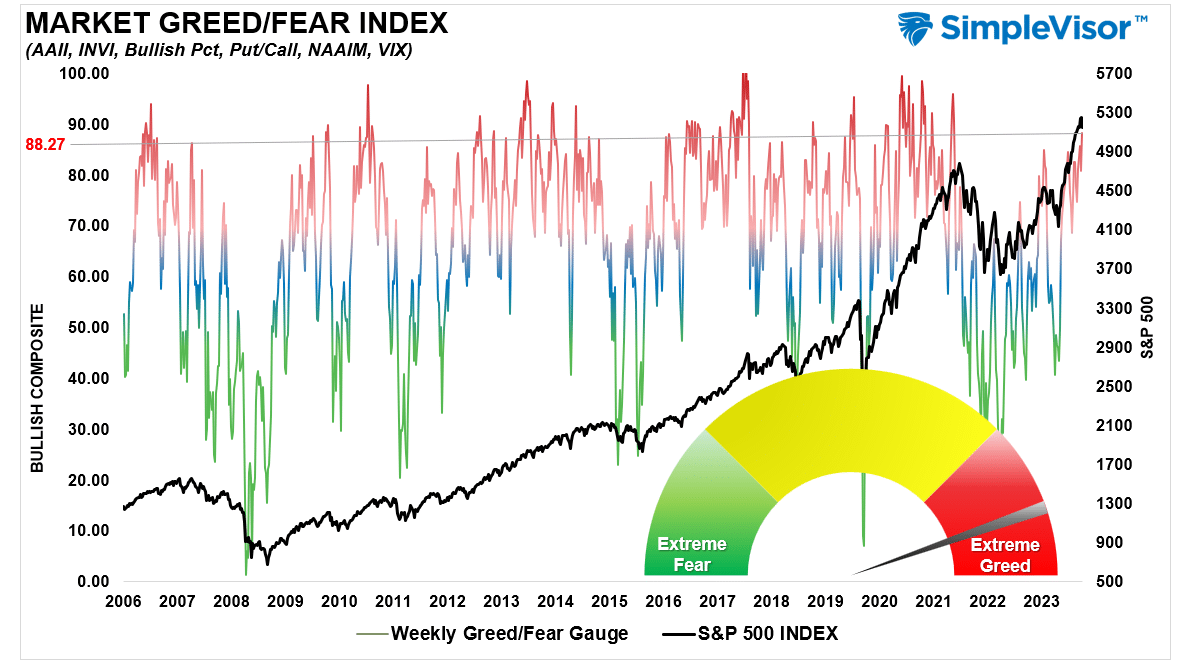

Excess Bullishness & 10-Rules To Navigate It

There is little doubt that excess bullishness has invaded the general market psyche. Just a couple of months following the market decline in March and April, where sentiment turned exceedingly bearish, the S&P 500 hovers near its highs.

Insider Selling Reveals Fallacy Of Buyback Theory

To benefit from a corporate buyback, an individual must sell their shares to the company. Conversely, those holding on to their shares are not compensated.

Meme Stock Trading & Livermore’s Approach To Speculation

The meme stock movement is again dominated by speculative retail trading driven by online forums, social media hype, and short-term momentum.

The Debt And Deficit Problem Isn’t What You Think

I understand the concerns about rising debt levels. However, the problem of rising debt levels for the U.S. is NOT a default but a continued degradation of economic growth. Let’s start this discussion with a basic fact—without continued increases in debt, there would be very little to no economic growth.

Bull Streak Ends As August Begins

As the turn of the calendar occurred on Friday, the bull streak for the market since the April lows ended. Such was not unexpected, and the correction has been a topic of discussion in our daily market commentary over the last two weeks.

Debasement: What It Is And Isn’t.

Over the past year, financial headlines continue to flood investors with doomsday predictions about the U.S. dollar. Whether it’s social media influencers waving “dollar collapse” charts or YouTube personalities warning about debasement, the noise has become deafening.

Portfolio Benchmarking: 5-Reasons Underperformance Occurs

When markets decline—especially after long periods of sustained growth—the familiar advice resurfaces: “Be patient. Stay invested. Ride it out.” The rationale? The market always goes up over time. But there’s a critical flaw in this narrative.

Is Private Equity A Wolf In Sheep’s Clothing?

Wall Street has a long history of selling the newest shiny object to Main Street just as the trade begins to sour. If the music stops at this private equity party, you don’t want to be the last one still dancing.

Retail Speculation Is Back With A Vengeance

Retail speculation is once again gripping the markets. A recent Wall Street Journal article highlighted how the latest retail gambling vehicle—zero-days-to-expiration (0DTE) options—has exploded in popularity.

China’s Economic Demise and its Impact on the U.S.

Few are as candid and historically accurate as hedge fund manager Kyle Bass when identifying structural breaks in the global economy. In a recent interview, Bass painted a grim but telling picture of China’s economic condition, warning.

Relative Returns Or Absolute. What’s More Important?

A couple of years ago, I wrote about absolute versus relative returns. Given the latest market run, I am getting a lot of questions about chasing returns, and individuals comparing themselves to the S&P 500 index.

Q2-2025 Earnings Season Preview

Next week, the Q2-2025 earnings season will begin in earnest as a barrage of S&P 500 companies report, starting with the Wall Street money center banks on Tuesday and Wednesday. Since earnings drive the market by supporting investor expectations, what should investors expect? Let’s dig into the details.

The Bull Market is Alive and Well

The bull market is alive and well, even amid widespread talk of the “death of U.S. exceptionalism.

SLR: Could It End The Bond Bear Market

For sophisticated investors, this technical shift marks a subtle but powerful pivot in monetary mechanics. It could create demand for Treasuries, improve market liquidity, and push yields lower at a time when the economy is slowing.

The Fed’s “Transitory” Mistake Is Affecting Its Outlook

The Fed’s credibility rests not on never being wrong, but on being adaptive and forward-looking. Inflation has cooled, wage growth has moderated, and economic momentum is slowing. Now is the time for the Fed to focus not on headline fears, but on real-time data.

The Dollar’s Death Is Greatly Exaggerated

The recent decline in the dollar relative to other currencies is well within historical norms. Notably, previous declines were much larger without the “fear-mongering” from the “experts of doom.”

Iran Struck By U.S.: Markets, Risk, and Rational Investing

Given the uncertainty of future events, global investors seek a “safe haven” for investment dollars. As such, U.S. Treasury Bonds and the U.S. dollar appreciate given their perceived “financial safety.” Last week, global investors were already starting to make that shift with the dollar rising.

The Iran-Israel Conflict And The Likely Impact On The Market

The Iran-Israel conflict and equity markets are now in sharp focus. As direct strikes escalated in June 2025, global financial markets responded immediately. Israel’s airstrikes on Iranian nuclear and energy infrastructure triggered retaliatory missile and drone attacks from Iran.

The Deficit Narrative May Find its Cure in Artificial Intelligence

Lately, the “deficit narrative” has dominated much of the financial media, particularly those channels that are continual “purveyors of doom.” In this post, we will discuss the “deficit narrative,” the likely outcomes, and why the cure for the deficit may be found in Artificial Intelligence.

“Buying The Dip” – Here’s A Technical Way To Do It

In recent years, “buying the dip“ and more vulgar variations have often been equated to “dumb money” or retail investors, who are presumed to always make a mistake. However, as investors, we need to rethink how we view “buying the dip” because the whole goal of investing is to “buy low and sell high.”

Does Consumer Spending Drive Earnings Growth?

It would seem evident that most investors would understand that consumer spending drives economic growth, ultimately creating corporate earnings growth. Yet, despite this somewhat tautological statement, Wall Street appears to ignore this simple reality when forecasting forward earnings.

Buying Stocks Is Always Hard

Buying stocks is always hard. Particularly during corrections. Or, near market peaks. Or, when stocks are falling. And when they are rising. Oh, buying stocks is also tricky when valuations are high. And when they are low. You get the point.

Ray Dalio Is Predicting A Financial Crisis…Again.

It doesn’t take much to understand that Ray Dalio, a hedge fund titan, is like every other human being and is prone to error. I will not dismiss Dalio entirely, as his track record of managing money at Bridgewater is nothing to be scoffed at.

The Stealth Bear Market

Given the uncertainty of what potentially happens next, the recent rally is an excellent opportunity to adjust portfolio risks to navigate the next leg of this market cycle.

The Anchoring Problem and How to Solve it

Keep your market perspective in check, avoid anchoring, and focus on your investment goals rather than market volatility.

Moody’s Debt Downgrade – Does It Matter?

As investors, we need to step back and examine the history of previous debt downgrades and their outcomes for the stock and bond markets. Let’s start with what Moody’s rating agency stated about its rating change.

Corporate Stock Buybacks – Do They Affect Markets?

Fisher Investments recently wrote an interesting article asking whether corporate stock buybacks affect markets.

A Bear Market Rally? Or, Just A Correction?

Assessing a bear market rally proves challenging when you experience it firsthand. It is only in hindsight that the complete picture reveals itself to investors. Of course, after a bear market rally, investors tend to review their investments and speculate on what they should have done differently.

The Awards You Never Get When Investing

In investing, success is often judged by numbers—returns on investment, percentage gains, and the ability to outperform benchmarks like the S&P 500. However, some investors frequently pursue a peculiar set of “awards” without realizing the pitfalls they embody.

Correction Continues – The Value of Risk Management

Despite the recent rally, the correction continues. While wanting to “buy the dip” is tempting, there has been enough technical damage to warrant remaining cautious in the near term.

Speculator Or Investor? 10-Rules From Legendary Investors

Are you a “speculator” or an “investor”? This is an essential question that every individual deploying capital into the financial markets must answer. The reason is that how you answer that question determines how you should behave during market cycles.

The Death Cross and Market Bottoms

In financial markets, few technical patterns generate as much attention and anxiety as the death cross.

Inflation Risk Is Subsiding Rapidly

Inflation risk has been a significant topic of discussion in the mainstream media for the last few years.

The Consumer is Tapping Out

The American consumer is tapped out. The savings buffer is gone, wage growth is declining, and credit costs are rising. Corporate America is already adjusting to this new reality, with companies issuing cautious guidance for 2025.

Yield Spreads Suggest The Risk Isn’t Over Yet

Yield spreads are critical to understanding market sentiment and predicting potential stock market downturns. While yield spreads have widened, they remain well below the long-term averages. However, if recession risks increase due to tariffs, sentiment, or illiquidity, those yield spreads will widen further.

The Stock Market Warning Of A Recession?

A Wall Street axiom states that the stock markets lead the economy by about six months. While not a perfect predictor, the stock market reacts to investor expectations about future corporate earnings, economic activity, interest rates, and inflation.

Stagflation Panic: A Misdiagnosed Media Spin

Following the latest Federal Reserve meeting, there was a massive surge in media headlines stating “stagflation.” The media’s stagflation panic is unsurprising as it elicits memories of the late 1970s during the Arab oil embargo.

U.S. Recession Risks Not As High As The Media Suggests

Over the last couple of weeks, the market sell-off eclipsed 10% on an intraday basis, sending investor sentiment plummeting to levels usually seen during more significant declines and previous bear markets.

Retail Investor Buys The Dip Despite Bearish Sentiment

It has been an interesting correction. The average retail investor was “buying the dip” despite having an extremely bearish outlook.

Stupidity And The 5-Laws Not To Follow

Human stupidity is the one thing you can rely on in financial markets. I recently read a great piece by Joe Wiggins at Behavioral Investment, which discusses why “Investing is hard.”

NYSE A/D Line: A Topping Process In Progress?

The recent sell-off has certainly sparked concerns with investors but the NYSE advance-decline line is an important technical measure to watch. However, what is it, and why does it matter?

The Risk Of A Recession Isn’t Zero

The risk of a recession in the U.S. is not zero. This is particularly true as the current Administration tackles Government bloat and implements tariffs. However, before we discuss why the risk of a recession could increase, it is crucial to remember the 2022 experience.

CAPE-5: A Different Measure Of Valuation

One of the most referenced valuation measures is Dr. Robert Shiller’s Cyclically Adjusted Price-Earnings Ratio, known as CAPE.

Estimates By Analysts Have Gone Parabolic

Just recently, S&P Global released its 2026 earnings estimates, which, for lack of a better word, have gone parabolic. Such should not be surprising given the ongoing exuberance on Wall Street. Unsurprisingly, rationalizations justify illogic when too much money is chasing too few assets.

The Tariff Risk Isn’t In Inflation (Part II)

If Trump tariffs Chinese, European, or Canadian products, those countries tend to enact counter-balancing tariffs on U.S. products. Such slows demand for goods and services between all parties, again a deflationary process.

Retail Exuberance Sets Market Up For A Correction

Retail investors are expected to become more bullish about increasing equity exposure when markets rise.

The Impact Of Tariffs Is Not As Bearish As Predicted

There are many media-driven narratives about the impact of tariffs on the economy and the markets. Most of them are incredibly bearish, predicting the absolute worst possible outcomes.

Bull Bear Report – Technical Update

The market defies more negative news because retail investors continue to step in and “buy the dip.” In our recent Bull Bear reports, we discussed the push by retail investors, but looking at retail sentiment is quite remarkable.

Forecasting Error Puts Fed On Wrong Side Again

The Federal Reserve’s record of forecasting has frequently led it to respond too late to changes in economic and financial conditions. In the most recent FOMC meeting, the Federal Reserve changed its statement to support a pause in the current interest rate-cutting cycle.

Tariffs Roil Markets

Over the weekend, President Trump announced tariffs of 25% on both Canada and Mexico, as well as a 10% tariff on China.

Bullish Exuberance Returns As Trump Takes Office

Bullish exuberance is returning to the markets and the economy in a big way following the Presidential election.

DeepSeek DeepSinks Bullish Exuberance

On Monday, markets were rocked by news that a Chinese Artificial Intelligence model, DeepSeek, performed better than expected at a lower development cost.

Do Money Supply, Deficit And QE Create Inflation?

In today’s post, we will examine the money supply represented by M2, the Federal budget deficit, the Fed’s previous adventures with QE, and the correlation to inflation.

Are Return Expectations For 2025 Too High?

Retail investors are the most optimistic about higher stock prices in 2025 by the most on record. Unsurprisingly, that sentiment resulted in the psychological rush to overpay for assets, pushing forward 1-year valuations sharply higher.

Gardening Guide To Better Portfolio Returns In 2025

As we head into 2025, investors are giddy over the market returns of the last two years. As shown, the annual returns, while elevated, have come with only average volatility along the way.

Tactically Bearish As Risks Increase

In last week’s discussion with Thoughtful Money, I noted that we are becoming more “tactically bearish” as we progress into 2025. While we have remained primarily bullish in equity positioning over the last two years, several risks are now worth considering.

“Curb Your Enthusiasm” In 2025

As we enter 2025, the financial markets are optimistic. That optimism is fueled by strong market performance over the last two years and analyst’s projections for continued growth. However, as “Curb Your Enthusiasm” often demonstrates, even the best-laid plans can unravel when overlooked details come to light. Here are five reasons why a more cautious approach to investing might be warranted in 2025.

The Rules Of Bob Farrell – An Updated Illustrated Guide

In a recent discussion on TheRealInvestmentShow, Bob Farrell and his 10 investment rules were discussed, which elicited several email questions asking, “Who is Bob Farrell, and where are these rules?”.

Permabull? Hardly.

I never thought someone would label me a “Permabull.” This is particularly true of the numerous articles I wrote over the years about the risks of excess valuations, monetary interventions, and artificially suppressed interest rates.

Prediction For 2025 Using Valuation Levels

It’s that time of year when Wall Street polishes up its crystal balls and predicts next year’s market returns. Since Wall Street never predicts a down year, these forecasts are often wrong and sometimes very wrong.

Economic Indicators And The Trajectory Of Earnings

Understanding the trajectory of corporate earnings is crucial for investors, as these earnings significantly influence stock valuations and market performance.

Portfolio Rebalancing And Valuations. Two Risks We Are Watching.

While analysts are currently very optimistic about the market, the combined risk of high valuations and the need to rebalance portfolios in the short term may pose an unanticipated threat.

The Kalecki Profit Equation And The Coming Reversion

Corporations are currently producing the highest level of profitability, as a percentage of GDP, in history.

Leverage And Speculation Are At Extremes

Financial markets often move in cycles where enthusiasm drives prices higher, sometimes far beyond what fundamentals justify.

Credit Spreads: The Markets Early Warning Indicators

Credit spreads are critical to understanding market sentiment and predicting potential stock market downturns.

Yardeni And The Long History Of Prediction Problems

Following President Trump’s re-election, the S&P 500 has seen an impressive surge, climbing past 6,000 and sparking significant optimism in the financial markets. Unsurprisingly, the rush by perma-bulls to make long-term predictions is remarkable.

“Trumpflation” Risks Likely Overstated

With the re-election of President Donald Trump, the worries about tariffs and pro-business policies sparked concerns of “Trumpflation.” Inflation has been a top concern for policymakers, businesses, and everyday consumers, especially following the sharp price increases experienced over the past few years.

Paul Tudor Jones: I Won’t Own Fixed Income

Paul Tudor Jones recently voiced concerns that rising U.S. deficits and debt and increasing interest rates could lead to a fiscal crisis. His perspective reflects the long-standing fear that sustained borrowing will trigger inflation, raise interest rates, and eventually overwhelm the government’s ability to manage its debt obligations.

Exuberance – Investors Have Rarely Been So Optimistic

Investor exuberance has rarely been so optimistic. In a recent post, we discussed investor expectations of returns over the next year, according to the Conference Board’s Sentiment Index.

Key Market Indicators for November 2024

Key market indicators for November 2024 present a complex but opportunity-filled environment for traders and investors. Following the first phase of Federal Reserve rate cuts and growing global uncertainties, the technical landscape suggests several notable shifts. Let’s explore the key market indicators to watch.

Lower Forward Returns Are A High Probability Event

I was emailed several times about a recent Morningstar article about J.P. Morgan’s warning of lower forward returns over the next decade. That was followed up by numerous emails about Goldman Sachs’ recent warnings of 3% annualized returns over the next decade.

Seasonality: Buy Signal And Investing Outcomes

Seasonality has long influenced stock market trends, offering insights into predictable cycles of strength and weakness throughout the year. Yale Hirsch, the creator of the Stock Trader’s Almanac, is one of the most well-known contributors to studying these patterns.

Bastiat And The “Broken Window”

Recent events, particularly the devastation caused by Hurricanes Helene and Milton in 2024, provide a clear example of why destruction does not create long-term economic prosperity. Despite the short-term boost in economic activity from rebuilding efforts, the broader economic implications are far more detrimental.

Greed And How To Lose 100% Of Your Money

While greed is necessary to build wealth, excessive greed often has far more terrible consequences when investing.

GDP Report Continues To Defy Recession Forecasts

The Bureau of Economic Analysis (BEA) recently released its second-quarter GDP report for 2024, showcasing a 2.96% growth rate. This number has sparked discussions among investors and analysts, particularly those predicting an imminent recession.

How Howard Marks Thinks About Risk…And You Should Too

When most people hear the word “risk,” they think about wild market swings, scary headlines, and losing money overnight, but Howard Marks, Co-Chairman and Co-Founder of Oaktree Capital Management, takes a different approach. In his new video series How to Think About Risk, Marks digs deep into what risk is and how investors should handle it. Spoiler alert: It’s not just about volatility.

Election Outcome Presents Opportunity For Investors

As the November 2024 election draws near, the election outcome will profoundly affect the financial markets. Whether Donald Trump or Kamala Harris wins the presidency, each administration will bring distinct policies creating investment opportunities and potential risks for investors. With a divisive political landscape, it is crucial to understand how these potential outcomes can shape the stock market and your portfolio strategy.

The “Everything Market” Could Last A While Longer

We are currently in the “everything market.” It doesn’t matter what you have probably invested in; it is currently increasing in value. However, it isn’t likely for the reasons you think. A recent Marketwatch interview with the always bullish Jim Paulson got his reasoning for the rally.

Tax Cuts – An Examination Of The 2017 TCJA Impact

An analysis of Presidential Candidate Trump’s policy proposals recently suggests that tax cuts will increase the deficit. While the raw analysis is correct, as it subtracts the potential for reduced tax collections from the tariff revenue, it ignores the impact on economic growth.

50 Basis Point Rate Cut – A Review And Outlook

Last week, the Federal Reserve made a significant move by cutting its overnight lending rate by 50 basis points. This marks the first rate cut since 2020, signaling the Fed is aggressively supporting the economy amid a backdrop of softening economic data. For investors, understanding how similar rate cuts have historically impacted markets and which sectors tend to benefit is key to navigating the months ahead.

Market Declines And The Problem Of Time

When stock markets rise, the bullish narrative tends to dominate, overlooking the potential impact of market declines. This oversight stems from two main problems: a basic misunderstanding of math and time’s critical role in investing.

Momentum Investing Gives You An Edge, Until It Doesn’t

Since 2020, momentum investing has generated significantly better returns than other strategies. Such is not surprising, given the massive amounts of stimulus injected into the financial system. However, Brett Arends for Marketwatch noted in 2021 that momentum investing can give you an edge.

Labor Market Impact On The Stock Market

The August jobs report highlighted a critical reality: the labor market is cooling off. While the headline figures seemed decent, the underlying data reveals clear warning signs that worker demand is slowing.

S&P 500 – A Bullish And Bearish Analysis

The S&P 500 index is a critical benchmark for the U.S. equity market, and its performance often dictates investor sentiment and decision-making. Between November 1, 2022, and September 6, 2024, the S&P 500 experienced a significant rally but not without volatility. Currently, investors have very mixed views about where markets are heading next as concerns of a recession linger or what changes to monetary policy will cause.

Technological Advances Make Things Better – Or Does It?

While technology is a powerful driver of economic growth, it also presents challenges that can negatively impact productivity, equality, mental health, and societal cohesion. Addressing these issues ensures that technological advancements promote sustainable and inclusive economic growth.

Risks Facing Bullish Investors As September Begins

Since the end of the “Yen Carry Trade” correction in August, bullish positioning has returned with a vengeance, yet two key risks face investors as September begins. While bullish positioning and optimism are ingredients for a rising market, there is more to this story.

Japanese Style Policies And The Future Of America

In a recent discussion with Adam Taggart via Thoughtful Money, we quickly touched on the similarities between the U.S. and Japanese monetary policies around the 11-minute mark. However, that discussion warrants a deeper dive. As we will review, Japan has much to tell us about the future of the U.S. economically.

Overbought Conditions Set Up Short-Term Correction

As noted in this past weekend’s newsletter, following the “Yen Carry Trade” blowup just three weeks ago, the market has quickly reverted to more extreme short-term overbought conditions.

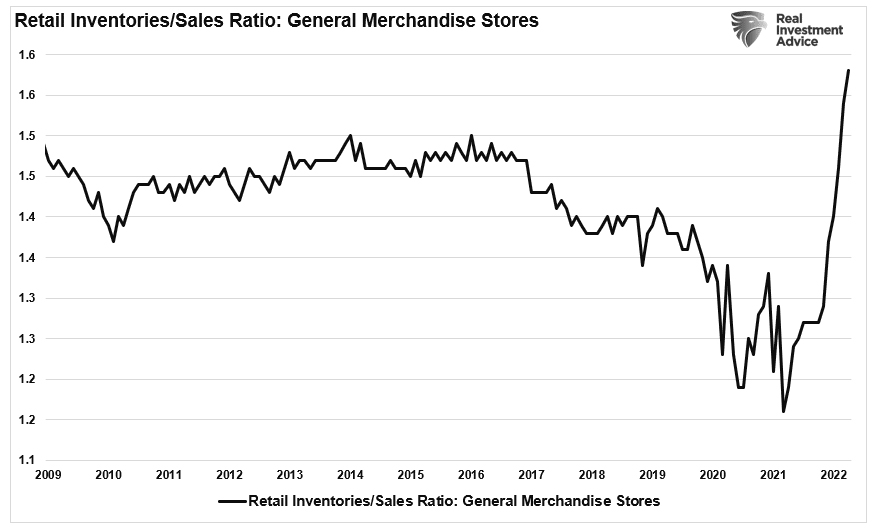

Red Flags In The Latest Retail Sales Report

The latest retail sales report seems to have given Wall Street something to cheer about. Headlines touting resilience in consumer spending increased hopes of a “soft landing” boosting the stock market.

Market Decline Over As Investors Buy The Dip

The market’s 8.5% decline during August sent shockwaves through the media and investors. The drop raised concerns about whether this was the start of a larger correction or a temporary pullback. However, a powerful reversal, driven by investor buying and corporate share repurchases, halted the decline, leading many to wonder if the worst is behind us.

Economic Growth Myth & Why Socialism Is Rising

Since the end of the financial crisis, economists, analysts, and the Federal Reserve have continued to predict a return to higher levels of economic growth. The hope remains that the Trillions of dollars spent during the pandemic-driven economic shutdown will turn into lasting organic economic growth.

Are Mega-Caps About To Make A Mega-Comeback?

Are the “Mega-Cap” stocks dead? Maybe. But there are four reasons why they could be staged for a comeback. The recent market correction from the July peak certainly got investors’ attention and rattled the more extreme complacency.

UBI – Tried, Tested And Failed As Expected

A Universal Basic Income (UBI) sounds great in theory. According to a previous study by the Roosevelt Institute, it could permanently increase the U.S. economy by trillions of dollars. While such socialistic policies sound great in theory, history, and data, they aren’t the economic saviors they are touted to be.

Yen Carry Trade Blows Up Sparking Global Sell-Off

On Monday morning, investors woke up to plunging stock markets as the “Yen Carry Trade” blew up. While media headlines suggested the sell-off was due to fears of a recession, slowing employment growth, or fears over Israel and Iran, such is not the case.

The Sahm Rule, Employment, And Recession Indicators

Economist Claudia Sahm developed the “Sahm Rule,” which states that the economy is in recession when the unemployment rate’s three-month average is a half percentage point above its 12-month low.

Bullish Years Often Have Corrections

In bullish years, markets often have corrections. Yet, after a lengthy bullish run, it always surprises me how quickly investors and the media panic with the slightest hint of a market pullback.

Overly Optimistic Investors Face Potential Disappointment

Overly optimistic investor expectations of market returns may be a problem.

The Bull Market – Could It Just Be Getting Started?

Yes, the market could continue to rotate massively from large-cap to small and mid-capitalization companies. However, given the current levels of bullish sentiment and allocations against a backdrop of weakening economic data and widening spreads, this suggests the current rotation may be nothing more than a significant short-covering rally.

Fed Rate Cuts – A Signal To Sell Stocks And Buy Bonds?

With both economic and inflation data continuing to weaken, expectations of Fed rate cuts are rising. Notably, following the latest consumer price index (CPI) report, which was weaker than expected, the odds of Fed rate cuts by September rose sharply. According to the CME, the odds of a 0.25% cut to the Fed rate are now 90%.

The “Broken Clock” Fallacy & The Art Of Contrarianism

Some state that “bears are like a ‘broken clock,’ they are right twice a day.” While it may seem true during a rising bull market, the reality is that both “bulls” and “bears” are owned by the “broken clock syndrome.”

Private Equity – Why Am I So Lucky?

Lately, I have been getting many questions about investing in private equity. Such is common during raging bull markets, as individuals seek higher rates of return than the market generates.

Earnings Bar Lowered As Q2 Reports Begin

Wall Street analysts continue significantly lowering the earnings bar as we enter the Q2 reporting period. Even as analysts lower that earnings bar, stocks have rallied sharply over the last few months.

Career Risk Traps Advisors Into Taking On Excess Risk

Financial advisors get a bad rap. Some deserve it; most don’t. The problem for the entire investment advisory and portfolio management community stems from the “career risk” they inevitably face.

S&P 6300? Is That Outside The Realm Of Possibility?

Goldman Sachs recently upped its price target to S&P 6300 for the end of this year, along with Evercore ISI upping its year-end target to 6000. Such is not surprising given the strong run in the markets this year.

A Fundamental Shift Higher In Valuations

Over the last decade, there has been an ongoing fundamental debate about markets and valuations. The bulls have long rationalized that low rates and increased liquidity justify overpaying for the underlying fundamentals.

Consumer Survey Shows Rising Bullishness

The latest consumer survey data from the New York Federal Reserve had interesting data.

Grant: Rates Are Going Much Higher. Is He Right?

Recently, James Grant, editor of the Interest Rate Observer, was asked about his outlook for interest rates. He sees interest rates moving in a cyclical pattern, potentially rising for another multi-decade period.

It’s Not 2000. But There Are Similarities.

More than a few individuals were active in the markets in 1999-2000, but many participants today were not. I remember looking at charts and writing about the craziness in markets as the fears of “Y2K” and the boom of “internet” filled media headlines.

Commodities And The Boom-Bust Cycle

It is always interesting when commodity prices rise. The market produces various narratives to suggest why prices will keep growing indefinitely. Such applies to all commodities, from oil to orange juice or cocoa beans. For example, Michael Hartnett of BofA recently noted.

Deviations From Long-Term Growth Trends Back To Extremes

In 2022, we discussed the market’s deviations from long-term growth trends. That discussion centered on Jeremy Grantham’s commentary about market bubbles.

Electricity Demand May Cure Debt Concerns

The future of electricity demand for everything from electric cars to Bitcoin mining to artificial intelligence may also be the cure for our debt concerns.

Benchmarking Your Portfolio May Have More Risk Than You Think

During ripping bull markets, investors often start benchmarking. That is comparing their portfolio’s performance against a major index—most often, the S&P 500 index. While that activity is heavily encouraged by Wall Street and the media, funded by Wall Street, is benchmarking the right for you?

Is Buffett’s Cash Hoard A Market Warning?

Every year, investors anxiously await the release of Warren Buffett’s annual letter to see what the “Oracle of Omaha” says about the markets, the economy, and where he is placing his money.

Moving Average Crossovers Suggest The Bull Is Back

While there is much debate over whether another bear market is imminent, weekly moving average crossovers suggest a different outcome for now. There are many current concerns, from geopolitical risk to still inverted yield curves, slowing economic growth, high interest rates, and inflation. Yet, despite those concerns, markets are flirting with all-time highs.

The Investment “Holy Grail” Doesn’t Exist

When it comes to the financial markets, investors have a litany of investment vehicles to choose from. The choices are nearly unlimited, from brokered certificates of deposit to complex derivative instruments.

Stock Rally As Powell Sparks A Buying Frenzy

The latest FOMC meeting caused a stock rally as Jerome Powell turned more “dovish” than expected. While Powell did note that progress on inflation has been lackluster, the announcement of the reversal of “Quantitative Tightening” (QT) excited the bulls.

Bullish Sentiment Index Reverses With Buybacks Resuming

Over the last two weeks, the bullish sentiment index has reversed from extreme greed to fear. The composite net bullish sentiment index, comprised of professional and retail investors, fell from 38.15 to 9.9 in two weeks.

Behavioral Traits That Are Killing Your Portfolio Returns

Behavioral traits and cognitive biases are anathemas to portfolio management as they impair our ability to remain emotionally disconnected from our money. As history all too clearly shows, investors always do the “opposite” of what they should when it comes to investing their own money.

Just A Correction, Or Is The Bull Market Over?

Is this just a correction after a strong bullish advance from November, or is the bull market ending?

Economic Warning From The NFIB

The latest National Federation of Independent Business (NFIB) survey was an economic warning that departed widely from more robust governmental reports.

Reflation Trade Is The New Bullish Narrative

Economic “reflation” is becoming the next bullish narrative as equity valuation increases continue to outpace earnings gains, at least according to Gold Sachs and Tony Pasquariello.

Immigration And Its Impact On Employment

While immigration has positively impacted economic growth and disinflation, this story has a dark side.

Margin Debt Surges As Bulls Leverage Bets

In the most recent report from FINRA, margin debt levels have surged as bullish investors leverage their bets in the equity market. The increase in leverage is not surprising, as it represents increased risk-taking by investors in the stock market.

Investing Lessons From Your Mother

Your mother likely imparted valuable investing lessons you may not have known. With Mother’s Day approaching and bullish market exuberance present, such is an excellent time to revisit the investing lessons she taught me.

Market Corrections Matter More Than You Think

During running bull markets, much commentary is written on why this time is different and why investors should not worry about market corrections.

Technical Measures And Valuations. Does Any Of It Matter?

Technical measures and valuations all suggest the market is expensive, overbought, and exuberant. However, none of it seems to matter as investors pile into equities to chase risk assets higher. A recent BofA report shows that the increase in risk appetite has been the largest since March 2021.

Wealth Gap And The Road To Serfdom

One of the most interesting conundrums is the surging wealth gap in America. Despite two of the largest bull markets in history since 1980, most Americans struggle with making ends meet and are unprepared for retirement. Such a reality starkly differs from the belief that rising asset prices benefit the masses.

Retirement Crisis Faces Government And Corporate Pensions

It is long past the time that we face the fact that “Social Security” is facing a retirement crisis. In June 2022, we touched on this issue, discussing the stark realities confronting Social Security.

Blackout Of Buybacks Threatens Bullish Run

With the last half of March upon us, the blackout of stock buybacks threatens to reduce one of the liquidity sources supporting the bullish run this year.

Household Equity Allocations Suggests Caution

Household equity allocations are again sharply rising, as the “Fear Of Missing Out” or “F.O.M.O.” fuels a near panic mentality to chase markets higher.

Digital Currency And Gold As Speculative Warnings

Over the last few years, digital currencies and gold have become decent barometers of speculative investor appetite.

Presidential Elections And Market Corrections

Presidential elections and market corrections have a long history of companionship. Given the rampant rhetoric between the right and left, such is not surprising. Such is particularly the case over the last two Presidential elections, where polarizing candidates trumped policies.

Valuation Metrics And Volatility Suggest Investor Caution

Valuation metrics have little to do with what the market will do over the next few days or months. However, they are essential to future outcomes and shouldn’t be dismissed during the surge in bullish sentiment.

Dumb Money Almost Back To Even, Making The Same Mistakes

After over two years, retail investors, also known as the “dumb money,” are almost back to breakeven.

This Is Nuts – An Entire Market Chasing One Stock

I revisited that original post a couple of weeks ago as the market approached its 5000 psychological milestone. Since then, the entire market has surged higher following last week’s earnings report from Nvidia (NVDA).

Small Cap Stocks May Be At Risk According To NFIB Data

Recently, retail investors have started chasing small-cap stocks in hopes of both a rate-cutting cycle by the Federal Reserve and avoiding a recession.

Don’t Fear All-Time Highs, Understand Them

Don’t fear all-time highs in the market. Such is a natural response for investors who are concerned about market risk. However, rather than fearing market exuberance, we must understand what drives it.

Fed Chair Powell Just Said The Quiet Part Out Loud

Regarding the surprisingly strong employment data, Fed Chair Powell said the quiet part out loud. The media hopes you didn’t hear it as we head into a contentious election in November.

Divergences And Other Technical Warnings

While the bulls remain entirely in control of the market narrative, divergences and other technical warnings suggest becoming more cautious may be prudent.

Housing Is Unaffordable. Dems Want to Make It Worse.

The cost of housing remains a hot-button topic with both Millennials and Gen-Z. Plenty of articles and commentaries address the concern of supply and affordability, with the younger generations getting hit the hardest.

“Theory Of Reflexivity” And Does It Matter?

I received an email this past week concerning George Soros’ “Theory Of Reflexivity.” It’s an interesting question, and I have previously written about the “Theory of Reflexivity.” Notably, this theory begins to resurface whenever markets become exuberant.

Retirement Savers Are Piling Into Stocks. Is That A Good Idea?

As the financial markets grind higher, retirement savers have consciously decided to add more to equity risk. Such was the result of a recent Bloomberg survey.

Money Market “Cash On The Sidelines” – A Myth That Won’t Die

As money market account balances soar, the mainstream media again proclaims, “There is $6 trillion of cash on the sidelines just waiting to come into the market.”

All-Time Highs For Stocks As Bitter Economic Headlines Persist

As the stock market hit all-time highs this past week, there remains an interesting disconnect from the more dour economic concerns of the average American. A recent survey by Axios, a left-leaning website that supports the current Administration, addressed this issue.

Q4 Earnings Season Gets Underway With Low Expectations

As we get ready to review the Q4 earnings report, stocks have rallied sharply over the last two months

Deficit Spending Keeping The Economy Out Of Recession

Economic growth continues to defy expectations of a slowdown and recession due to continued increases in deficit spending.

Portfolio Return Expectations By Investors Are Too High

A stunning post from VisualCapitalist showed a poll of 8550 investors and 2700 advisors and the gap between the two of future portfolio return expectations. The poll was global; however, I will focus on this post’s domestic portfolio return expectations.

Sell Cash, Buy Stocks As Powell Pivots?

A recent warning by YahooFinance warns investors to sell their cash and buy bonds and stocks now as the Fed pauses.

Wealth Effect Increases and Recession Risks

What is the “wealth effect,” and why is it important? It is a great question and reminded me of “A Funny Thing Happened on the Way to the Colosseum.“

The Markets Are Front Running the First Rate Cut

In October, the markets were down 10% from the July high, bond yields were touching 5%, and talk of a coming recession was rampant. What happened?

Wall Street Analysts Are Optimistic For 2024

It’s that time of the year where Wall Street polishes up their crystal balls and pin targets on the S&P index for the upcoming year. As is often the case, while Wall Street is always optimistic, the forecasts prove pretty wrong.

Stock Market Correction Coming Before The Santa Claus Rally

Is a stock market correction coming before the Santa Claus rally at the end of the year?

Recessionary Indicators Update. Soft Landing Or Worse?

I previously discussed a slate of recessionary indicators with high correlations to recessionary onsets. However, as we head into 2024, many Wall Street economists predict a “soft landing” or “no recession” outcome for the economy.

CFNAI: The Most Important & Overlooked Economic Number

The Chicago Fed National Activity Index (CFNAI) is arguably one of the most important and overlooked economic indicators.

Bond Bear Market. Is It Dead, Or Just Hibernating?

Is the bond bear market finally over? That is the question everyone is asking now that bond prices rallied sharply following the November FOMC policy meeting.

Job And Retail Sales Data: Always Good Until They Aren’t

Despite substantially tighter monetary policy, the strength of jobs and retail sales stumped expectations of a recessionary downturn in 2022.

Investing Rules To Navigate Volatile Markets

While often difficult, investing rules can help us maintain our focus and investment discipline in volatile or uncertain markets.

Economists No Longer Expect A Recession. Are They Right?

Economists no longer expect a recession. Such was according to a recent WSJ survey of Wall Street economists.

The Pain Trade Is Higher Into Year-End

The “pain trade” continues to be higher into year-end.

Consequences Are Always Unintended

While the article focuses mainly on the rise in bond yields, it applies to several current market events.

Restrictive Yields Will Be The Fed’s Waterloo

Restrictive monetary conditions, from higher yields and tighter lending conditions, are the Fed’s “Waterloo.”

Crisis Events Are A Hallmark Of The Federal Reserve

As the “soft landing” narrative grows, the risk of a “crisis” event in the economy increases. Will the Fed trigger another crisis event? While unknown, the risk seems likely as the Fed’s “higher for longer” narrative is compromised by lagging economic data.

Bond Valuations Are Cheap.

Psychology in markets is always fascinating. In February 2009, I wrote “8 Reasons For A Bull Market.” While in hindsight, it is easy to see that was the right call, overall, psychology was highly negative at the time.

Fund Flows And Bond Yields. Two Different Stories

While bond yields have risen sharply lately, fund flows into bonds tell two very different stories.

Government Shutdown Averted. But Is That A Good Thing?

Once again, due to the ongoing lack of fiscal responsibility in Washington, the markets and the economy faced a Government shutdown.

“Soft Landing” Hope By The Fed Is Likely Optimistic

The Fed’s “soft landing” hopes are likely overly optimistic. Such was the context of the recent #BullBearReport, which discussed the long record of the Fed’s economic growth projections.

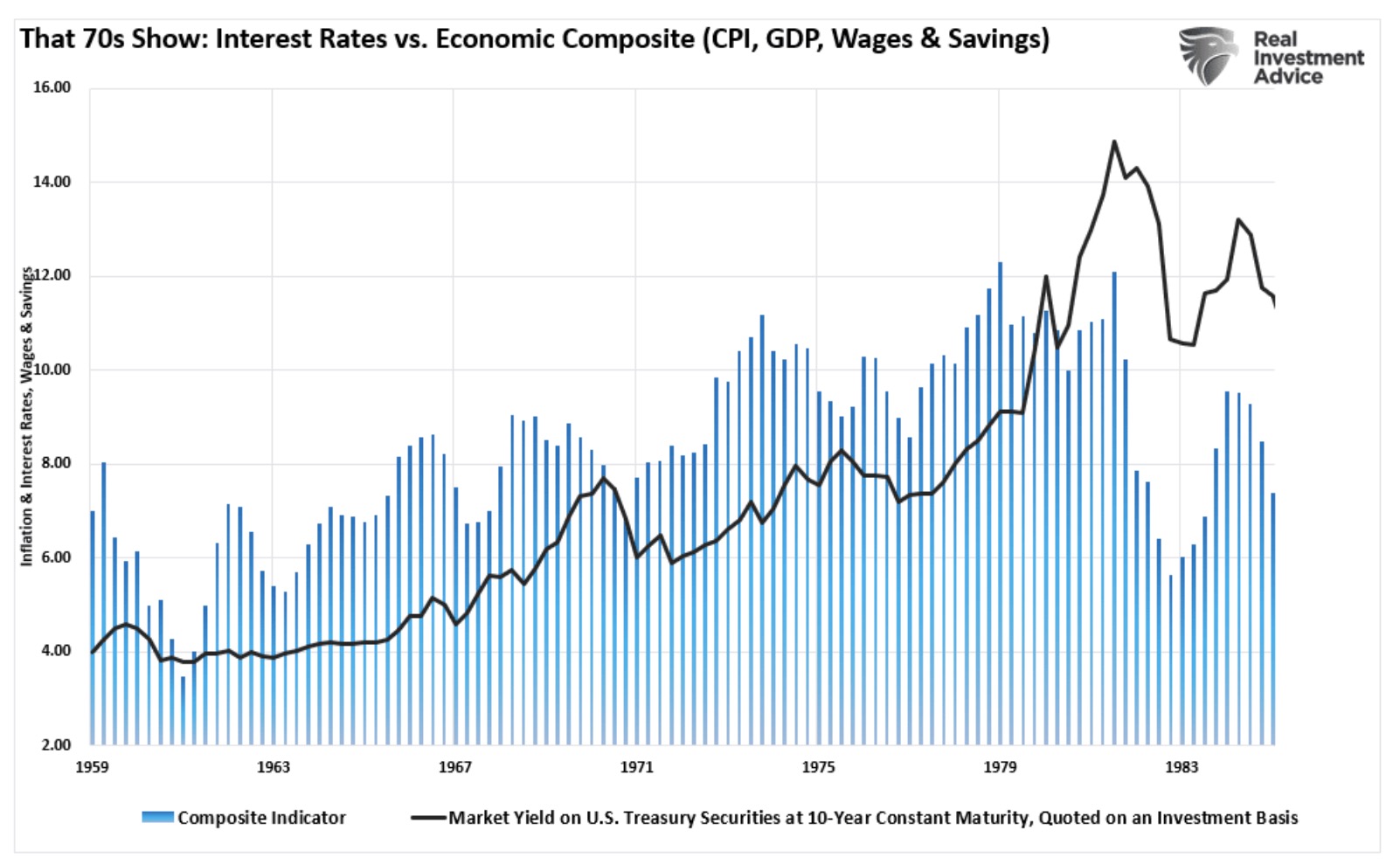

“That 70s Show”

The hit TV series “That 70s Show” aired from 1998 to 2006 and focused on six teenage friends living in Wisconsin in the late 70s.

Bond Vigilantes And The Waiting For Godot

The term “Bond Vigilantes” is a nostalgic twist on an old-west theme. In the nineteenth century, the American West formed self-appointed groups, or committees, to seize the duties of law enforcement and judicial authority in situations when citizens found law enforcement lacking or inadequate.

Predictions Are Pointless. Why You Shouldn’t Listen To Gurus.

Okay, I took a little poetic license, but the point is that while we try, predictions of the future are difficult at best and impossible at worst.

Economic Data Points Diverge

Since the beginning of the year, economic data has continued to defy the recession calls of 2022.

Mega-Cap Stocks Continue To Dominate. But Why?

Mega-cap stocks continue to dominate the market in 2023. The question is, why? After all, many other great companies have arguably much better valuations and fundamentals.

Powell’s Speech Obfuscates The Truth Behind Inflation

Powell’s recent Jackson Hole Summit speech was mainly as expected. Well, except for the part where Powell obfuscated the truth behind the surge in inflation.

10 Best Days – A Meme For Every Bull Market

About once a year, I have to address the issue of chasing the “10 Best Days” of the year.

Deficit Surge Will Lead To Lower Rates, Not Higher

Fitch’s recent downgrade of the U.S. debt rating alarmed investors as the deficit and debt steadily increased. The downgrade sent 10-year Treasury bond yields above 4%, causing concern about America’s deteriorating financial condition.

Stock Market Rally Coming? And Investing In 2024.

Is a stock market rally coming? I think that is most likely the case. However, to understand why, we must review what we said at the beginning of July in “Complacency Seems Overly Complacent.”

A Recession Is Coming, Or Is It?

Since the beginning of 2022, the media has regularly warned a recession is coming.

Government Bonds Or Stocks? Which Is A Better Choice Now?

Government bonds or stocks? If you were picking an asset class to outperform over the next 18-24 months, which would you choose?

Tax Receipts. Another Leading Recession Indicator?

Tax receipts are falling, which has historically preceded economic recessions.

Market Cycle Lows and Bull Market Recoveries

There is a rhythm to the markets, and market cycle lows support bull market recoveries. Recently, Ed Yardeni made a bold prediction that the S&P 500 index could hit a high of 5400 in 2024.

Deficits, Debt, And Why $32 Trillion Matters

While Washington continues a seemingly unbridled spending spree under the assumption “more spending” is better, debts and deficits matter. To better understand the impact of debt and deficits on economic growth, we must know where we came from.

“Beating Estimates” – How Companies Win in Earnings Season

No matter what happens, financially or economically, there is always a high number of companies regularly beating Wall Street estimates.

ESG Is Dying Its Inevitable Death

ESG scoring and mandates remain a subject we have contested since it sprang to life in 2020. The push of “woke activism” on, and by companies, to meet nebulous or artificial standards has led to various bad outcomes.

Volatility Index Is So Low It Has To Go Up?

The volatility index is so low it has to go higher eventually. Such seems obvious, but this year, despite the banking crisis, higher interest rates, and slowing economic data, investors continue to abandon hedges amid bullish optimism.

Market Cycles And Why The Bull Isn’t Dead

There is much debate as of late on the current market cycle. Is it a bear market? Maybe. But what if this is just a correction within a 40-year-long secular bull market cycle?

Stock Risk – Does It Decline Over Time?

Does stock risk decline the longer the holding period is? It’s a great question and something I received a comment about.

Student Loan Repayments – Will It Start The Recession?

Millions of young Americans will face the end of the student loan payment moratorium this summer. Why is this happening now, after a three-year break from payments?

Bull Trap Or A Bull Market?

Is the recent rally a “bull trap,” or are we in a new “bull market?” Such was a question I recently received on Twitter. Of course, understanding the term “bull trap” is needed for those not deep into technical analysis.

Signs, Signs, Everywhere Signs (But No Recession Yet)

“Signs” was a song by the Five Man Electrical Band in 1970 about the hippie movement. The song came to mind as I was looking at the economic data recently.

Speculation In A.I. May Face Challenges

The current market speculation surrounding artificial intelligence (A.I.) has garnered everyone’s attention.

New Bull Market? It’s Different This Time.

“It’s a ‘New Bull Market’!” Over the past few days, the call of a new bull market has plastered headlines and media commentary.

Bullish Sentiment Rises As FOMO Kicks In

Bullish sentiment has surged as the “Fear Of Missing Out,” or FOMO, kicked in in recent weeks. It is somewhat interesting to write this blog, given that we discussed the exact opposite roughly one year ago.

Eurozone Revised Into a Recession

The Eurozone just entered a recession as the region posted two consecutive quarters of negative economic growth. The manner in which it entered a recession is a bit quirky.

Breadth Not As Strong As Advance-Decline Suggests

In several recent blog posts and weekly Bull Bear Reports, we discussed our concern over the narrow breadth of the rally in 2023.

Technical Review Of The Market: Bulls In Control

Lately, we discussed macro-related market issues such as the” A.I., chase,” but a technical review can help manage shorter-term risks. Currently, the debate is about the market rally from the October lows. Is it a resumption of the 2009 bull market trend or an extended bear market rally?

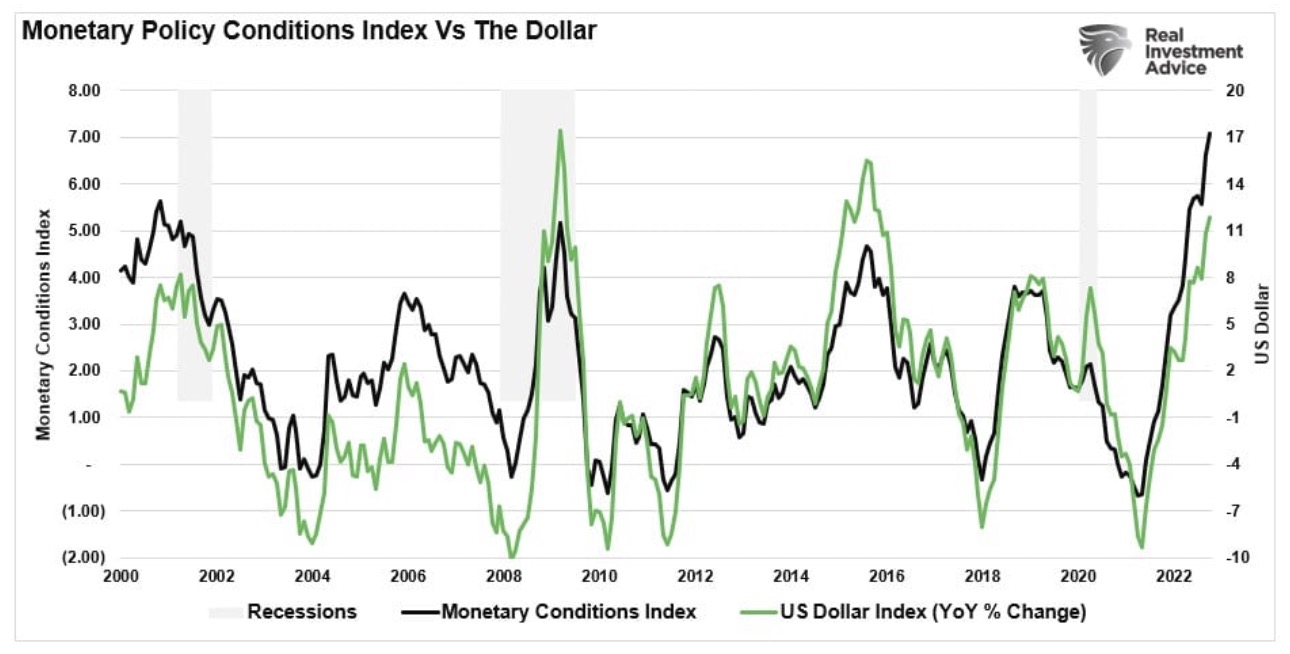

Monetary Conditions Index Is Working Against The Fed

Could monetary conditions be supportive of the “soft landing” scenario? While the “recession” versus “no recession” debate rages, there is a precedent for a “soft landing” scenario. Such is where the economy slows substantially but avoids a deeper contraction.

The Treasury Bond. It’s Time Has Likely Come.

I received many emails and questions on “why” we are adding the U.S. Treasury bond to our portfolios. The question is understandable, given its dire performance in 2022, where bonds had the biggest drawdown since 1786.

A.I., Narrow Markets, And The New T.I.N.A.

The A.I. chase is making for a very narrow market.

The AI Revolution. A Repeat Of History.

The artificial intelligence, or “AI,” revolution is upon us. The financial media and headlines are abuzz with stories of generative “AI” and the subsequent “industrial revolution.”

Monetary Support Suggests Bear Market Is Possibly Over