Last Wednesday, the Federal Reserve announced the latest decision concerning monetary policy which contained three primary components:

- A cut of 25bps

- Stopping balance sheet reductions (or Quantitative Tightening or Q.T.)

- An outlook suggestive this may be the only rate cut for a while.

While stocks dropped on disappointment they Fed may not cut further; it didn’t take long for bullish commentators to start suggesting why the cuts were supportive of higher asset prices. To wit:

“Given today’s Fed decision and guidance, we remain comfortable with our view that the Fed will provide two more 25bp cuts this year (September and October),” – Bank of America.

Simply, cutting rates, and stopping Q.T., is the return of “accommodative policy” for the markets and the “ringing of Pavlov’s bell.” Via CNBC:

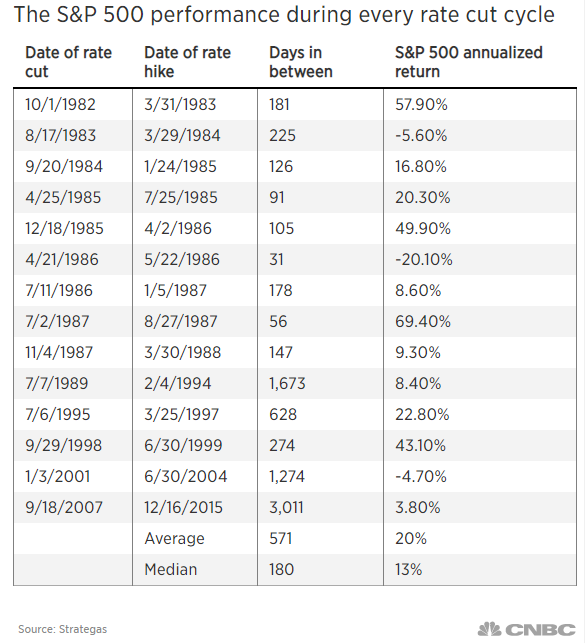

“The old investing mantra ‘don’t fight the Fed’ stands the test of time for a reason. Going back to 1982, the average annualized return for the S&P 500 between the first rate cut and the next hike has been 20%, while the median increase has been 13%, according to Strategas. The data show investors would do well if they invest in a way that aligns with the Federal Reserve’s policy direction, rather than against it, hence ‘don’t fight the Fed.’”

This is an interesting premise because when the Fed started hiking rates at the end of 2015, it also was bullish. Via Forbes:

“Early in a rate increase cycle, however, higher rates are actually good for the stock market. This is because rising rates, early on, signal an improving economy, and the faster growth more than compensates for higher rates.”

So, exactly “when” are Fed actions are “not bullish?”

I would suggest now.

As I noted in this past weekend’s missive:

“Lower rates have less impact on the ‘economy,’when the monetary transmission system is weak. This is evident from the fact that surging asset prices have left 80% of the population behind in terms of higher levels of prosperity. This also is why tax cuts failed to work as intended. After a decade of low rates, and excess liquidity, the ability to ‘pull-forward’ demand has become limited.”

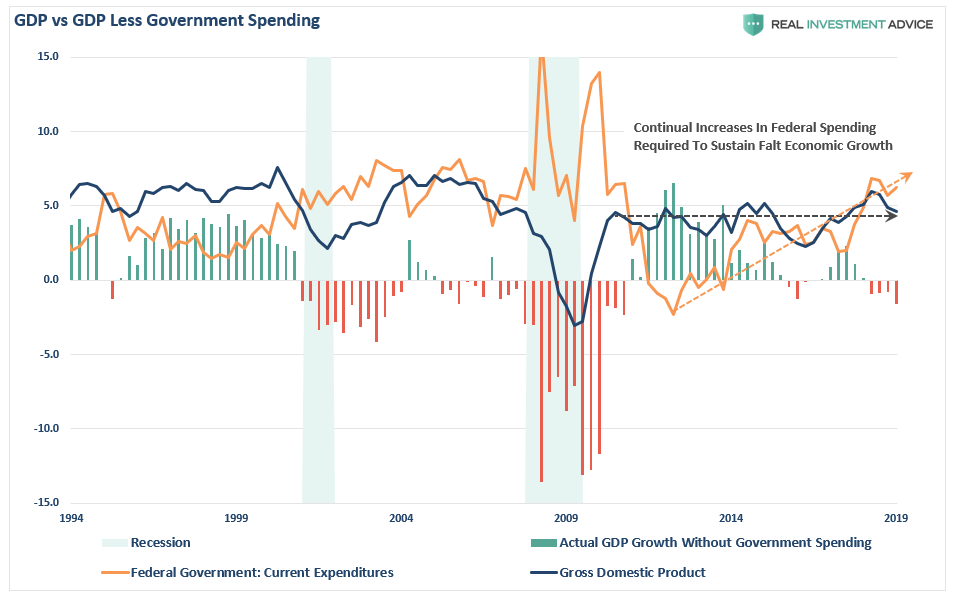

While, in the short-term, it may seem that whatever the Fed does is “bullish,” as the performance of the stock market since 2009 would seem to support, it has been a function unbridled fiscal largesse. As shown in the chart below, the Fed’s actions have been supported by a massive amount of Government spending as noted last week:

“As shown in the chart below, since 2010 it has taken continually increases in Federal expenditures just to maintain economic growth at the same level it was nearly a decade ago.”

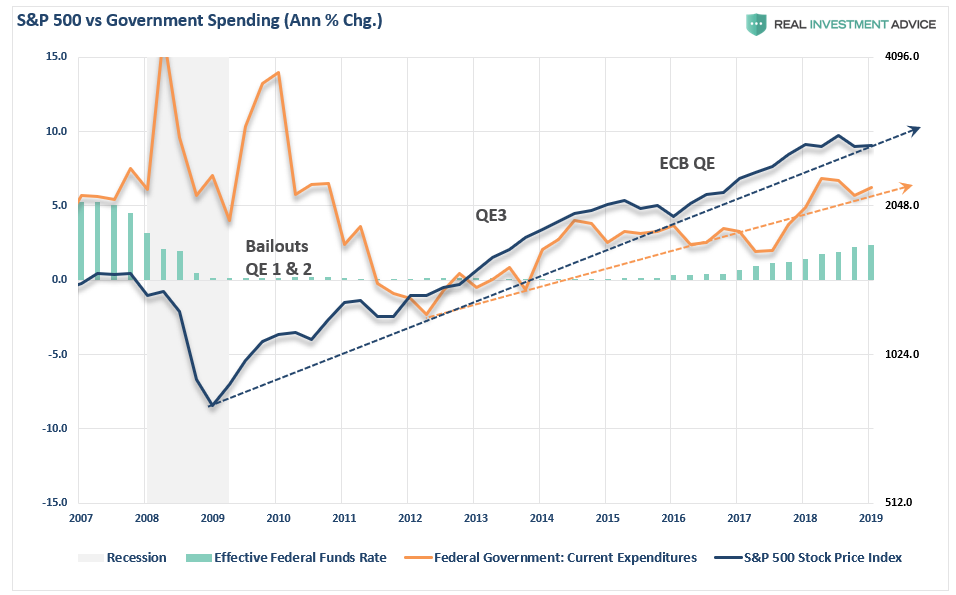

But let’s modify that chart to compare the Fed’s actions plus government expenditures to the S&P 500.

With that much liquidity sloshing around, it had to go somewhere. Not surprisingly, as the Fed suppressed interest rates, it forced investors to chase yield.

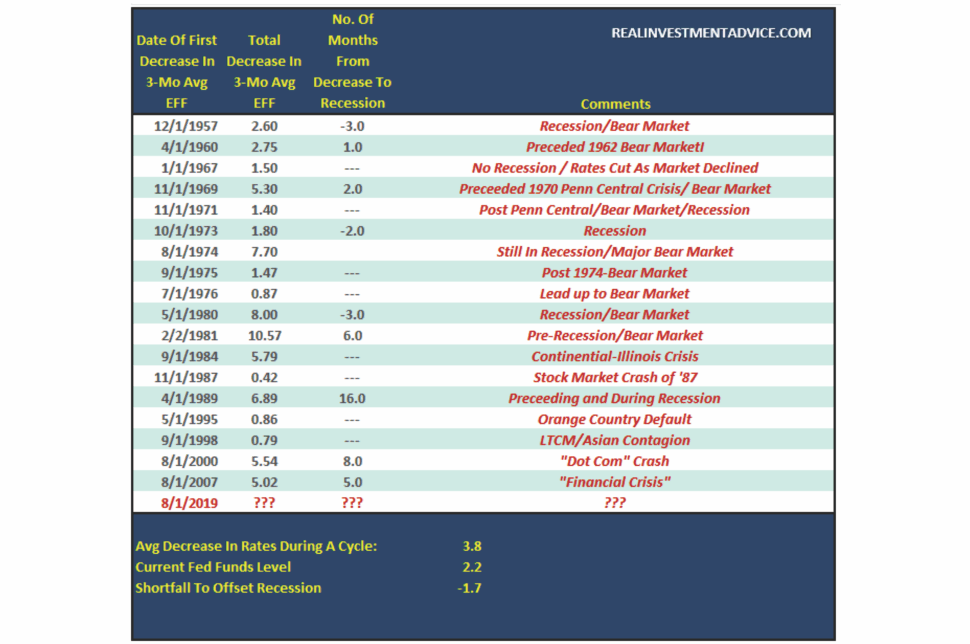

The problem with the table from CNBC above, as it only tells you what happens immediately after the Fed cut rates the first time. By the time the Fed is starts cutting rates, the markets are well entrenched into a bullish trend. Stocks aren’t beginning a bull run, but rather are being carried higher by existing momentum which has typically been a hallmark of a late-stage bullish cycle. In every case, there was an eventual negative outcome following Fed rate cut cycles. (The table below uses the 3-month average of the effective Fed Funds rate.)

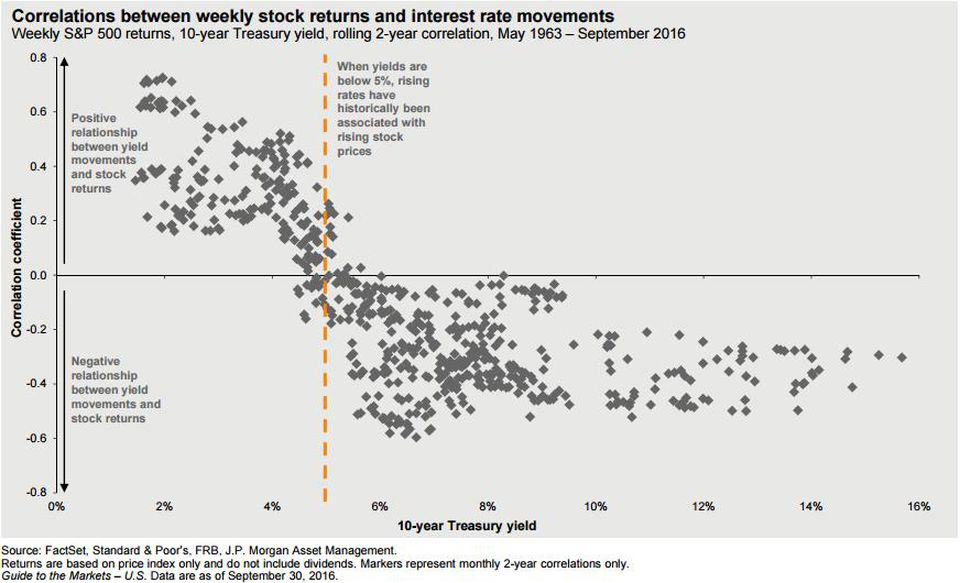

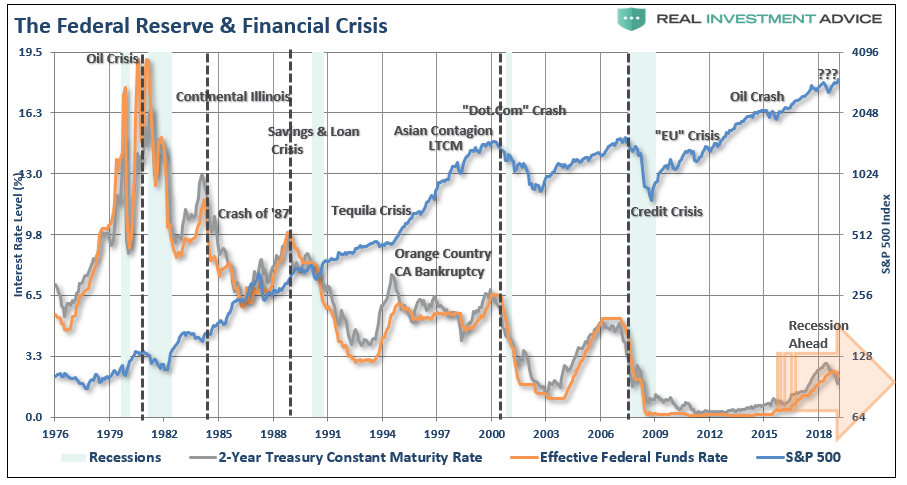

The chart of the effective Fed funds rate and the S&P 500 tells the story. (The vertical dashed lines marked the initial cuts, and you can see where subsequent crisis and declines occurred.)

The one exception was the initial rate cut in 1995 following the Orange County Bankruptcy, an “insurance cut,” despite both a strong market and economy at the time. As recently noted by J.P. Morgan:

“The late 1990’s rate cuts were used as insurance against Mexican and Russian default and collapse of hedge fund Long-Term Capital Management at the time, bolstered the equity market. The only other time the S&P 500 saw stronger performance following a rate cut was in 1980.”

The early 1980s are NOT comparative to the current cycle.

- The U.S. economy was just coming out of back-to-back recessions

- Valuations were extremely low

- Dividends were high; and,

- Inflation and interest rates were in double-digits.

- President Reagan had just passed tax reform

- The banks were deregulated; and,

- Inflation and interest rates were beginning a 40-year secular decline.

- Household debt was only about 60% of net worth and just starting a 40-year “leveraging cycle” .

In other words, there was nowhere for the market to go but up.

Clearly, such is not the case today, as deflation, debt, and demographic shifts loom large.

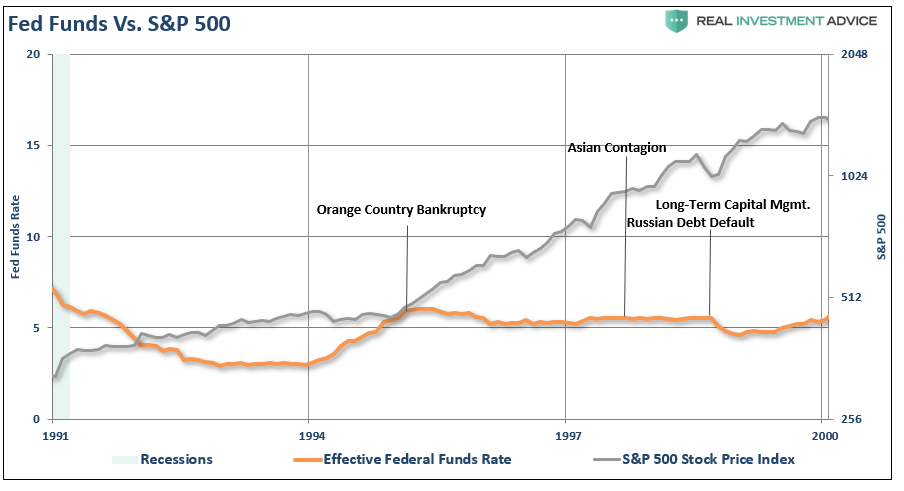

But What About 1995?

The mid-late 1990’s rate cuts was also another anomalous market environment. The Fed began a rate hiking campaign in 1993 as the economy began to stretch its legs post the 1991 recession. However, the Fed cut rates slightly in 1995, and again in 1998, to offset the risk imposed from three major market-related events. Ironically, it was the Fed’s tightening of monetary policy which contributed to those events.

Another critical point is that rates were relatively stable post the 1991 recession rather than the rather sharp increase we have seen over the last couple of years. Also, economic growth, as I showed last week, was running at an average of 3.5% on an inflation-adjusted basis, versus 2%-ish today.

Importantly, the markets sharp advance in the late-1990’s was due to a period of “market nirvana” as the internet became mainstream changing the way information was accessed, utilized, and institutionalized.

- Mutual funds were a virtual “Hoover vacuum” sucking up retail assets and lofting asset prices higher.

- Pension funds were finally allowed to invest in stocks, rather than just Treasuries, which brought massive buying power to the markets.

- Foreign flows also poured into Wall Street to chase the raging bull market higher.

- Lastly, “internet trading” hit the internet, which further opened the doors of the “WallStreet Casino” to the masses.

Yes, for a brief moment, the markets raged as “irrational exuberance” prevailed. Of course, while the rate cuts in 1995 didn’t slow the growth of the “bubble” immediately, it wasn’t long before all the gains were wiped out by the “Dot.com” crash.

Timing, as they say, is everything.

This Isn’t 1995

A quick comparison between 1995, and today, also elicits many other concerns about the markets ability to dramatically extend its current cycle.

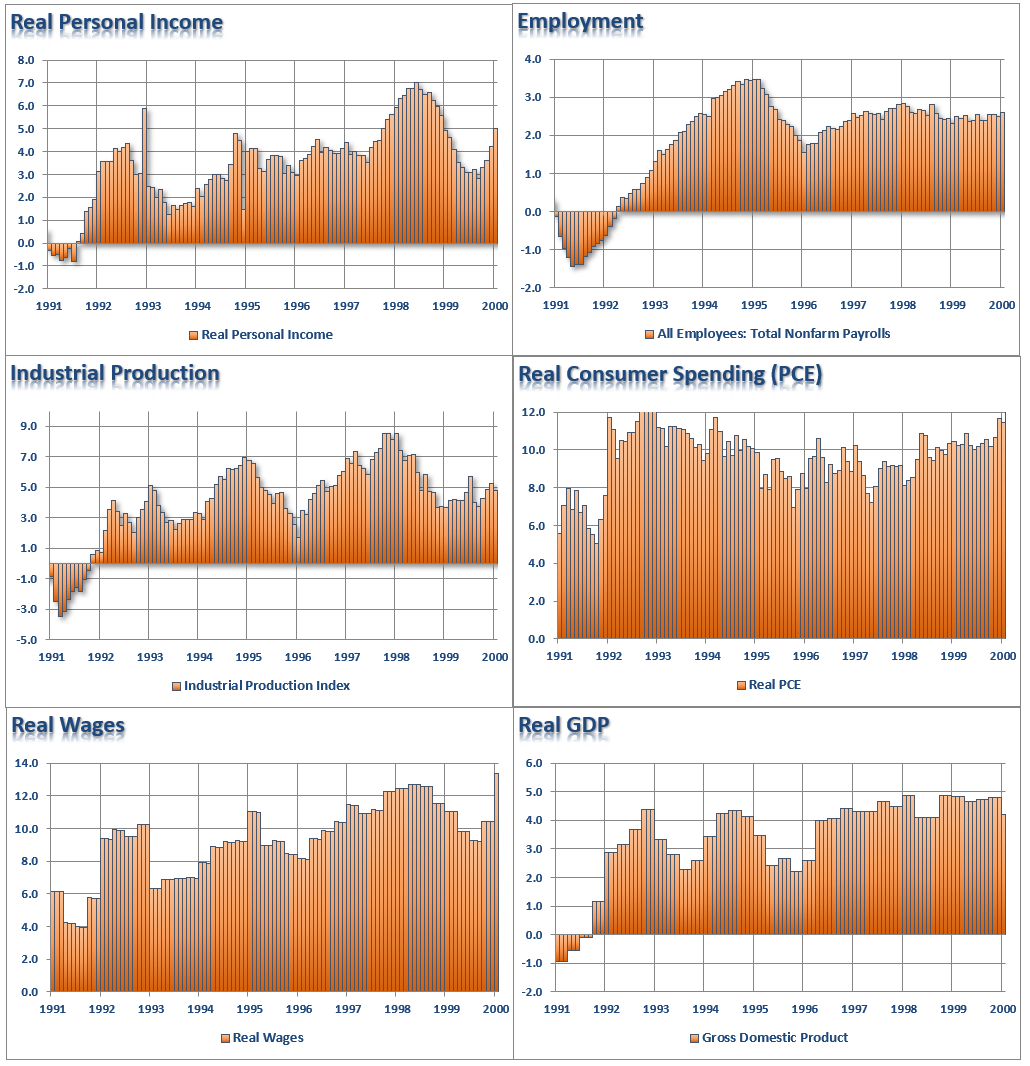

From 1991-2000 (10-Years)

- Personal Incomes averaged 4% and were rising to 5% on an annual rate

- Employment averaged a 2.5% annual growth rate and was solid heading into 2000.

- Industrial Production averaged about 5% annual growth and was rising at the end of 1999.

- Real Consumer Spending averaged a nearly 12% annual growth rate heading into 2000.

- Real Wages were climbing steadily from 1991 to 1999 and hit a peak of almost 14% in 1999.

- Real GDP was running at more than 4% annually in December of 1999.

NOTE: There was NO SIGN of RECESSION in late 1999.

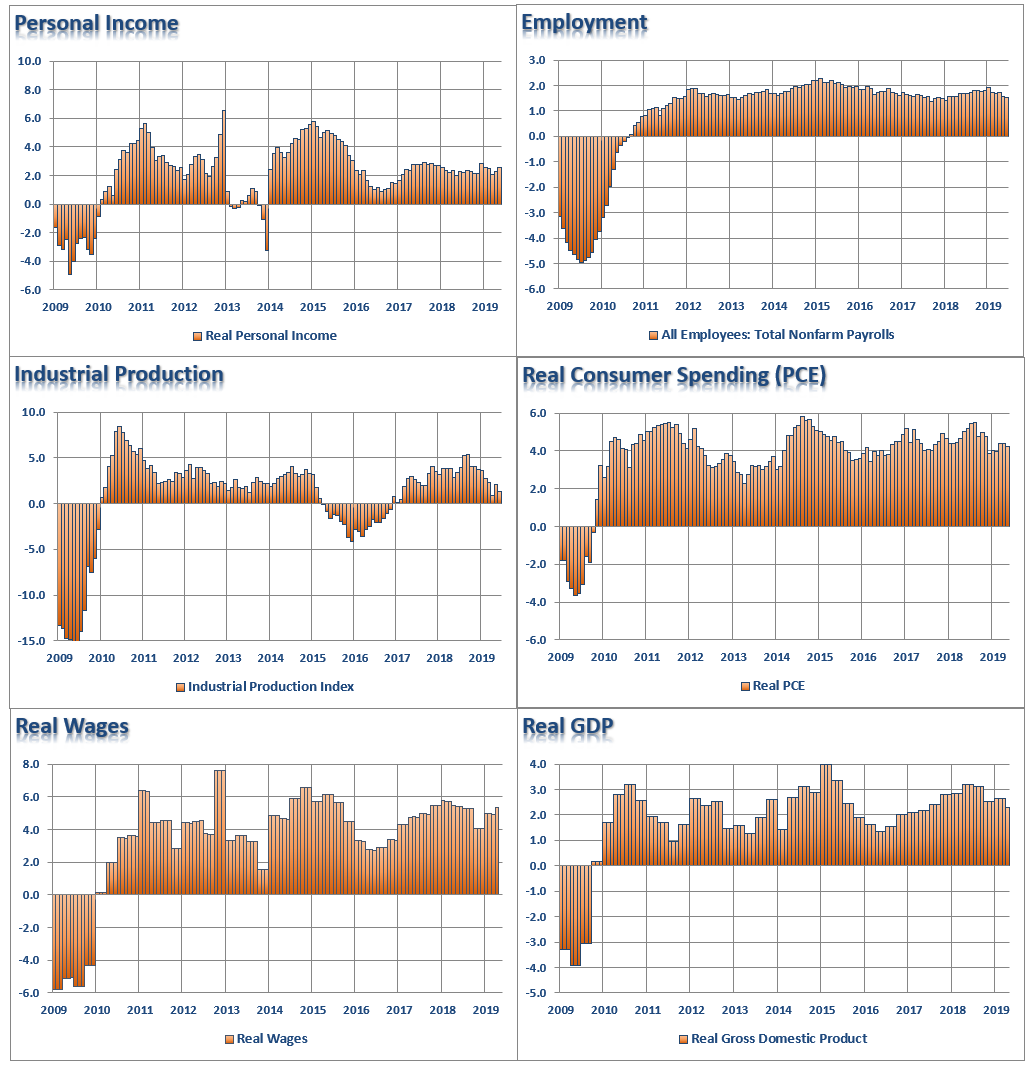

Compare the chart above with the one below.

There is a vast difference between the strength of the economy today versus 1999; particularly we are already in a longer economic expansion than we were then.

- Personal Incomes currently average about 2% versus 4% in 1995

- Employment is averaging about a 1.5% annualized growth rate versus 2.5% in 1995.

- Industrial Production has averaged about 2% annual growth vs 5% previously.

- Real Consumer Spending has averaged about 4% annual growth versus 8-10% in 1995.

- Real Wages have averaged about a 3.5 annual growth rate versus 8-10% in 1995.

- Real GDP has averaged about 2% annual growth over the last decade versus 3% previously.

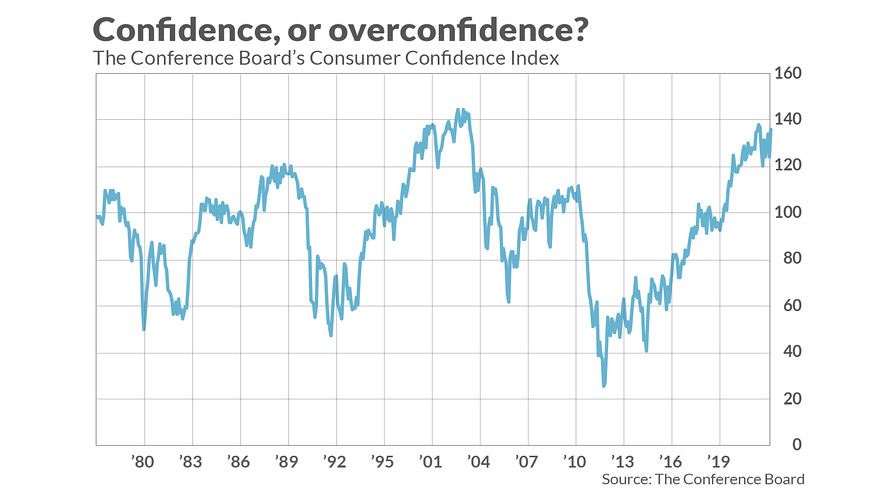

There is also one other significant difference.

In 1995, Consumer Confidence was at about 100 on its way to 140.

Today, it is likely not possible to get more optimistic than consumers are currently.

It’s All Bullish

“We could get more volatility in the coming days, but as we settle into August you’ll see equities start to perk again. My assumption is that we could start to see a buy-the-dip mentality, created by the easy money move and the need to chase returns.” – Yousef Abbasi, INTL FCStone

“Low rates will continue to support a higher-than-average valuations for the S&P 500. At the same time that corporations are growing revenue at a healthy clip and appear set to avoid the earnings recession that many investors had been fearing this year.” – Brad McMillan, CommonWealth

Not surprisingly, since the Fed’s announcement, the financial media and Wall Street have been pushing the bullish narrative. Just as they did in 1999 and 2007, as there was “no recession in sight,” then either.

The problem is financial media, or Wall Street, is they never tell you when to sell. (They don’t make money when you are in cash.)

Currently, the risk to the market is elevated.

- Confidence is at highs, not lows.

- Economic growth is at a cycle peak

- Earnings growth is beginning to weaken, and corporate profits are on the decline.

- Valuations are elevated

- Leverage is at records

-

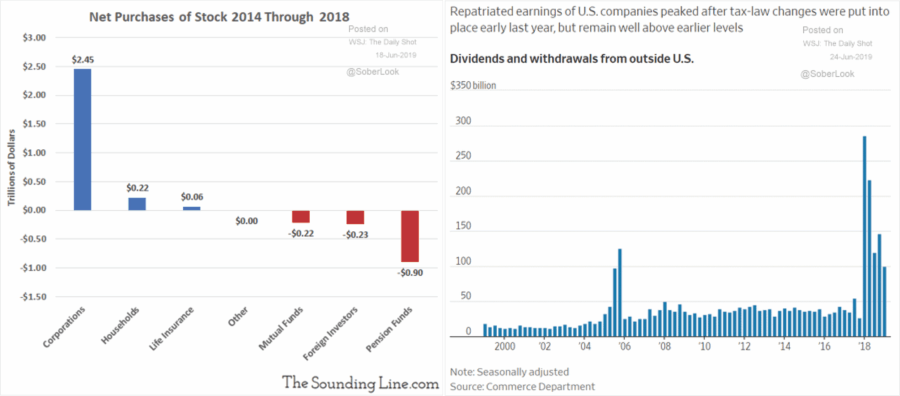

Stock buyback activity is slowing (As we noted previously, since 2014, buyback activity has accounted for nearly 100% of net equity purchases in the market and is now slowing).

While it is certainly possible for equities to push higher over the short-term, seemingly to confirm the “bullish calls,” don’t forget your time horizon is substantially longer than 6-12 months.

No one will ring a bell at the eventual top, the media won’t tell you to “sell,” and the mainstream financial advice will tell you that if your only option is to “buy and hold.”

If history is any guide, the next mean reverting event will likely wipe out of the bulk of the gains made over the last 5-7 years at a minimum.

If you are close to retirement, it should be clear that risk outweighs the reward currently.

Not everything the Fed does can be bullish.

© Real Investment Advice

© Real Investment Advice

More Factor-Based Investing Topics >