Key Points

-

Valuation has many shades—from black to white, with lots of gray in between.

-

But valuation is more of a sentiment indicator than a fundamental indicator.

-

Macro conditions (for now) support higher-than-average multiples; but earnings estimates for next year are cloudy at best.

“It is only in appearance that time is a river. It is rather a vast landscape and it is the eye of the beholder that moves.”

-Thornton Wilder

I’m often asked about equity valuations and whether the market is cheap or expensive (or somewhere in between). My answer is rarely any of the above because to some degree it depends on the valuation metric being used. But the reality is that valuation—regardless of metric—is as much (or more of) a sentiment indicator than it is a fundamental indicator. Yes, if you’re looking at a traditional price/earnings (P/E) ratio, it’s “fundamental” in the sense that there is an actual defined “E” (earnings) and of course there is always an actual defined “P” (price). However, there are times when investors are willing to pay very little for stocks and P/Es descend to historically-low levels—like in 2010-2011, when earnings were rebounding sharply, but investors remained skittish. Then there are times when investors are willing to pay exorbitant prices for stocks and P/Es ascent to historically-high levels—like in 1999-2000.

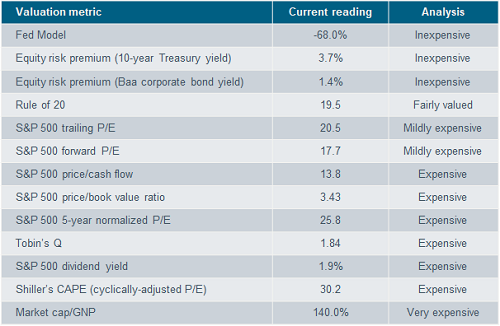

Back to the metrics; I often say, when speaking to a large group of investors, that I could find the most bearish person in the room, and the most bullish, and easily find a valuation metric they could use to support their view. Case in point is the valuation table below. It covers myriad valuation metrics many of which are familiar to investors but some are a tad more esoteric. Below the table I added in the definitions for each.

Source: Charles Schwab, Bloomberg, FactSet, The Leuthold Group, Copyright 2019 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/, as of November 29, 2019.

Definitions

Fed Model: Compares the S&P 500’s earnings yield (which is the inverse of the P/E—or E/P) to the yield on long-term U.S. government bonds. Negative readings suggest favoring stocks over bonds.

Equity Risk Premiums: Subtracts either the forward 10-year U.S. Treasury bond yield or the forward Baa corporate bond yield from the forward S&P 500’s earnings yield (E/P). Positive readings suggest stocks are undervalued relative to bonds.

Rule of 20: Stocks are considered fairly valued when the sum of the S&P 500 forward P/E ratio and the year-over-year change in the consumer price index (CPI) is equal to 20 (or inexpensive when it’s below 20).

Trailing P/E: Divides the current S&P 500 price by 12-month trailing operating earnings per share.

Forward P/E: Divides the current S&P 500 price by 12-month forward expected operating earnings per share.

Price/cash: Measures the value of the S&P 500 relative to its operating cash flow per share.

Price/book: Divides the S&P 500 price by the book value of its components per share.

5-Year Normalized P/E: Uses four years of historic earnings, two quarters of forward earnings; taking the midpoint between reported and operating earnings (a take on Shiller’s CAPE, but with a shorter time span, and with an adjusted earnings calculation).

Tobin’s Q: Developed by Nobel Laureate James Tobin, it’s a fairly simple concept, but laborious to calculate (calculations are done by the U.S. government and the ratio’s readings are provided by the Fed). It’s often called the Q Ratio and is the total price of the U.S. stock market divided by the replacement cost of all its companies. A high Q (greater than .85) implies overvaluation.

Dividend Yield: Compares the current dividend yield on the S&P 500 with both historic averages and the 10-year U.S. Treasury yield. At near-equivalent yields, the market is seen as fairly valued.

Shiller’s Cyclically-Adjusted P/E (CAPE): Uses an inflation-adjusted price for the S&P 500 and divides by reported earnings over the prior 10 years.

Market Cap/GNP: Considered Warren Buffett’s “favorite valuation indicator,” it’s the ratio of total U.S. market capitalization to gross national product (GNP).

Popularity contest

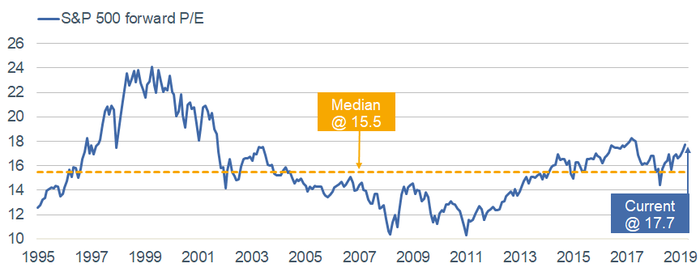

The most popular valuation metric(s) is the P/E ratio—but even with that, there are several versions as seen above. Because the stock market is ostensibly forward-looking and discounts the expected future trajectory of earnings, it’s arguably the most widely used. As you can see in the chart below, the forward P/E for the S&P 500 is currently 17.7 (meaning the index is trading at 17.7 times expected earnings over the next 12 months). Relative to the long-term (post-1995) median, that is slightly expensive—but nowhere near the nosebleed levels of the late-1990s.

Forward P/E slightly above median

Source: Charles Schwab, FactSet, as of November 29, 2019.

What about the E?

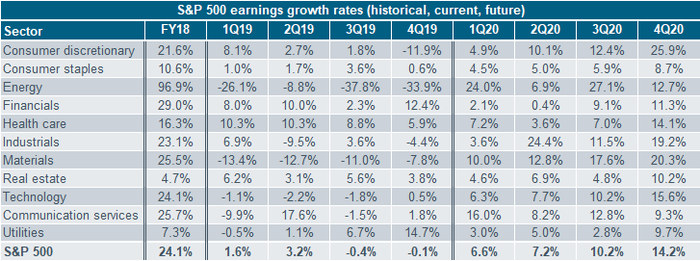

A rub in the current environment is that there is a debate raging among analysts and strategists about the validity of earnings expectations for next year. Those with more bearish leanings believe earnings-per-share (EPS) estimates are too high and don’t reflect the ongoing effect of the trade war and tariffs. Those with more bullish leanings believe that there is a likely Phase I trade deal pending, that the planned December 15 tariffs won’t kick in, that global manufacturing may be troughing, and that EPS may have upside next year.

Below, you can see the trajectory of EPS expectations from Refinitiv—showing the possibility of an “earnings recession” courtesy of negative earnings in both the third and fourth quarters; with a pickup to double-digit growth by next year’s second quarter. I do believe trade, tariffs and the fate of the December 15 tariffs (which target a vast number of consumer-oriented goods) will decide the fate of EPS expectations. However, I won’t do the impossible and try to predict the outcome of the ongoing trade negotiations.

Source: Charles Schwab, I/B/E/S data from Refinitiv, as of November 27, 2019. Forecasts are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Macro support

Most macro conditions do continue to support multiples at the higher end of any normal range—with low interest rates, low inflation and the Federal Reserve on hold for now. Low bond yields mean equities are inexpensive on a relative basis (to Treasuries and/or corporate bond yields; as seen in the valuation table in the beginning of this report). A change in those macro conditions—like higher inflation expectations—and/or a deterioration in EPS expectations in 2020, could put some downward pressure on multiples.

My colleague Kathy Jones wrote about a similar topic in her Sunday evening (internal) missive:

“Ever since the Federal Reserve reversed course and began easing policy, markets have enjoyed smooth sailing. It looks like it can last a while, since we don’t anticipate a shift in central bank policies any time soon. The problem is that market valuations become skewed in environments like this. Low interest rates and high liquidity encourage risk-taking and yield-seeking. Asset valuations become elevated and investors become complacent.”

I’ll end with another quote, from Joan Jett (today’s report title is thanks to her as well):

“You want to have butterflies in your stomach, because if you don’t, if you walk out onstage complacent, that’s not a good thing.”

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

©2019 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab & Co.

© Charles Schwab

Read more commentaries by Charles Schwab