Recent hiccups in U.S.-China trade talks and uncertainty around a “phase one” deal have reaffirmed that trade headlines continue to drive larger market swings.

Key U.S. economic data has been on the weaker side—holding the United States back from participating in an emerging global manufacturing recovery.

Negative interest rates around the world have created favorable financing conditions for manufacturing firms, harboring the global labor market from a downturn.

“The noblest pleasure is the joy of understanding.” —Leonardo Da Vinci

Reality check

After a near-two-month lull on the trade news front, a surge in investor optimism, and reduced fears of a near-term recession, U.S. stocks remain fairly elevated but are off their all-time highs. Trade tensions between the United States and China briefly resurfaced after recent reports that a “phase one” deal may not happen by year-end, and no decision has been made to delay or roll back the December 15 tariffs. Accompanied by November’s weaker U.S. manufacturing and construction data, renewed trade uncertainty helped stoke fears that an uptick in domestic economic growth may not be as imminent as many had hoped. The initial rally to new highs for U.S. stocks was led by cyclical sectors, but some defensive sectors have since taken back the lead; suggesting that investors are not fully convinced of a near-term economic rebound.

Aside from the ongoing tug-of-war between cyclical and defensive sector leadership, small-cap stocks have failed to meaningfully break out and overtake their large-cap peers; and international indexes have not confirmed the new highs seen in the United States. Nonetheless, U.S. stocks have mostly ignored mediocre economic data and weak earnings growth; focusing instead on trade optimism. In turn, some measures of valuation have climbed quite markedly; and we may be approaching a point when earnings growth will have to do more of the market’s heavy lifting. [Read how valuation is as much a sentiment indicator as it is a fundamental indicator in Any Weather: Valuations Say Stocks are Cheap and Expensive].

Growing global

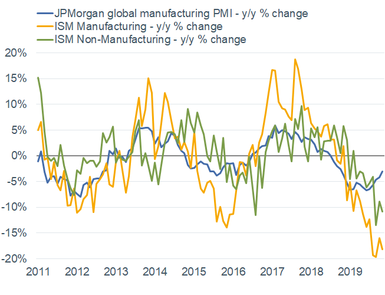

The aforementioned weakness in U.S. manufacturing reinforces the narrative of the still-firm dividing line between the manufacturing and services sectors. November’s Institute for Supply Management (ISM) Manufacturing Index missed consensus estimates and fell to 48.1; while the Non-Manufacturing Index ticked down to 53.9. Though the latter also missed estimates, the overall level remains above 50, which separates expansion from contraction and suggests that services remains relatively strong. Given the still-healthy consumer and gradual fading of trade tensions, investors had hoped for a pickup in activity synonymous with the recent improvement in global manufacturing data. As you can see in the chart below, the global Purchasing Managers’ Index (PMI) has continued to rebound on a year-over-year basis; thus diverging from the U.S. manufacturing and services measures. By no means does this suggest the entire globe has shifted into growth mode, but data of late has trended favorably.

Global Manufacturing Is Showing Some Signs of Life

Source: Charles Schwab, Bloomberg, Institute for Supply Management (ISM), IHS Markit data as of 12/4/2019.

Some pundits and investors have dismissed still-soft manufacturing, pointing to its increasingly-smaller share of the total U.S. economy. Yet, the reality is that it is more cyclical in nature—with a higher correlation to corporate profits—and tends to lead the rest of the economy. In other words, manufacturing punches above its weight. Absent a meaningful rebound in soft or survey-based measures (such as the ISM indexes) and hard data (such as industrial production and business investment), manufacturing’s malaise may start to spill over into services, with employment being the main transmission mechanism. Fortunately, the labor market has remained firm. November’s strong jobs report from the Bureau of Labor Statistics (BLS) showed an increase of 266k nonfarm payrolls, which beat the consensus estimate of 180k. Average hourly earnings ticked down to 0.2% month-over-month, but the year-over-year figure moved up to 3.1% after October’s upward revision to 3.2%; and the unemployment rate edged down to 3.5%. Job growth at the sector level was broad-based, with manufacturing leading the gains—perhaps unsurprising, considering the GM strike has ended. For now, on the employment front, we can say so far so good.

Just another mini-slowdown?

Among the myriad economic data that hit the press around the Thanksgiving holiday were the revisions for third quarter gross domestic product (GDP) growth. Original estimates from the Bureau of Economic Analysis (BEA) showed a 1.9% annualized growth rate, which was revised upwards to 2.1%. Strength in revisions wasn’t broad-based, though, as inventories accounted for nearly the entire increase; while imports and state & local government spending were revised downwards. Though revisions surprised to the upside, growth expectations for the fourth quarter suggest further slowing in the economy—as the Atlanta Fed’s latest GDPNow forecast came in at 1.5% as of December 5, 2019.

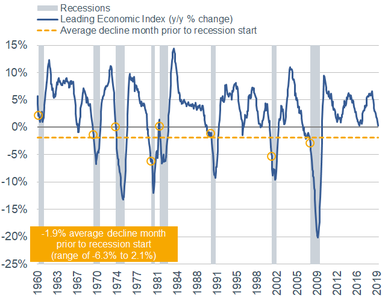

Corroborating weaker expectations has been the continued decline in The Conference Board’s Leading Economic Index (LEI). You can see from the chart below that the LEI’s trend—as measured on a year-over-year basis—has been falling since late 2018. It’s now at a lower level than the prior two slowdowns in growth.

Another Descent for the LEI

Source: Charles Schwab, Bloomberg, The Conference Board data as of 11/21/2019.

While the LEI’s weakness suggests we are later in the economic cycle, we haven’t yet reached the average level that has signaled past recessions. In other words, the LEI is not in the “danger zone,” as denoted by the orange dotted line. The jury is still out as to whether this is just another mini-slowdown (similar to 2011 and 2016) or something worse, so data in the next few months will give a more certain tell about growth prospects. Our view has been—and continues to be—that trade is the biggest needle-mover with regards to how much longer this cycle can last. Should uncertainty persist and a deal remain elusive, corporate confidence will likely remain under pressure and further strain investment; potentially affecting the consumer and labor market. Any détente or “skinny” deal would likely, at best, herald a stabilization in growth.

Trade has been a tough trade

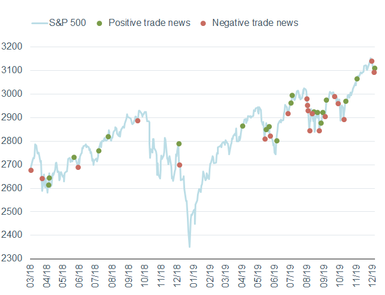

Up until last week, investors had grown increasingly optimistic and complacent that a “phase one” U.S.-China trade deal was near completion and would be signed by year-end. No news had been the best news, as the silence from both Washington and Beijing for most of October and November helped push the market to new highs. Yet, stocks resumed choppy trading after renewed hesitation that a deal was to be completed this year—bringing uncertainty back into the light and confirming that the market is still largely beholden to trade news; as you can see in the chart below.

Trade Has Dictated Market Moves

Source: Charles Schwab, Bloomberg data as of 12/5/2019. Past performance is no indication of future results.

While trade optimism has at times provided a meaningful lift to stock prices, the bite has clearly been equally as painful. In fact, as per our own findings, the market has moved (in points traveled terms) nearly twofold on days when trade news is front and center, compared to days when there are no major headlines. Thus, as we have warned in prior reports, trading around short-term trade news has proven to be quite a treacherous task.

As the trade war’s impact on the market has been profound, such has been the case for the broader economy. Notwithstanding the material effects on GDP growth courtesy of strained business investment and a beleaguered manufacturing sector; corporate earnings, business confidence, and future planned capital expenditures have taken substantial blows. Tariffs have been a considerable drag on U.S. companies, forcing C-suites to either compress their profit margins and/or pass higher costs onto customers—an issue that will be further amplified should the December 15 tariffs (which directly hit consumer goods) kick in. China has experienced similar setbacks and, while there is a serious debate as to who is “winning” the trade war, weak manufacturing and economic data in both countries prove that there are no winners.

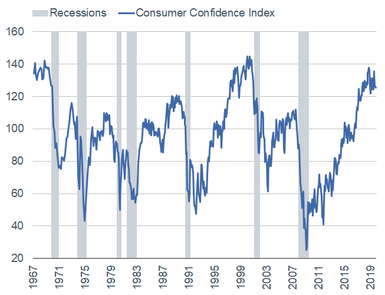

For the most part, the U.S. consumer has remained relatively strong, save for some deterioration in hours worked and paltry wage growth. As you can see in the chart below, consumer confidence remains elevated and has stayed in a tight range since the start of the trade war, which stunted its climb in late 2018.

Consumers Are Waiting for Positive News

Source: Charles Schwab, Bloomberg, The Conference Board data as of 11/30/2019.

Further escalation in trade tensions and/or the implementation of the December 15 tariffs could hurt the stock market and hike prices on consumer goods—thus leading to a pullback in spending and weaker confidence. You can see that a significant decline in confidence has historically not bode well for the economy; and since the consumer has been among the few bright spots, any meaningful deterioration in confidence might shorten the runway between now and the next recession.

Taking inventory of the labor market

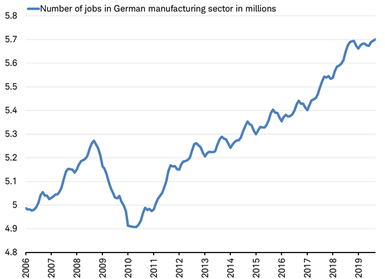

It seems to be a mystery: why has the world’s labor market been so strong in the face of weakening global growth and a manufacturing recession? From Canada to China, employment has been consistently resilient across major economies. Remarkably, strength in the labor market has persisted even where the global economy is weakest—such as Germany, where employment is at an all-time high in the manufacturing sector, as you can see below. This labor market resilience has supported consumer spending and has kept the global economy from sliding into a broad recession. But why has it been so strong and how long might it last?

What Recession? Number of German Manufacturing Workers at All-Time High

Source: Charles Schwab, Bloomberg data as of 12/4/2019.

After 15 straight months of declines, global manufacturing PMIs have recently stabilized due to trade deal optimism, but actual demand hasn’t improved. As a result, unsold inventory has been growing in most major countries. The world’s three largest developed economies highlight the growing global stockpiles: in the United States, the inventory of durable goods is growing at nearly a 5% pace; the orders-to-inventory ratio remains below 1.0 in Japan (as per Bloomberg); and the Information and Forschung (Ifo) Institute inventory assessment in Germany has recently hit the highest level since the global financial crisis, as you can see in the chart below.

German Unsold Inventories Highest Since “Great Recession” of 2008-09

Source: Charles Schwab, Bloomberg data as of 12/4/2019.

Historically, when demand softens, employers often reduce output through job cuts—especially in manufacturing industries where excess inventories are costly to maintain and weigh on pricing. Yet, nearly two years into this slowdown, there are few signs companies are cutting payrolls. This cycle may be different, as financing the production of unsold inventory in a world of negative interest rates may be more attractive than laying off workers. Inventory financing costs in recent years have been low by historical standards and may even be at all-time lows. With negative real interest rates, businesses can borrow to finance inventory at a lower rate than the pace at which that inventory is inflating in value—resulting in a positive impact on profits. This is unique to this business cycle and could explain why the labor market has remained strong nearly two years after sales began to weaken.

But there is a limit. Businesses can’t recognize the gain until the inventory is sold. Without a trade deal, the heightened tensions that have contributed to the slowdown in demand may not ease. A failed “phase one” U.S.-China deal by December 15—when the next tranche of tariffs goes into effect—could force businesses to finally begin shedding payrolls, undermining the key support for the global economy.

So what?

U.S. stocks continue to trade near their all-time highs but recent hiccups in trade talks have re-emphasized that a deal remains elusive, decisively unpredictable, and incomplete. Key components of the first phase have yet to be put in writing and major structural issues—such as intellectual property theft and forced technology transfers—will remain unaddressed for the foreseeable future, confirming that little-to-no material progress has been made. Persistent uncertainty has proven to be a significant strain on business confidence and spending, especially in the United States. Yet, the rest of the globe is showing nascent signs of emerging from the growth slump—bucking the usual trend of following the lead of the United States. Considering sluggish domestic growth expectations and a trade scenario that can tip in either direction, we maintain our neutral stance on U.S. equities (with a bias towards large caps relative to small caps), as well as developed and emerging market equities. We continue to encourage investors to use volatility to rebalance back to strategic long-term allocations.