Key Points

-

Although no enhanced forward guidance was provided, the Fed reiterated its commitment to support the economy with tools from the GFC-era playbook as well as new programs.

-

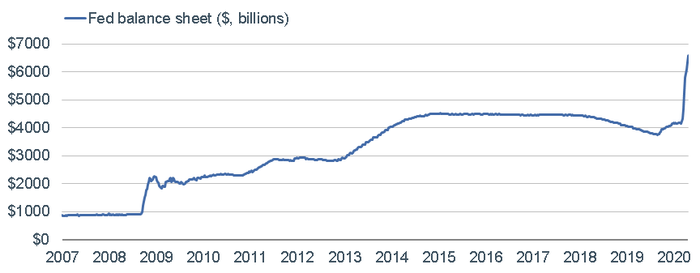

The Fed’s balance sheet has spiked to $6.5 trillion, from less than $4 trillion at the end of 2019.

-

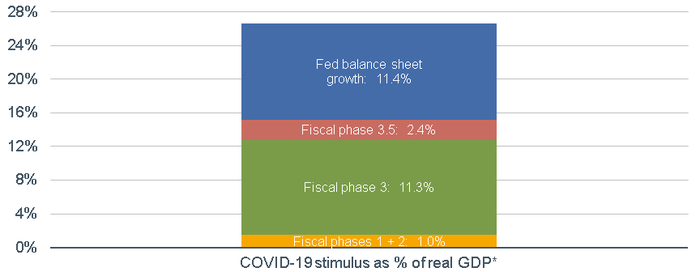

Combined with Congressional and Treasury Department actions, the relief/liquidity programs amount to nearly 25% of expected 2020 real U.S. GDP.

Following its April meeting, the Federal Open Market Committee (FOMC) restated its commitment to use its full range of tools to support the economy and to keep the fed funds rate near zero “until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.” The FOMC also announced that it will continue with its Treasury and agency securities purchases “in the amounts needed to support smooth market functioning, thereby fostering effective transmission of monetary policy to broader financial conditions.” From a peak of $75 billion per day in the third week of March, the Federal Reserve (Fed) has already slowed its Treasury purchases to $10 billion per day this week; with more easing back expected as market functionality continues to improve.

Considerable risks bring back GFC playbook … and then some

The FOMC believes that the COVID-19 pandemic “poses considerable risks to the economic outlook over the medium term” and that it “will use its tools and act as appropriate to support the economy.” Earlier today, the initial read on first quarter real gross domestic product (GDP) was released, which contracted at a -4.8% annualized quarter/quarter rate, the largest since the Global Financial Crisis (GFC) in 2008. Consensus estimates are significantly more dire for the second quarter; with an approximate range of -10% to -50% by Wall Street economists. Given this heightened uncertainty, the FOMC left unchanged its vague guidance on the future path of interest rates.

The Fed has not only used its playbook from the GFC, but significantly added to it during the COVID-19 crisis. Using International Monetary Fund (IMF) data, since March, in addition to the aforementioned rate cuts and Treasury/agency securities purchases, the Fed has:

- Expanded overnight and term repurchase agreements (repos).

- Lowered the cost of discount window lending.

- Reduced the existing cost of swap lines with major central banks and extended the maturity of foreign exchange operations.

- Broadened U.S. dollar swap lines to more central banks

- Offered temporary repo facilities for foreign and international monetary authorities

- Introduced facilities to support the flow of credit, in some cases backed by the U.S. Treasury department, using funds appropriated under the CARES Act, including:

- Commercial Paper Funding Facility to facilitate the issuance of commercial paper by companies and municipal issuers.

- Primary Dealer Credit Facility to provide financing to the Fed’s 24 primary dealers collateralized by a wide range of investment grade securities.

- Money Market Mutual Fund Liquidity Facility (MMLF) to provide loans to depository institutions to purchase assets from prime money market funds (covering highly-rated asset backed commercial paper and municipal debt.

- Primary Market Corporate Credit Facility to purchase new bonds and loans from companies.

- Secondary Market Corporate Credit Facility to provide liquidity for outstanding corporate bonds.

- Term Asset-Backed Securities Loan Facility to enable the issuance of asset-backed securities backed by student loans, auto loans, credit card loans, loans guaranteed by the Small Business Administration (SBA), and certain other assets.

- Paycheck Protection Program Liquidity Facility (PPPLF) to provide liquidity to financial institutions that originate loans under the SBA’s Paycheck Protection Program (PPP) which provides a direct incentive to small businesses to keep their workers on the payroll.

- Main Street Lending Program to purchase new or expanded loans to small and mid-sized businesses.

- Municipal Liquidity Facility to purchase short-term notes directly from state and eligible local governments.

So far, most of the ~$2.3 trillion that’s been pumped into the U.S. economy has come from the Fed’s purchases of U.S. Treasuries and mortgage-backed securities (MBS)—taking a page from its 2008 Global Financial Crisis (GFC) playbook. This has led to a rapid and significant increase in the Fed’s balance sheet, as you can see below.