Key Points

-

The FOMC kept rates steady, detailed its new average inflation targeting policy framework, and updated its economic/rates projections.

-

The economic contraction is now expected to be shallower; but the recovery thereafter slower.

-

Highlights of the post-meeting press conference included as assertion that more fiscal relief is needed.

Surprising no one, the Federal Open Market Committee (FOMC) kept interest rates unchanged near zero. However, with greater clarity and precision than in the recent past, the committee signaled it would hold rates steady through at least 2023 as an aid to the pandemic-hit economy. The mostly-dovish statement that accompanied the meeting details the Federal Reserve’s new long-term policy framework around average inflation targeting—previewed by Fed Chair Jerome Powell last month at the annual Jackson Hole Symposium. The policy aims for inflation to overshoot the 2% target, as detailed in the statement: “…with inflation running persistently below” the 2% longer-term inflation target, the FOMC “will aim to achieve inflation moderately above 2% for some time so that inflation averages 2% over time.”

The FOMC vote was not unanimous at 8-2; with Dallas Fed President Robert Kaplan and Minneapolis Fed President Neel Kashkari both dissenting; based largely on language. Kaplan wants “greater policy flexibility,” favoring to keep in the prior language about keeping rates at current levels until the pandemic crisis has been weathered (without time specificity). Kashkari is in favor of waiting for a rate hike until “core inflation has reached 2% on a sustained basis.”

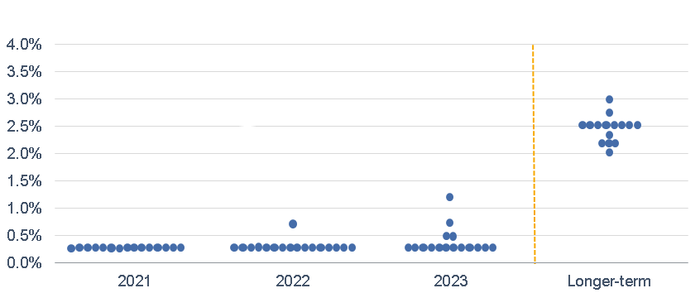

A key part of the statement: “It will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.” Also in the statement was a reiteration of the buying of U.S. Treasuries (USTs) and mortgage-backed securities (MBS) “at least at the current pace to sustain smooth market functioning.” The Committee continues to peg those amounts at $80 billion of USTs and up to $40 billion of MBS. In terms of the FOMC’s updated Summary of Economic Projections (SEP), its members generally see rates staying extraordinarily low through 2023; although four officials expect at least one hike in 2023. The new “dots plot” can be seen below.

“Dots Plot” of Fed Funds Rate Expectations

Source: Charles Schwab, Bloomberg, FOMC Dot Plot, as of 9/16/2020.

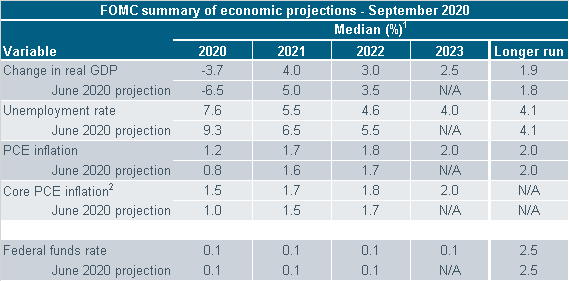

In other updates to the committee’s quarterly forecasts—which now include projections for 2023, officials see a shallower economic contraction this year relative to their prior forecasts; but a slower recovery thereafter. Their unemployment rate forecasts have improved and their inflation forecasts have ticked higher. Interestingly though is that their inflation forecasts don’t actually show any overshooting on the 2% target—giving credence to the open question many are asking about how exactly the Fed plans to stimulate higher inflation. A summary SEP table can be seen below.

Source: Charles Schwab, Federal Reserve, as of 9/16/2020. Note: Projections of change in real gross domestic product (GDP) and projections for both measures of inflation are percent changes from the fourth quarter of the previous year to the fourth quarter of the year indicated. PCE inflation and core PCE inflation are the percentage rates of change in, respectively, the price index for personal consumption expenditures (PCE) and the price index for PCE excluding food and energy. Projections for the unemployment rate are for the average civilian unemployment rate in the fourth quarter of the year indicated. Each participant’s projections are based on his or her assessment of appropriate monetary policy. Longer-run projections represent each participant’s assessment of the rate to which each variable would be expected to converge under appropriate monetary policy and in the absence of further shocks to the economy. The projections for the federal funds rate are the value of the midpoint of the projected appropriate target range for the federal funds rate or the projected appropriate target level for the federal funds rate at the end of the specified calendar year or over the longer run. 1For each period, the median is the middle projection when the projections are arranged from lowest to highest. When the number of projections is even, the median is the average of the two middle projections. 2Longer-run projections for core PCE inflation are not collected.

The statement did provide an “escape clause” highlighting that the Fed could eventually “adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals”—which was likely aimed at financial stability risks. On that note, during Powell’s post-meeting press conference, in response to a question about financial stability, he replied that “monetary policy should not be the first line of defense,” noting that regulatory tools should be on the first line.

The press conference brought many references to fiscal policy; with Powell grimly noting the millions of people still out of work, a rash of struggling small businesses, and beleaguered state and local revenue streams. Although Powell said the initial monetary and fiscal response was rapid and “effective,” his “sense is that more fiscal support is likely to be needed.” Without that support, “there’s certainly a risk … that will start to show up in economic activity.”

It was a clear message to Congress.

Important Disclosures:

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see www.schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

© Charles Schwab

Read more commentaries by Charles Schwab