Key Points

-

Stock market performance during the transition period between outgoing and incoming U.S. presidents tends to be more dependent on the economic cycle (recession, recovery or expansion) than the election results.

-

Between election day and inauguration day, foreign adversaries often choose to act in conflict with U.S. interests, testing the incoming administration and adding potential market volatility.

-

While the risk of geopolitical events in the coming weeks may be elevated, these flare-ups haven’t typically led to short-lived declines, outside of a recession.

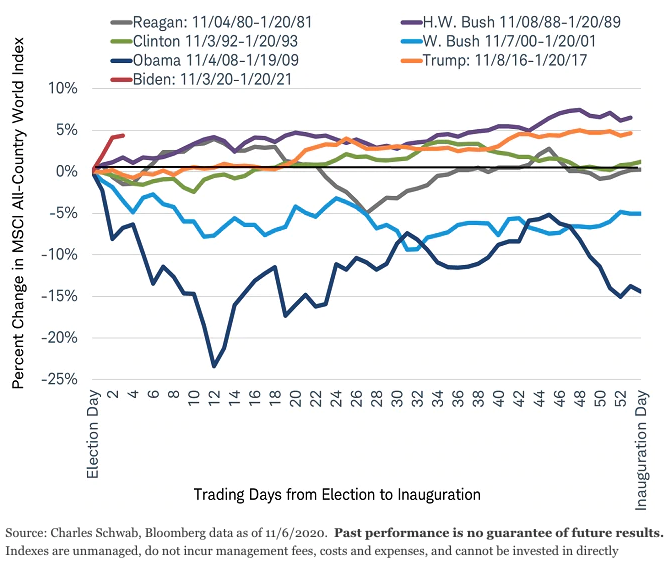

History shows us that following the election, investors seem to turn their focus back to the economic outlook. During past transition periods between outgoing and incoming U.S. presidents, the global stock market has produced both gains and losses. Whether a gain or loss took place from election day to inauguration day depended on the economic cycle: losses during recessions and gains during recoveries or expansions.

Stock market performance from election day to inauguration day

Recessions

In general, stocks tended to post gains during periods of transition to a new U.S. administration, but there were exceptions. The transitions to both the George W. Bush and Barack Obama administrations saw market declines, having taken place during the unrelated recessions and bear markets of 2000 and 2008. Recall that the stock market rally after the 2016 election occurred during a favorable period of economic expansion. However, investors may want to note that the current environment may not be as positive, given the lingering economic impacts of COVID-19.

Recoveries

The transition periods of the Reagan (1980) and Clinton (1992) administrations were more volatile. Stocks overall posted gains, but the path included short-term declines of about 5%. Similar to the current environment, these periods came shortly after recessions. The global economy had begun to recover from the recessions that ended in July 1980 and March 1991, but the stock market was still vulnerable to shocks.

The transition between outgoing and incoming presidents has often been a time when foreign adversaries choose to act in conflict with U.S. interests, testing the incoming administration. The short-lived declines in 1980 and 1992 can be traced to such geopolitical events:

- After the 1980 elections, the Iran hostage crisis came to a peak, ending in January 1981 with the release of 52 American hostages, shortly after the inauguration of Ronald Reagan.

- After the 1992 elections, 28,000 U.S. troops were sent to intervene in Somalia’s Civil War that December. In January 1993, Iraq escalated tensions by moving surface to air missiles into the no-fly zone patrolled by the U.S. and allied forces, who responded by bombing the missile sites.

As President-elect Biden and his transition team replace thousands of political appointees in January, provocative actions by geopolitical rivals have the potential for negative impacts on the stock market, given the currently vulnerable global economic recovery.

Expansions

During the transitions to the George H.W. Bush and Trump administrations in 1988 and 2016 the global economy was in the midst of a long economic expansion. However, geopolitical developments tested both market performance and incoming administrations.

- After the 1988 elections, the terrorist bombing of a commercial airliner over Lockerbie, Scotland (12/21/88) and an aerial clash that led to U.S. fighters shooting down Libyan warplanes (1/4/89) greeted the incoming Bush administration

- In 2016, China, North Korea and Syria/Iran/Russia all took actions that challenged the U.S. or its goals. In December 2016, China seized a U.S. naval drone. Syrian President Assad, backed by Russia and Iran, claimed victory in Syria’s largest city after thousands of rebels and civilians had perished in a relentless aerial bombing campaign. In January 2017, North Korea threatened to test an intercontinental ballistic missile that could potentially reach U.S. soil.

Fortunately, these events failed to disturb the global stock market, as the booming economy helped lift stocks to their strongest gains during these transition periods.

Takeaway

Drawing conclusions for the remainder of 2020 is challenging, but not because of the U.S. presidential election. Market performance during periods of transition to a new administration is more likely to be influenced by the overall economic environment. While the potential for geopolitical events in the coming weeks may be elevated, these flare-ups haven’t made investors historically bearish, outside of a recessionary global economy. This suggests that while some market participants could react to a perceived threat and take defensive actions, the moves may be short-lived if the global economy remains in recovery.

Investors are best served when grim headlines are in the news by remembering that geopolitical risks are a regular part of investing and that a long history of geopolitical developments shows us that holding a well-diversified portfolio may buffer the short-term market moves than can be the result.

Important Disclosures:

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets

Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

©2020 Charles Schwab & Co., Inc. All rights reserved. Member SIPC.

(1120-06CK)

© Charles Schwab

Read more commentaries by Charles Schwab