Inflation has been top of mind for investors throughout 2021, as a combination of supply chain disruptions and pent up demand have led to higher prices throughout the economy. The question going forward is whether these increases are transitory or permanent. In our view, the risk of sustained inflation is higher now than at any point in recent memory, and we believe that fixed income investors should adopt a defensive posture.

What Is Inflation?

The concept of inflation has evolved over time and is now generally understood to measure price changes for goods and services that are consumed – the inflation that impacts our day-to-day budgets and “feels bad.”

Importantly, increases in asset values such as home prices and equity prices are not considered in official inflation calculations. So, although one could argue that the dotcom boom of the late 1990s and the housing boom of the 2000s were both inflationary episodes, neither factored into the published numbers. These types of inflation are typically dismissed as asset bubbles, with little thought given to how they might add inflationary pressure to the broader economy.

Whether this is the right way to measure inflation and guide policy is a worthy debate topic, but is not the subject here – which is to evaluate the current “feel bad” inflation and assess whether it is transitory or persistent.

How Is Inflation Measured?

One of the trickiest aspects of inflation is that it is difficult to quantify, as the U.S. economy is both vast and complex. No single measure is able to capture price changes across such a diverse, dynamic landscape.

Probably the best-known inflation statistic is the Consumer Price Index (CPI), which measures the monthly price changes of a static basket of consumer goods as well as food and energy. Core CPI, which excludes food and energy prices, is another well-known indicator. The Federal Reserve (Fed) prefers Core CPI for its policy decisions because food and energy are both susceptible to transient supply shocks (typically caused by acts of nature). These shocks are neither reflective of economic activity nor within the Fed’s control, so they do not want them influencing interest rate policy. The Fed also uses the Personal Consumption Expenditures (PCE) Core Price Index – which tells a similar story to Core CPI.

There are several other metrics that we rely on to inform our view of inflation.

- Producer Prices – There are multiple indices that track price changes of the inputs manufacturers need to produce finished goods, and these can be predictive of consumer prices (i.e., when producer prices go up, they may be passed on to the end customer).

- Wages – Unit Labor Costs and Average Hourly Earnings provide visibility into wage inflation.

- Durable Goods – Price changes in durable goods generally reflect aggregate demand for large purchases (e.g., cars and appliances), and are particularly important because of the capitalization weighting of CPI measurement.<\li>

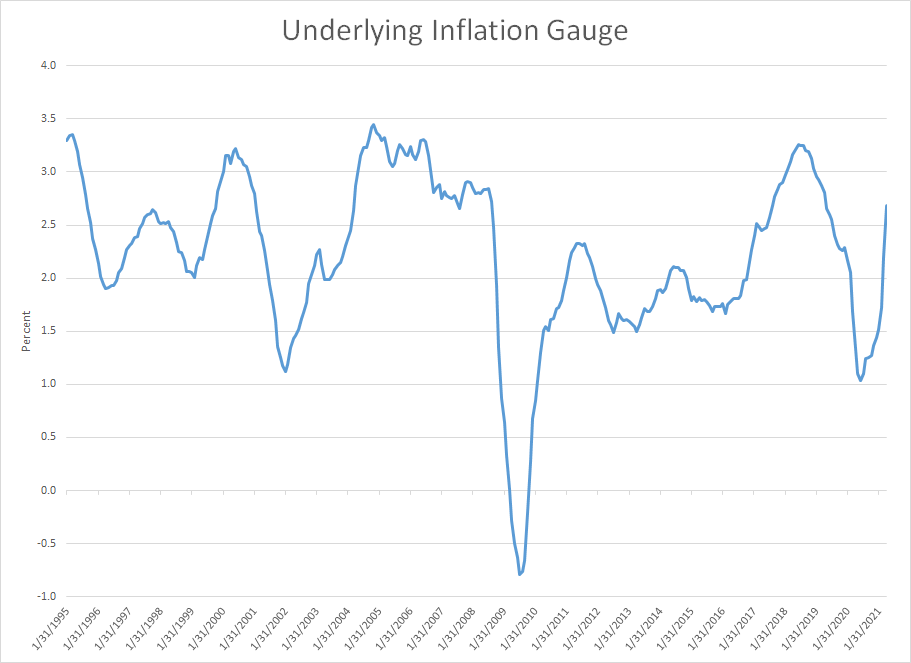

- Underlying Inflation Gauge (UIG) – a measure devised by the Federal Reserve Bank of New York specifically designed to tackle the question of predicting inflation. There are two sub-indices:

- UIG “Prices Only” – which is derived from disaggregated price series in the CPI

- UIG “Full Data Set” – which overlays macroeconomic and predictive financial data on the prices only index.

Underlying Inflation Gauge Is Flashing Yellow

The UIG Full Data time series is indicating that persistent inflation could be upon us. The index has several interesting features that lend credibility to its forecast.

- It is relatively stable, eliminating noise that plagues other series (durable goods and CPI itself)

- It was predictive of the downturn in 2008, as CPI spiked >5% in 2008 before the crash while UIG peaked in 2004-2006.

- It does NOT reflect a period of inflation persistently below 2% over the last 10 years.

Source: Bloomberg

The recent spike in UIG to 2.68% suggests a strong economic recovery as well as the potential for a material rise in inflation. This is higher than any measurement registered between 2009-2014 – the other period on record characterized by quantitative easing.

Traditional Monetary Theory Still Works

The question remains – will this persist? Specifically, why did we not witness inflation during the prior “money printing” bout of quantitative easing, and why would it be different this time? Modern Monetary Theory (MMT) has gained traction in recent years as Traditional Monetary Theory (TMT) seemingly failed during this period. To recap TMT, Gross Domestic Product is defined as:

GDP = Money Supply x Velocity of Money = Price of Output x Quantity of Output

Quantitative easing triggered a substantial increase in the supply of money, but because this was countered by a decrease in the velocity of money, there was little change in the overall GDP. In other words, printing money didn’t create a material increase in output or prices.

However, the financial health of most consumers during the first several years of QE was quite diminished, particularly relative to today. Personal balance sheets had been decimated by a combination of housing and equity market crashes. In truth, the “printing of money” largely achieved a healing of balance sheets, not a robust round of speculation – since after all, it was speculation that triggered the crisis.

It Could Be Different This Time

2021 is shaping up very differently. We have a similar concoction of zero rates and expanded quantitative easing purchases, and thus rapid expansion of money supply. However, we’re adding fiscal stimulus in excess of the prior quantitative easing period through stimulus checks and the prospect of a large infrastructure program, and we also face markets that are already showing evidence of bubbles, with equities near all-time highs, double digit gains in home prices, and massive appreciation of both cryptocurrency and collectables. In truth, perhaps there was nothing wrong with Traditional Monetary Theory to begin with, except for the assumption that printing money would directly translate into inflation.

Instead, our concern is that the current combination of monetary and fiscal policy could lead to an overshoot. Chair Powell has said the Fed will continue with its QE program until inflation is consistently above 2%, but from our perspective it seems probable it will creep higher than their target.

Recent inflation metrics have consistently printed above expectation, and the UIG measure suggests that inflation is already taking root. Continued stimulus programs at a time when markets have already fully healed – and then some – seems unnecessary and potentially reckless. A variety of forward-looking measures of inflation are establishing new highs – PPI recently printed above 6% year-over-year, and inflation sentiment indices (including University of Michigan’s survey) are flashing expectations over 4% for the next year. While many ascribe these changes to temporary supply shocks, a closer look at forward-looking measures of inflation (in particular, UIG) certainly suggests otherwise.

Final Thoughts

Obviously, we won’t know whether the current inflationary trend is transitory for at least a few more months, but we do know that the indicators we care about most are giving us pause. We are expecting inflation to persist, and we believe that investors should adopt a defensive posture with respect to interest rate risk, as rising inflation will likely lead to higher rates.

Eddy Vataru

Chief Investment Officer – Total Return

© Osterweis Capital Management

Read more commentaries by Osterweis Capital Management