Supply chains typically aren’t something the average person needs to think about too much. When they’re working, these high-tech, globalized networks of parts suppliers, assemblers, shippers, and distributors allow companies to make and move goods around the world so quickly and cheaply that it’s tempting to take them for granted.

That is, until a pandemic hits and exposes the fragility of this whole enterprise. Early on, essentials such as toilet paper, surgical masks and nitrile gloves suddenly became unavailable as surging demand gave way to panic-buying and hoarding. Later in the pandemic, lumber shortages caused wild price spikes, ruining many COVID-era home-improvement projects. More recently, news headlines report how a semiconductor shortage is driving up the price of consumer electronics and cars.

With retailers’ deadlines for ordering and stocking goods for the holiday season rapidly approaching, it’s possible shoppers just won’t be able to get everything on their list this year.

To be clear, this isn’t likely to become the new normal—though, when it might end is still uncertain. Many familiar features of modern life are implicated: Global shipping, COVID-linked worker shortages, extreme demand for limited supplies leading to price surges and inflation, and bigger transformations in our economy, including the shift to working from home, the rise of electric cars, and the potential for new infrastructure spending. So, the question now is what—if anything—can the average shopper or investor do in response?

What’s wrong with the supply chain?

Starting in the 1970s, the rise of the shipping container revolutionized global trade. These standard-sized corrugated steel boxes can stack on ships and fit on truck beds—and dramatically lowered the cost and time to transport goods. This enabled businesses to shift production to lower-cost destinations overseas and source materials and components from just about anywhere.

The steady and stable flow of inputs led companies to adopt lean “just-in-time” manufacturing, a system under which parts and materials are timed to arrive from suppliers right when they’re needed for production. This was another savings strategy, aimed at cutting the cost to store inventory.

While these developments helped make many goods more affordable, the system wasn’t prepared for the shock of COVID. Pandemic-linked shutdowns and layoffs, port closures, and disruptions in demand helped drive the biggest drop in global merchandise trade on record in the second quarter of 2020, according to the World Trade Organization.1 While the situation improved through the spring of this year, it took a turn for the worse this summer.

A traffic jam at America’s busiest ports in Los Angeles and Long Beach, which together process more than a third of U.S. goods imports, is the headline problem now.

“After dropping to less than 10 in June, the number of ships waiting in San Pedro Bay to unload peaked at 73 on Sept. 19. By the end of September there were still 67,” says Jeffrey Kleintop, Schwab’s chief global investment strategist. “Most were coming from China and took about 14 days to cross the Pacific—but then had to wait as long as several weeks for an opportunity to unload and get put on trucks.”

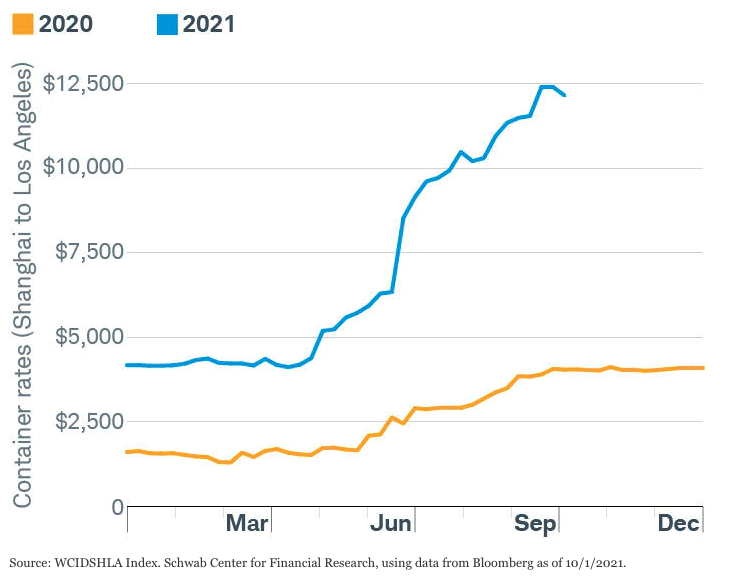

Shortages of longshoremen and truckers to haul goods to their final destinations are the primary culprits here. The backlog has pushed shipping costs to extreme levels, with the spot rate for a 40-foot shipping container from Shanghai to Los Angeles rising from about $3,500 last year to $12,500 as of the end of September.

Shipping costs have exploded

This comes as U.S. producers are already struggling to meet the strong recovery in demand for all kinds of goods after multiple rounds of government stimulus, high prices for raw materials, and worker shortages—just in time for the holiday shopping season.

“This year, suppliers need to deliver their holiday-season inventory to Amazon by November 15,” Jeffrey says. “With two weeks of transit time from the point of manufacture, plus several weeks sitting at port to unload, it could already be too late for some producers to meet the deadline.”

Impact on investors

Supply chain problems can increase risks to corporate sales, manufacturing production and consumer inflation.

“Analysts have been rapidly raising their earnings per share forecasts in recent months, after second-quarter results widely exceeded expectations,” Jeffrey notes. “Better forecasts have been supporting stocks’ historically high valuations. But as growth momentum slows and risks rise, stocks could be vulnerable to a pullback in the short term.”

Because our economy is so dependent on trade, few sectors of the stock market are immune to these risks, though some, such as financials and utilities, may be better placed than others.

“The consumer discretionary sector faces the strongest headwinds, as these companies—including car, home appliance, apparel and luxury brands—tend to be the biggest importers,” says David Kastner, senior investment strategist at the Schwab Center for Financial Research. “But any industry that needs imported machinery, electronics, or semiconductors, in particular, faces a potential revenue hit from supply chain problems.”

Longer-term trends in our economy are also contributing to increased demand for goods already in short supply. For example, as more people work from home, more workers will need computer hardware upgrades. The 5G buildout means communications services companies need more routers and other gear. The health care sector relies on imported drugs and medical equipment. The industrials sector needs machinery for construction, which also bears on real estate and, potentially, any new infrastructure spending that comes out of Congress this year.

“It might seem dire, but it’s worth noting that some of the current backlog is linked to the seasonal surge in shipping before the holidays, and business leaders are saying they expect things to improve,” David says. “Markets look forward, and even now are looking beyond this crunch. Share prices already reflect a lot of this optimism, although they could decline if the difficulties last longer than expected.”

Given the breadth of the impacts across sectors, it may not be possible to completely insulate your portfolio from supply chain problems. However, investors looking to partially offset some of this risk could consider European stocks.

“Europe could dodge the worst of this situation for three reasons,” says Jeffrey. “First, European business leaders made relatively fewer mentions of shortages hurting their businesses over the summer than their U.S. counterparts. That means less risk to sales.”

“Second, Europe’s supplier delivery times improved slightly over the summer, while those in the United States, United Kingdom and Japan worsened. That means less production risk,” he adds. “Finally, inflation pressures are lower in Europe than in the U.S.”

What can shoppers do?

The situation for shoppers is a little different, as looking ahead isn’t always an option for certain purchases.

“Supply chain crunches and general inflation create similar problems, practically speaking,” says Chris Kawashima, CFP®, a senior research analyst at the Schwab Center for Financial Research. “Prices have gone up, so what do you do? Essentially, these are cashflow and budgeting issues.”

The first thing is to try to determine whether a price increase is transitory or something you’ll need to adjust for permanently. If it’s transitory and the item you’re looking to buy is a “want” more than a “need,” can you wait it out? If it’s a “need,” can you make it work with your budget, or do you need to adjust?

Chris identifies three budgetary levers you can manipulate in response to supply chain dislocations:

-

Cut spending elsewhere. If the cost of a necessity or even a strong “want” has gone up significantly, you could consider reducing spending in other areas. Is there another “want” you can sacrifice?

-

Add income. Do you have options for putting more spending power behind your budget?

-

Work with your existing budget. Can you buy less of an item or an alternative without cutting spending elsewhere?

“That last point is actually where you can get pretty creative without disrupting your budget,” Chris says. “For example, maybe you could consider used items instead of new. Look for sales. Or if you have a few extra dollars, maybe bring some of your future purchases forward, especially if it means getting a discount. If you normally buy a month’s supply of something, consider buying a three months’ supply in bulk if the price is right.”

The final step is just to acknowledge that supply chain problems could put more demands on your dollars in the coming months, so it could be worth it to increase your cash cushion.

1“Trade shows signs of rebound from COVID-19, recovery still uncertain,” World Trade Organization, 10/6/2020.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Investing involves risk, including loss of principal.

All corporate names are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

(1021-176W)

© Charles Schwab

Read more commentaries by Charles Schwab