No Quarter (For Consistency)

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThere is no shortage of headwinds facing both the market and the economy: the tragic Russian invasion of Ukraine and attendant commodity/energy crisis; the Federal Reserve's transition from accommodative to tighter monetary policy; and increased chatter of a recession on the horizon; among others. Yet, over the past month, stocks have rallied sharply, coming close to erasing their year-to-date losses.

Whether this proves to be a rally in the midst of a bear market, or the end of a corrective phase and start of a leg higher, remains to be seen. Regardless, attempting to guess the short-term moves of the market is always treacherous; so, let's stick with what we know and assess the health of the rally.

Taking stock

From their own respective troughs, the major indexes have experienced sharp gains:

- S&P 500 (since its trough on March 8th) has gained 9%

- NASDAQ (since its trough on March 14th) has gained 13%

- Russell 2000 (since its trough on January 27th) has gained 8%.

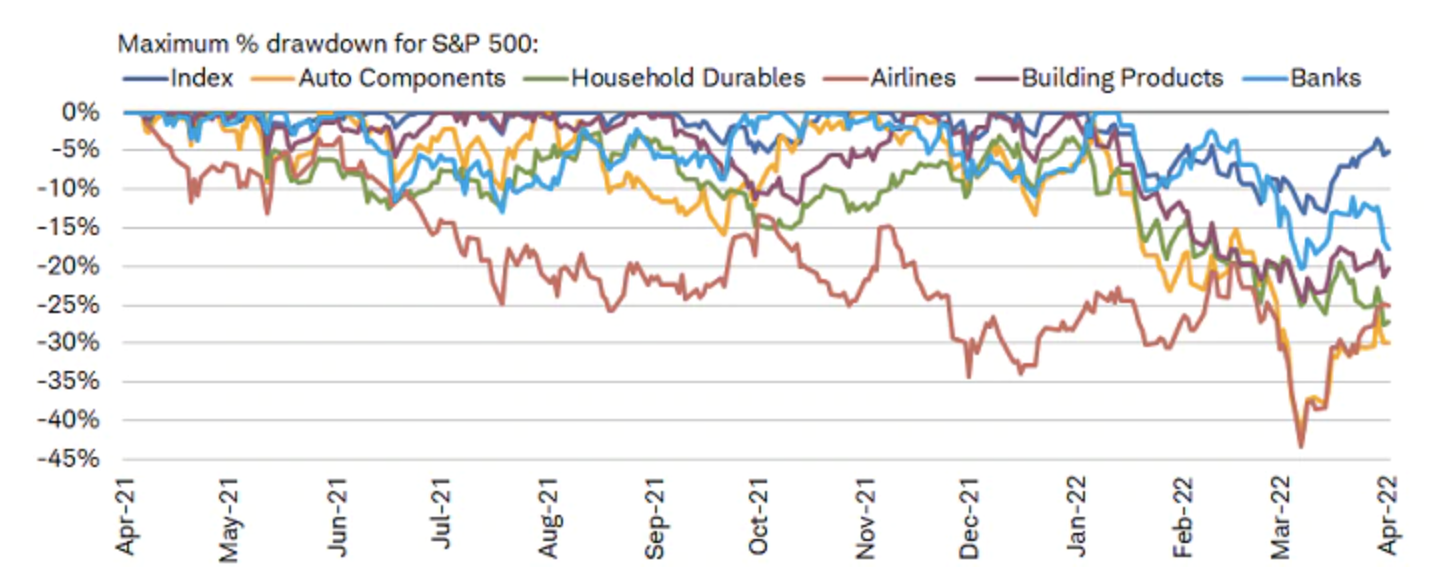

Those moves are impressive when considering—on a year-to-date basis—all three indexes have undergone a traditional correction (a decline of at least 10%), and the NASDAQ and Russell 2000 did experience traditional bear markets (a decline of at least 20% from a high), as shown in the table below. Individual member performance within those benchmarks has been worse, with the average member's maximum drawdown from year-to-date highs ranging from -19% to -29%, and from 52-week highs ranging from -25% to -46%.

Source: Charles Schwab, Bloomberg, as of 4/1/2022. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results. Some members excluded from year-to-date return columns given additions to indices were after January 2022.

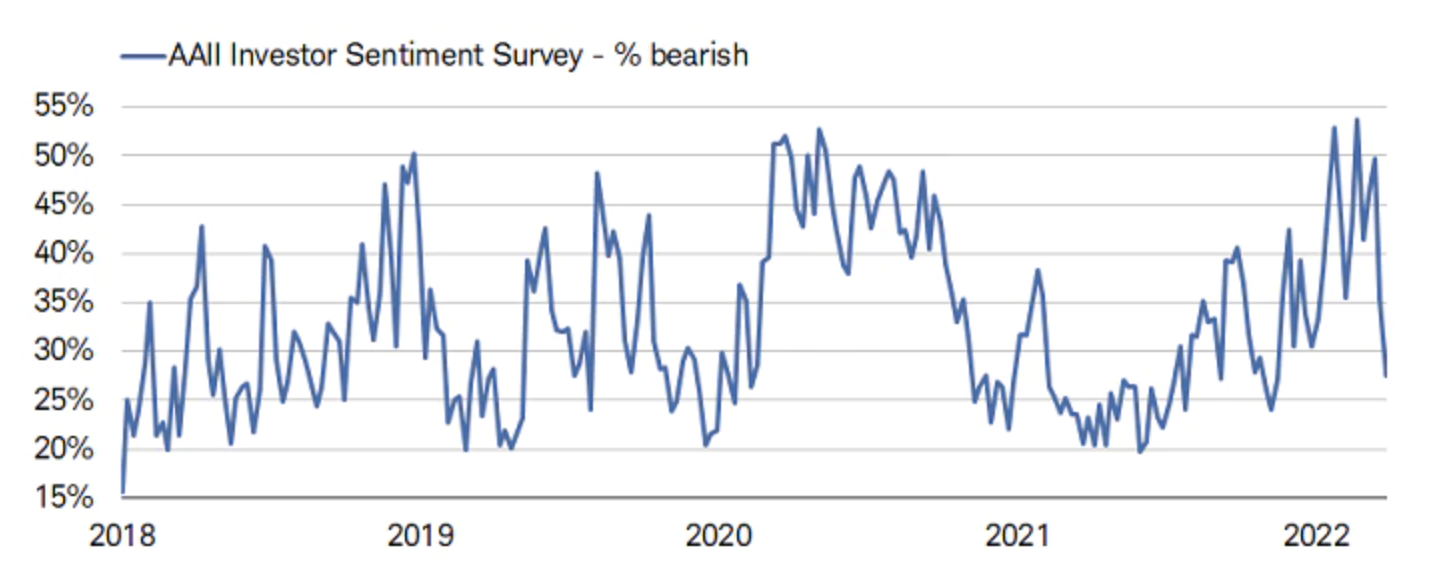

As we often highlight, investor sentiment—a contrarian indicator at extremes—can help establish both short-term troughs and peaks for the stock market. Shown below is the percentage of bearish respondents to the weekly American Association of Individual Investors (AAII) survey of its members. Bearishness hit a relative low of less than 25% last November and had only lifted to 30% as 2022 began. That may have served as a contrarian indicator for stocks, which began to fall under the weight of monetary policy and geopolitical uncertainty. By the time Russia invaded Ukraine on February 24th, bearishness had surged to nearly 55%, perhaps serving as a contrarian indicator for stocks in the other direction. The move back down to 27% suggests most of the recent pessimism has retreated and could be a setup for more weakness.

Low bearishness again

Source: Charles Schwab, Bloomberg, as of 3/31/2022.

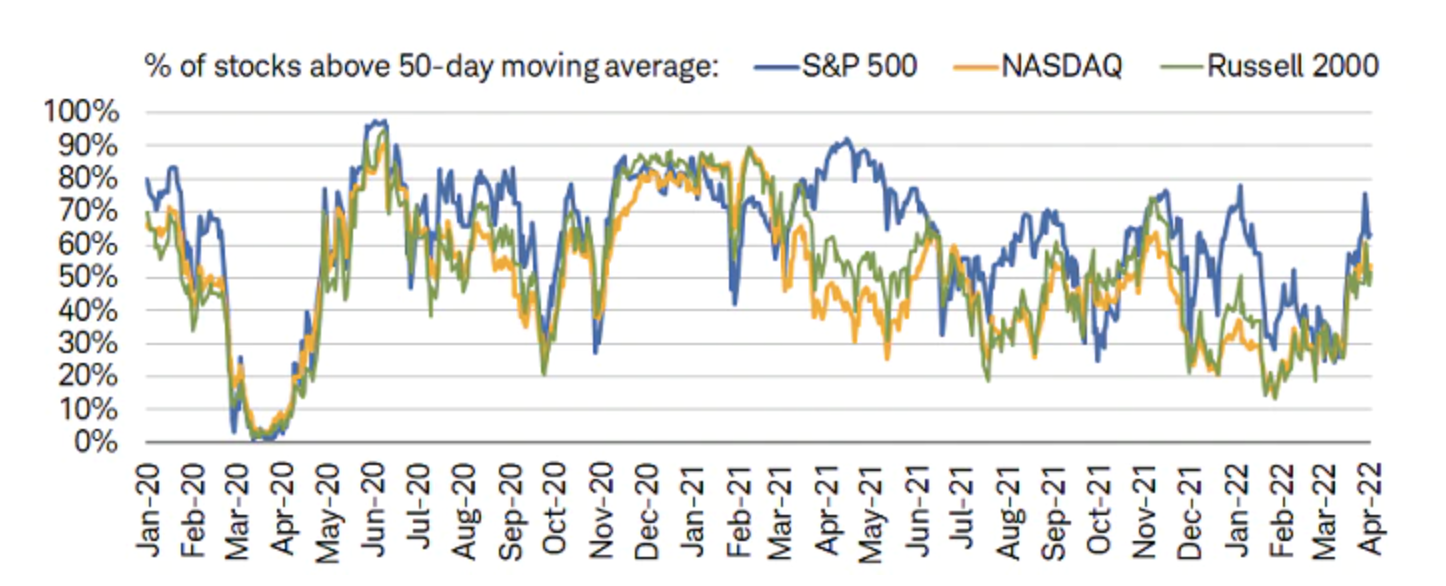

At the surface level, participation during the latest rally has been fairly strong. As shown in the chart below, the percentage of index members trading above their 50-day moving averages has climbed sharply, relative to much more anemic percentages at the beginning of March.

Short-term breadth up sharply

Source: Charles Schwab, Bloomberg, as of 4/1/2022. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

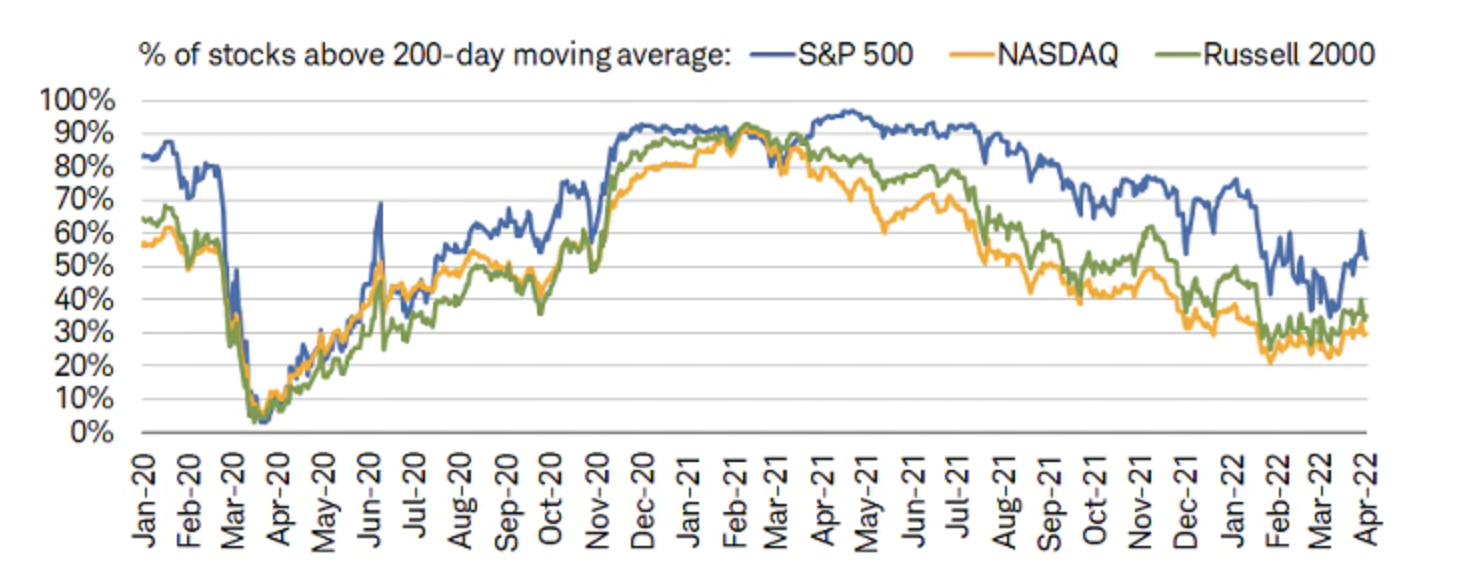

Breadth starts to look a bit weaker when we broaden the scope to the percentage of stocks trading above their 200-day moving average, shown below. There has, so far, been less of an improvement, with the S&P 500 having led the way while the other two indexes have yet to match its strength.

Long-term breadth improving

Source: Charles Schwab, Bloomberg, as of 4/1/2022. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

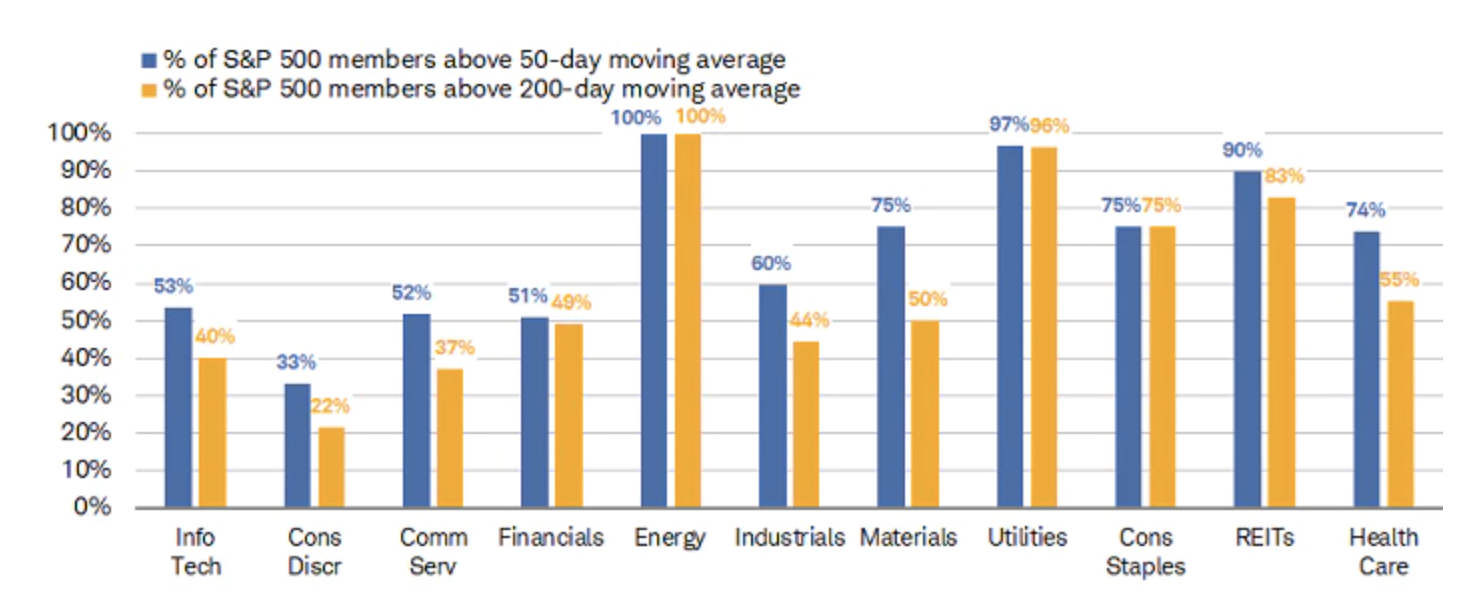

Another hint of weakness shows up in the sector breakdown for the S&P 500. As shown in the next chart, traditionally defensive areas such as Utilities, REITs, and Consumer Staples experienced strong participation among their members, which is at odds with the strength (or lack thereof) in the traditionally cyclical areas like Financials, Industrials, and Materials. The Energy sector is indeed a cyclical sector but remains an outlier given it has, unsurprisingly, benefited from the surge in oil prices this year.

Breadth gets defensive

Source: Charles Schwab, Bloomberg, as of 4/1/2022. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

In search of quality and quantity

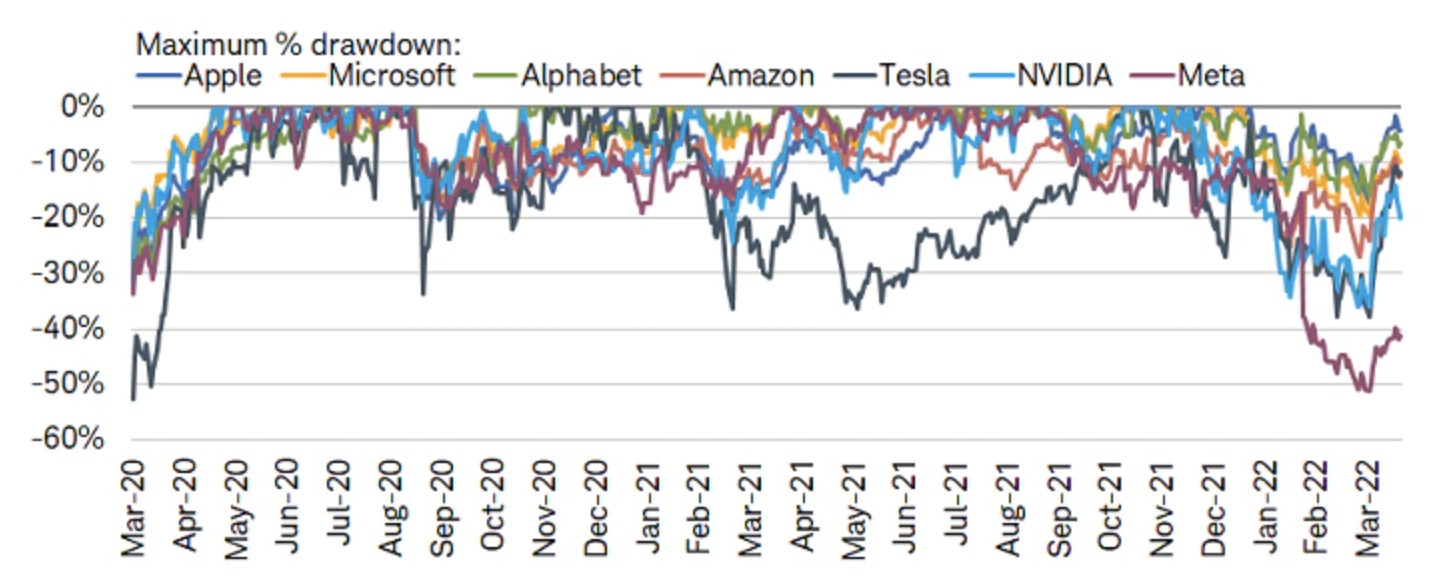

Similar to what we saw after the pandemic trough on March 23rd, 2020, some of the largest tech- and tech-related members in the S&P 500 by market cap—dubbed the "super 7" and shown in the chart below—have helped propel the index's rebound. It remains debatable whether their current outsized contributions are healthy. There was a stronger justification in March 2020, given the economy was shut down and we were living almost solely in the spheres represented by these companies. The differences today are stark, though, given a broader reopening has been underway for the better part of a year and the worst of the pandemic is hopefully behind us.

Supersized rebound

Source: Charles Schwab, Bloomberg, as of 4/1/2022. Individual stocks are shown for illustration purposes only. Past performance is no guarantee of future results.

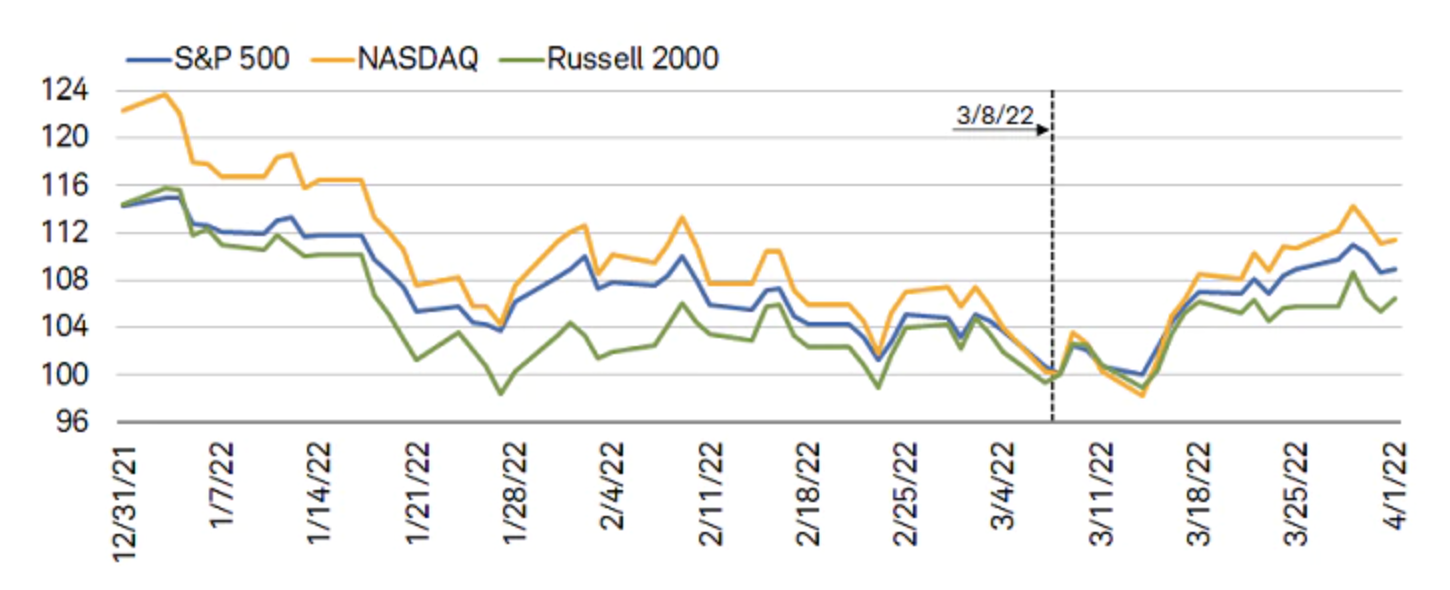

Moving to the not-as-good news, let's dissect some of the best performers within the indexes. Shown in the pair of charts below is the performance for several benchmarks before and after the S&P 500's trough on March 8th. All three major indexes are up by at least 5% from the trough (nearly 12% for the NASDAQ).

All aboard the rebound

Source: Charles Schwab, Bloomberg, as of 4/1/2022. Data indexed to 100 (base value = 3/8/2022). An index number is a figure reflecting price or quantity compared with a base value. The base value always has an index number of 100. The index number is then expressed as 100 times the ratio to the base value. Past performance is no guarantee of future results.

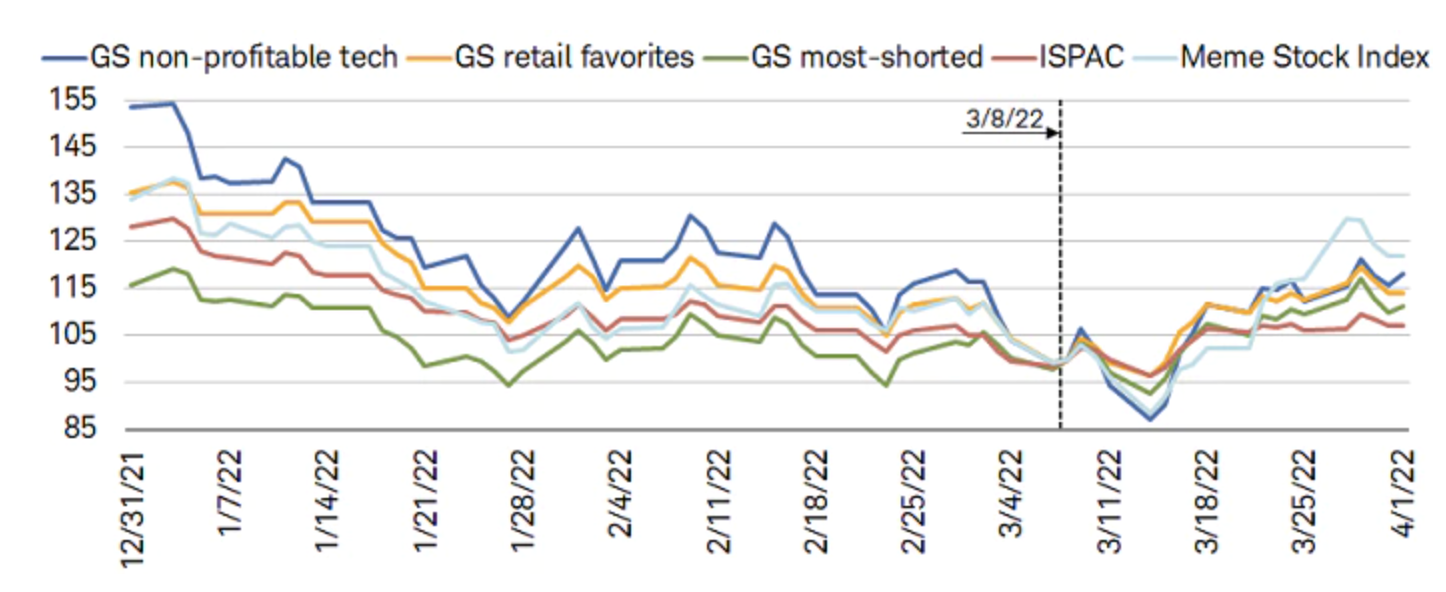

The rub is that some of the most speculative and arguably low-quality segments of the market have outperformed the major indexes markedly over the same timeframe. As shown below, non-profitable tech stocks, meme stocks, SPACs, and heavily shorted stocks have had much stronger gains—some well into double-digit percentage territory, with the memes leading the way.

Spec has driven rally

Source: Charles Schwab, Bloomberg, as of 4/1/2021. Data indexed to 100 (base value = 3/8/2022). Goldman Sachs (GS) non-profitable technology basket consists of non-profitable U.S.-listed companies in innovative industries. Technology is defined quite broadly to include new economy companies across GICS industry groupings. Goldman Sachs (GS) retail favorites basket consists of U.S. listed equities that are popularly traded on retail brokerage platforms. Goldman Sachs (GS) most-shorted basket contains the 50 highest short interest names in the Russell 3000; names have a market cap greater than $1 billion. ISPAC Index is a passive rules-based index that tracks the performance of the newly listed Special Purpose Acquisitions Corporations ("SPACs") ex-warrant and initial public offerings derived from SPACs since August 1, 2017. The Meme Stock Index includes 37 highly-traded and popular stocks that became of interest on the part of retail investors throughout various social media sites. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance does not guarantee future results.

The outperformance in those areas may make it seem that the low-quality rally is concentrated in more arcane pockets, but if we zoom out to look at the market in its entirety—proxied by the Russell 3000—the thesis still holds.

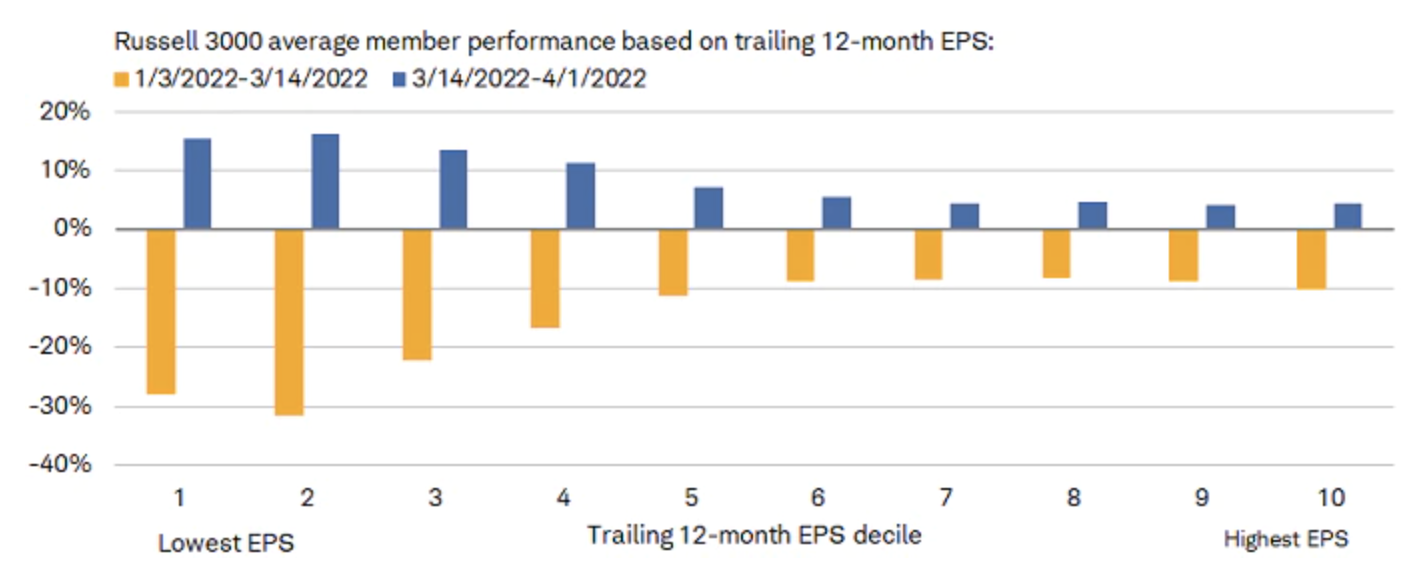

The chart below shows performance for two periods: the peak on January 3rd this year to the trough on March 8th (yellow bars) and the rally since the trough (blue bars). Performance is broken up by earnings per share (EPS) growth decile, with decile 1 representing no or negative EPS and 10 representing the highest EPS. As shown, the members on the weaker end of the EPS spectrum were hit the hardest from peak to trough, but have led the subsequent bounce higher. In other words, this is looking more like a mean reversion trade than the start of a new era of lower-quality leadership.

No EPS? No problem (for now)

Source: Charles Schwab, Bloomberg, as of 4/1/2022. Past performance is no guarantee of future results.

Historically, lower-quality segments of the stock market—including non-profitable companies—have launched into leadership positions when there is an expectation of accelerating economic growth. That is not a safe bet in the current environment. At the industry level, shown below, economically sensitive areas have not held up as well as the broader S&P 500 index. Given the brutal start for the bond market this year, selling there has been a key source of buying pressure for equities. However, earnings will start to matter again (soon, given first-quarter reporting season is about to be underway).

Cyclical industries lagging

Source: Charles Schwab, Bloomberg, as of 4/1/2022. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

The uniquely tricky phase the markets are in contributed to our recent decision to temporarily "neutralize" our tactical asset and sector allocation recommendations. Instead, we are suggesting investors utilize the diversification associated with their strategic allocations—and the periodic rebalancing needed to keep those in line with targets—to navigate the current environment.

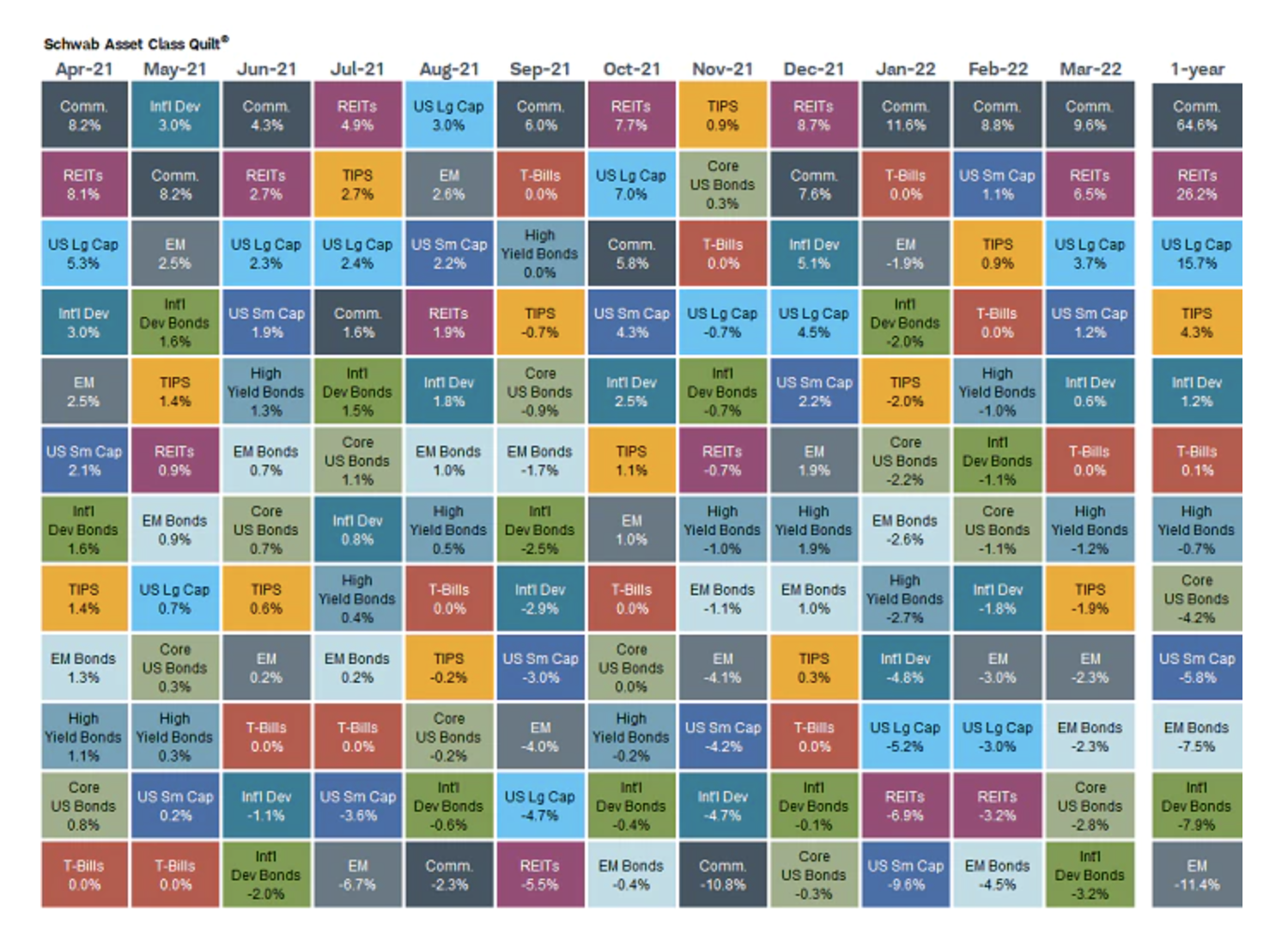

To view the benefits of diversification (across and within asset classes) with a shorter-term lens, we took liberties with regard to our traditional "asset class quilt." The first quilt below is a version of our standard quilt, but instead of the broad asset classes ranked for performance by year, we ranked them by month over the past year. As shown, Commodities have been a stellar performer over the past year; but they also spent two months at the bottom of the performance rankings. Conversely, Emerging Markets was the worst performer over the past year, but it ranked last only once (relative to Commodities' two times). Trying to time those shorter-term moves is extremely difficult.

Asset classes ranked by month

Source: Schwab Center for Financial Research with data provided by Morningstar, Inc., as of 3/31/2022. Asset class performance represented by annual total returns for the following indexes: S&P 500® Index (US Lg Cap), Russell 2000® Index (US Sm Cap), MSCI EAFE® Net of Taxes (Int’l Dev), MSCI Emerging Markets IndexSM (EM), MSCI US REIT Index (REITs), S&P GSCI® (Comm.), Bloomberg Barclays U.S. Treasury Inflation-Linked Bond Index (TIPS), Bloomberg Barclays U.S. Aggregate Bond Index (Core US Bonds), Bloomberg Barclays U.S. High Yield Bond Index (High Yield Bonds), Bloomberg Barclays Global Aggregate Ex-USD TR Index (Int’l Dev Bonds), Bloomberg Barclays Emerging Markets USD Bond TR Index (EM Bonds), FTSE U.S. 3-Month T-Bill Index (T-Bills). Past results are not an indication or guarantee of future performance. Returns assume reinvestment of dividends, interest, and capital gains. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly.

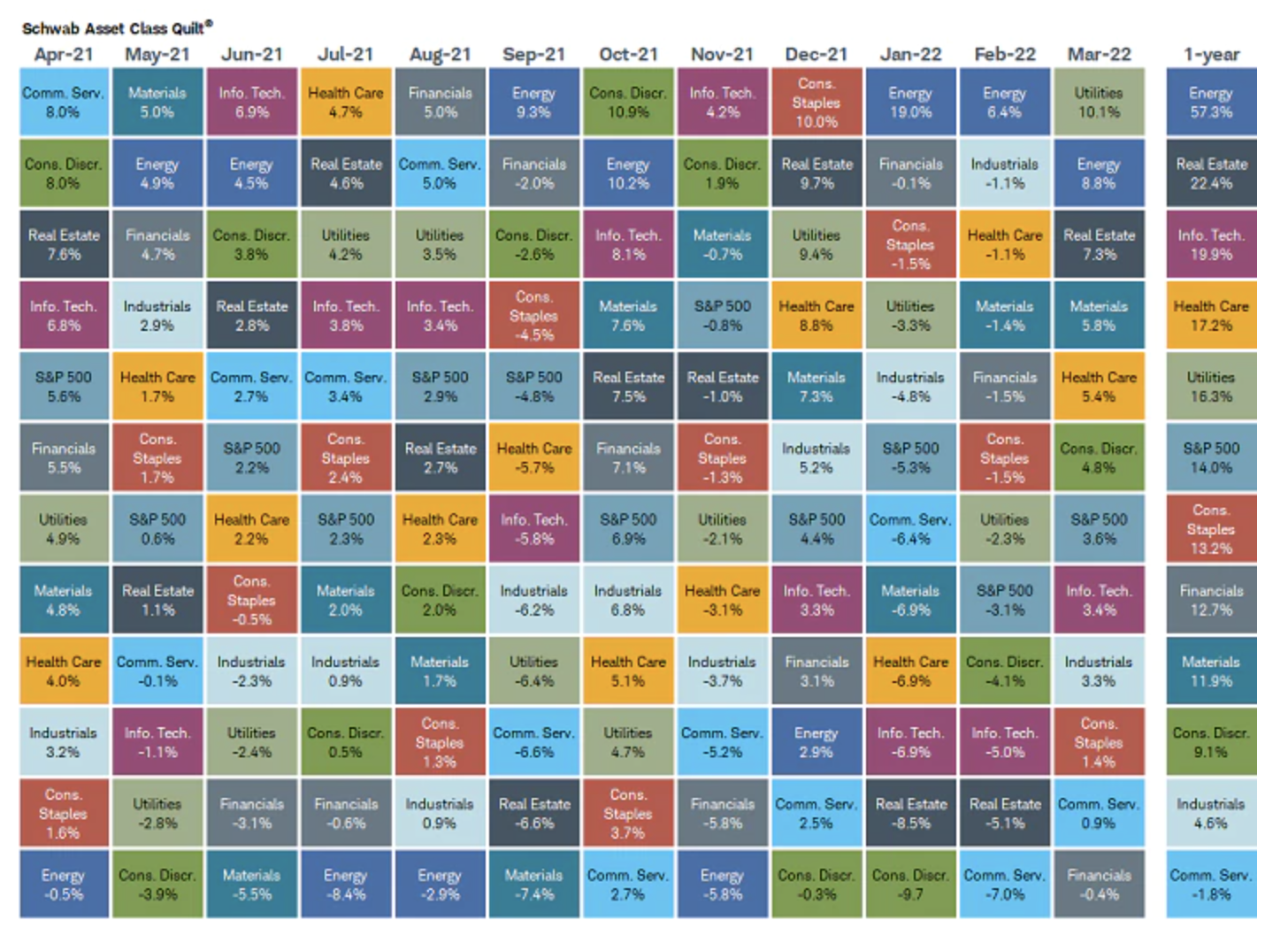

The second quilt below ranks the 11 S&P 500 sectors, also by monthly performance. Like Commodities (which of course have energy components), Energy has been the best-performing sector over the past year. However, it was actually the worst-performing sector in more months (four) than it was the best-performing sector (three). Conversely, Communication Services has been the worst performer over the past year, but it ranked last only twice (relative to Energy's four times). Like with broader asset classes, trying to time those shorter-term moves is extremely difficult in this environment.

Sectors ranked by month

Source: Charles Schwab, Bloomberg, as of 3/31/2022. Sector performance is represented by price returns of the following 11 GICS sector indices: Consumer Discretionary Sector, Consumer Staples Sector, Energy Sector, Financials Sector, Health Care Sector, Industrials Sector, Information Technology Sector, Materials Sector, Real Estate Sector, Communication Services Sector, and Utilities Sector. Returns of the broad market are represented by the S&P 500. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

For what it's worth, both Energy as a sector, and Commodities as an asset class run the risk associated with being technically "over-bought." In the event there is some sort of end to the war in Ukraine, both could come under significant pressure; but, of course, a further escalation could work in the opposite direction. Over-bought conditions may be in place; however, that's in stark contrast with the fact that they both remain "under-owned" in portfolios (in general).

In sum

Stocks have had two back-to-back downturns this year, followed by a relief rally. Leadership has flip-flopped, as has investor sentiment. Fed tightening and the war in Ukraine have been the dominant macro forces. The correction earlier this year was largely about higher inflation and rate hikes. More recently, the inversion in the yield spread between 10-year and 2-year Treasuries has heightened recession risk. However, it doesn't appear as if the stock market has appropriately priced in likely weaker economic growth to come—or the likely weaker accompanying earnings growth.

Trying to trade around these short-term swings has been difficult, and we recommend a relatively neutral stance—while using the diversification associated with strategic allocations, and periodic rebalancing to navigate the volatility. For stock pickers, we continue to recommend a factor-based approach vs. either a sector-based or style index-based approach. We believe factors such as strong free cash flow, low volatility, and rising earnings revisions will ultimately lead throughout this period of likely heightened volatility.

At Charles Schwab, we encourage everyone to take ownership of their financial life by asking questions and demanding transparency.

Our Insights & Ideas bring you information that fosters that ownership, because we believe that the best outcomes in life come from being fully engaged.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All