April tears

It was quite a month. The S&P 500 was down nearly 9% in April, its worst month since March 2020, when the pandemic wreaked havoc with stocks. It was worse for the Nasdaq, which was down more than 13%, its worst month since October 2008, when the Global Financial Crisis wreaked havoc with stocks. Even more significant pain was felt by the "Big 5" largest stocks in major indexes [Apple, Microsoft, Alphabet (Google), Amazon, and Tesla], which were collectively down nearly 20%, their worst month ever as a group. Amazon was in the crosshairs late last week, having announced that it had overbuilt during the pandemic, and is now experiencing waning demand…which may be a canary for broader consumption/inflation trends ahead.

Peeling a layer or two of the market onion back, underlying weakness has been evident for quite some time—it's just that lately, the largest-capitalization names have not been spared. Below is our crowd-favorite drawdowns table, and as shown, the average member drawdown from both year-to-date and 52-week highs is between -21% and -47%. In other words, the average member drawdown of -21% for the S&P 500 puts it in bear market territory, even though the index decline has skirted that moniker for now.

Source: Charles Schwab, Bloomberg, as of 4/29/2022. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results. Some members excluded from year-to-date return columns given additions to indices were after January 2022.

History's lessons

It's the third-worst four-month start for the S&P 500 since WWII, while it's the worst in the Nasdaq's shorter history. Looking back at historically weak starts of at least or near this magnitude, average and median returns going forward were weaker than average. Volatility has been especially pronounced for the Nasdaq 100. Bespoke Investment Group (BIG) looked at its average daily moves since its inception in 1971, and there were only three periods with loftier readings: dotcom bust era around 2000; GFC era in 2008; and debt downgrade era in 2011.

BIG also looked at the most-highly correlated years with 2022 so far. Of the 10 most similar, nine were after WWII. Again, subsequent returns were mixed-to-weak the following year. Based on the "average" patterns of the prior 10 periods, the S&P 500 tended to have further declines over the next 100 trading days, before starting to show signs of stabilization. As to whether the S&P 500 is on its way to an index-level bear market, the decline so far isn't much of a "tell" based on history. BIG compared the S&P 500's performance over the past 80 trading days to the first 80 trading days of prior post-WWII bear markets from all-time highs. In the vast majority of those prior periods, the index was down less from its all-time high than where it is now.

Halitosis

Market breadth statistics remain generally weak and "out of gear"—perhaps oversold enough to warrant a bounce, but not oversold enough to suggest the market has priced in the possible recession on everyone's mind. However, since weakness has moved up the cap spectrum, that has allowed for some breadth improvement (the hard way) for the cap-weighted indexes.

Leadership has also provided a tell in terms of the economy's trajectory. The relative outperformance of traditionally defensive segments of the market relative to more cyclical segments has been in force since last summer. At the same time, some of the most speculation-driven segments of the market are again under significant pressure. Goldman Sachs-tracked baskets, including Retail Favorites, Most-Shorted, Non-Profitable Tech-and the De-SPAC Index, are down between 40% and 70% from their highs last year.

In the market's favor could be the plunge in attitudinal measures of investor sentiment (often a contrarian indicator at extremes) and the possibility that inflation could be in the process of peaking. Earnings have also been relatively strong, in aggregate (more on that below). But risk remains high that volatility bursts will persist, especially with the Federal Reserve set to hike rates aggressively over the next several months.

GDP: emphasis on "gross"?

Those in the recession camp got some fillip last week with the release of first-quarter real gross domestic product (GDP), although the report had something for economic bulls as well. At the headline level, growth (or lack thereof) was objectively weak: real GDP contracted at a 1.4% quarter/quarter annualized rate, the first decline since the second quarter of 2020.

For what it's worth, we think the odds point more toward recession than soft landing (where the Fed can raise rates, tame inflation, and keep unemployment low.) Of the past 13 rate hiking cycles, a recession has unfolded 10 times, with soft landings only three; as such, a recession is typically the "safer bet." If the current period's unique additives—a 40-year high in inflation, growth already weak as the Fed ramps up rate hikes, the simultaneous shrinking of the Fed's nearly $9 trillion balance sheet, a pandemic that isn't over and the Russia/Ukraine war—it arguably moves the needle more toward recession. Key to the ultimate answer is likely to be the labor market, which remains an important economic support.

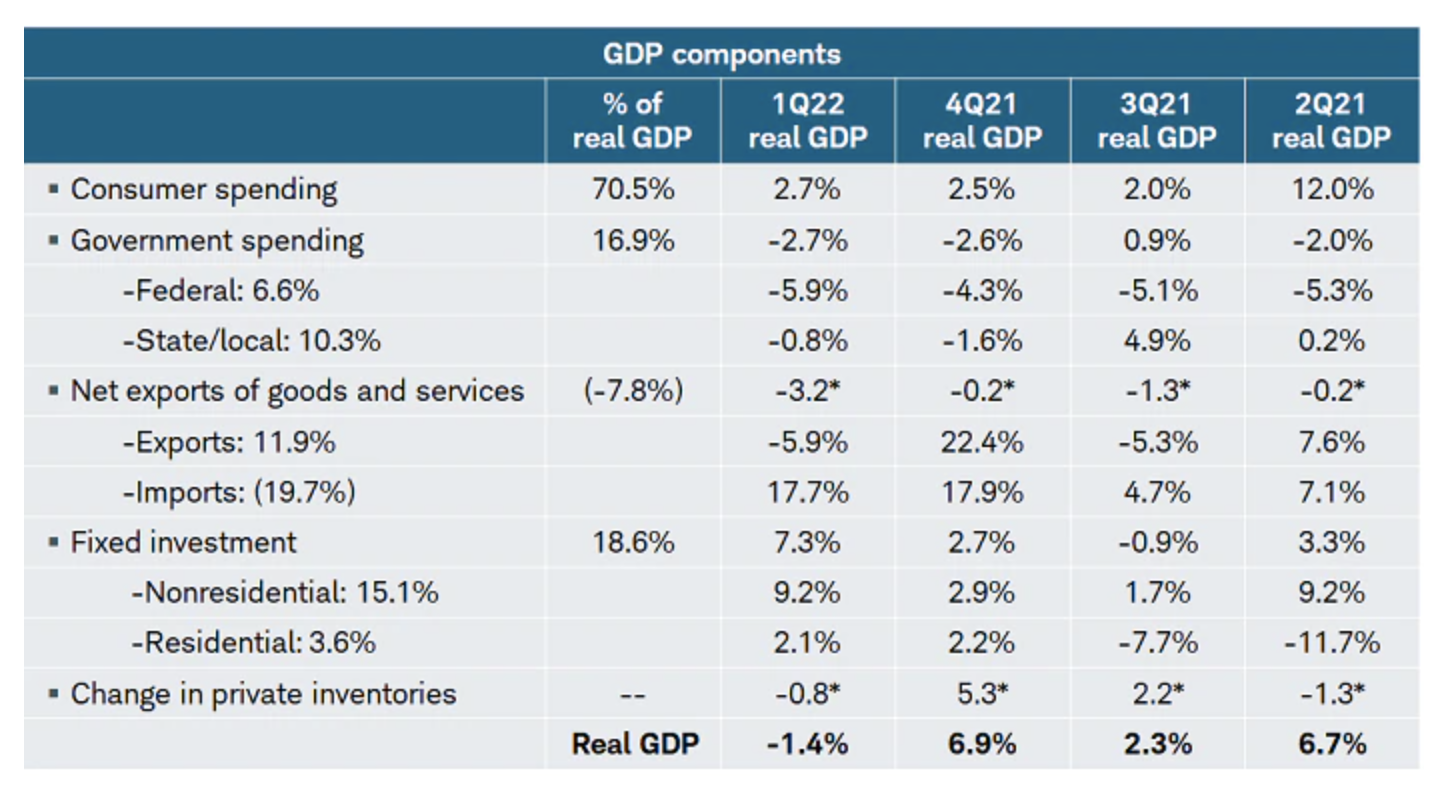

GDP details

As shown in the table below, consumer spending increased by 2.7% and business investment increased by an impressive 9.2%. Both components undoubtedly kept real GDP from falling further, given the drag from net exports and inventories, which contributed -3.2% and -0.8%, respectively, was largely responsible for pulling the headline figure into negative territory (in addition to a negative contribution from government spending).

Source: Charles Schwab, Bureau of Economic Analysis, as of 3/31/2022. *Represents contribution to percent change in real GDP. Numbers may not add up to 100% due to rounding. Real (inflation-adjusted) GDP based on annualized Q/Q % change.

Those in the soft-landing camp may write off the short-term irregularities associated with the trade balance and inventory data, instead shifting focus to the relative strength of the consumer. The surge in imports was indeed a confirmation that shipping congestions continued to ease throughout the quarter, and though inventories have climbed in level terms, the rate slowed considerably (it was never expected to match the increase in the fourth quarter of 2021).

The economically bearish take is that negative inventory contributions may persist for longer than expected. Inventories as a component of GDP are calculated as the change in the growth rate as opposed to the change in the stock; if businesses are unable to boost stockpiles at the same rate as in the prior quarter, there will be a net negative effect. If that persists alongside a slowdown in consumption, there is likely further downside to headline growth.

A balanced view of growth in the first quarter is that consumption's pace has slowed, business investment remains incredibly strong (a plus for the supply side of the economy), and the fiscal drag persists. What helped keep the economy afloat in the depths of the pandemic was a double-barreled boost from both fiscal and monetary policy; yet the math is such that we now have a double-barreled tightening from the reversal in (or now lack of) stimulus. In conjunction with the surge in inflation, that will put downward pressure on growth, incomes, and spending.

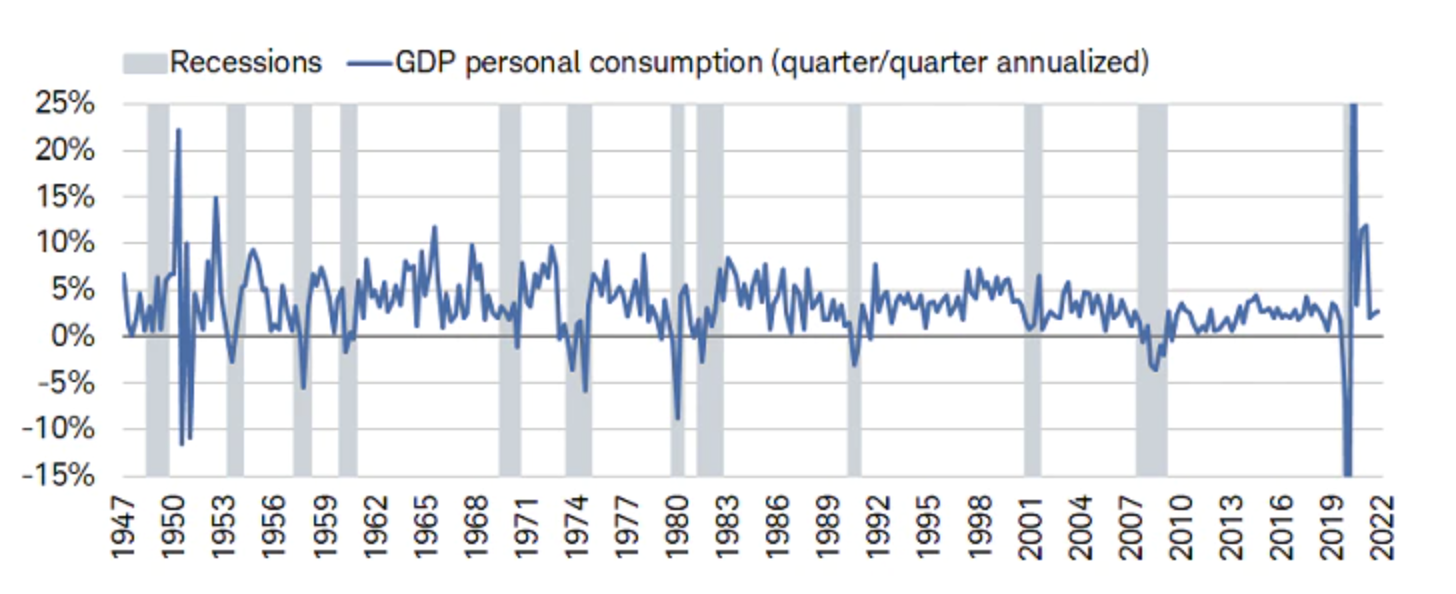

A note on the "strength" of the consumer

The 2.7% increase in first-quarter consumer spending is not to be discounted, as consumption helped keep growth from diving lower. Worth noting, however, is that consumer spending does not need to turn negative for the broader economy to weaken or even enter into a recession.

As shown below, consumer spending never contracted during the 2001 recession, contracted for only one quarter in the 1981-1982 recession, and was even positive for one quarter in 2008 (as the financial crisis unfolded). Acute observers will note that the narrative of the strong consumer is not always the elixir for the economy; broader macro forces can at times be powerful enough to supersede spending.

Consumption's boomerang

Source: Charles Schwab, Bureau of Economic Analysis, as of 3/31/2022. Y-axis truncated at +25% and -15%.

Also worth emphasizing is both the trend in spending and the reason it moved up in the first quarter. Real consumption improved in March relative to February, assuaging some fears that the second quarter started on weak footing. However, March's 0.2% gain was down considerably from the 1.5% gain in January. Not only that, but the savings rate fell to 6.2% in March (the lowest since 2013), a 2.2% drop from the end of 2021. That indicates that consumers dipped into their savings to maintain their spending throughout the quarter, which isn't surprising given the sharp increase in inflation.

Should that trend continue, however, there may be less slack for consumption to continue to boost growth; and while business investment remains strong right now, the future is murkier with an aggressive Fed, supply chain disruptions failing to dissipate, and margins coming under pressure. Regardless of whether recent economic weakness is the marker of a recession on the horizon, investors should be keenly aware that growth is slowing. Not only have the effects of the pandemic relief/stimulus, post-vaccine reopening, and pro-cyclical inflationary boom worn off, they have turned into headwinds.

Beat it

As noted, first quarter 2022 earnings season so far has provided decent news, at least in the aggregate. Of the 279 companies in the S&P 500 that have reported earnings per share (EPS), more than 80% have beaten consensus estimates—compared to a long-term (since 1994) average of 66%, but a prior four-quarter average of 83%. In aggregate, companies have reported EPS 6.7% above estimates—compared to a long-term average of 4.1%, but a prior four-quarter average of more than 13%.

On the negative side, there have been 75 negative EPS pre-announcements issued by S&P 500 companies compared to 27 positive, which puts the negative/positive ratio at 2.8 (significantly higher than normal). On a more positive note, the window for stock buybacks has reopened, which could provide a boost to EPS.

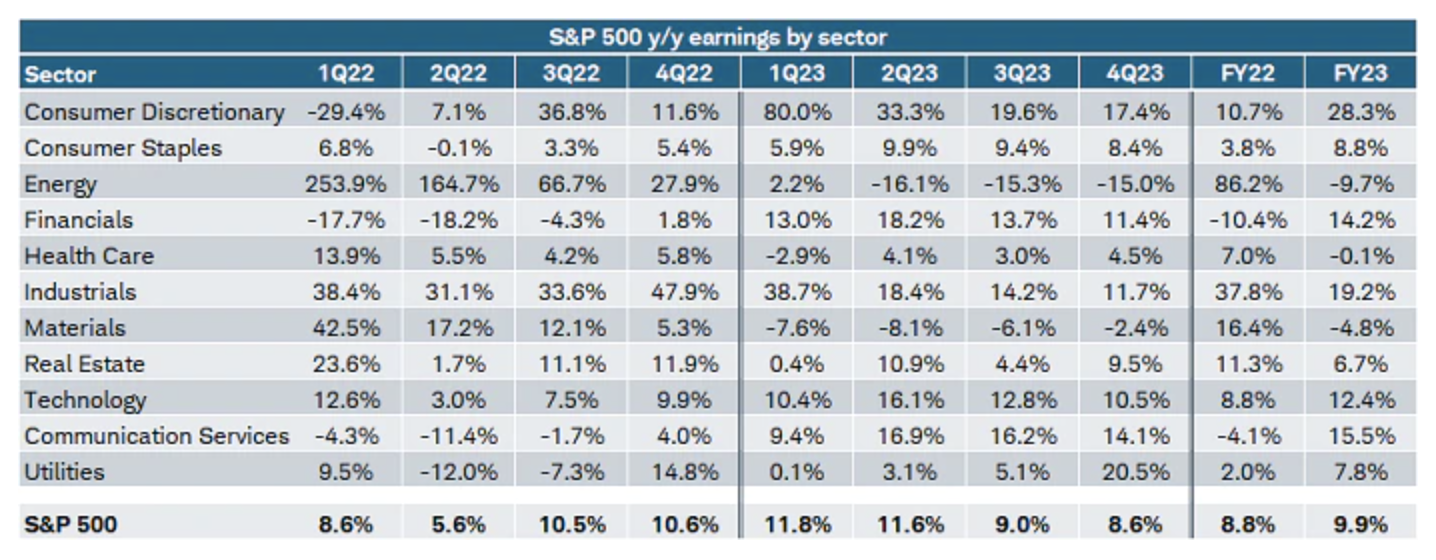

As shown below, the "blended" growth rate (combining already-reported earnings with consensus expectations for those not yet reported) for the S&P 500 is now more than 8%, with Energy leading the sector pack and Financials bringing up the rear. From there, earnings are expected to slow to about 6% in the second quarter before rebounding in the second half. We can say for certain that these growth rates will not prove to be accurate—but whether the bar remains set too low will largely be dependent on the trajectory of the economy from here (obviously).

Source: Charles Schwab, I/B/E/S data from Refinitiv, as of 5/2/2022. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

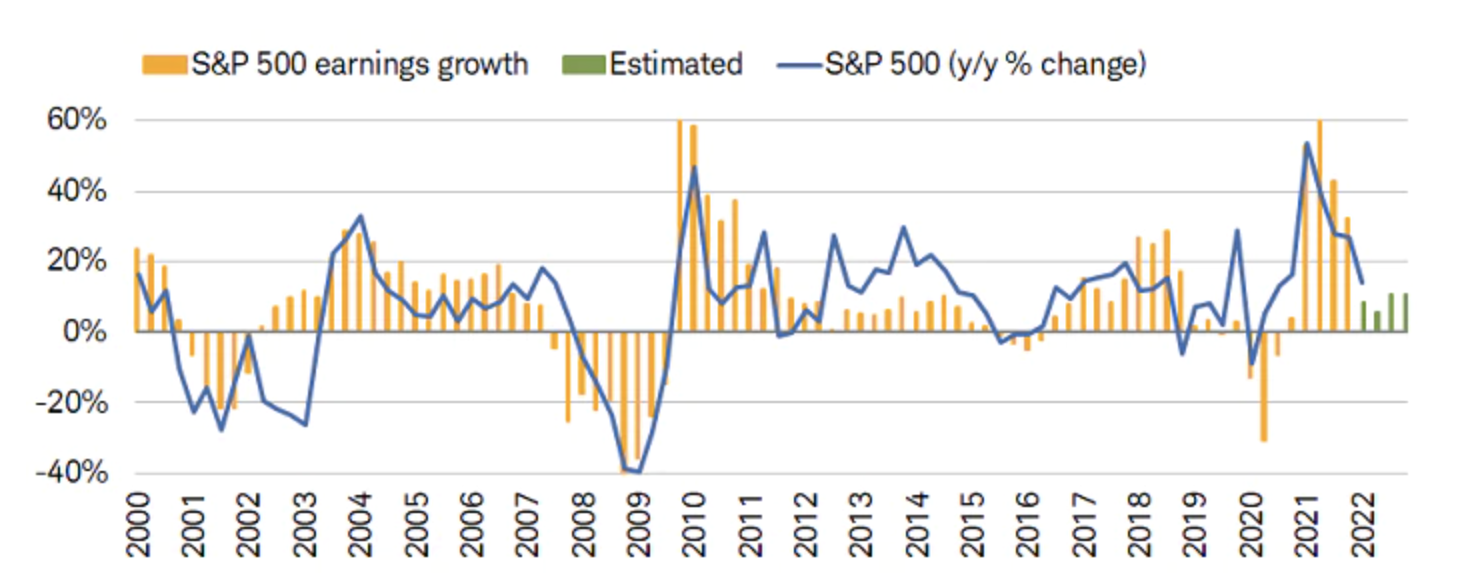

Thanks in large part to high labor costs, profit margins have decelerated as well, though not yet to a significant degree (we expect more to come next quarter). In keeping with the deceleration in earnings growth underway since last year's peak, the S&P 500's year/year change has decelerated accordingly, as shown below (the green bars represent quarterly consensus estimates).

S&P change mirrors EPS growth rate

Source: Charles Schwab, I/B/E/S data from Refinitiv, as of 5/2/2022. Y-axis truncated at +60% and -40%. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data. Past performance is no guarantee of future results.

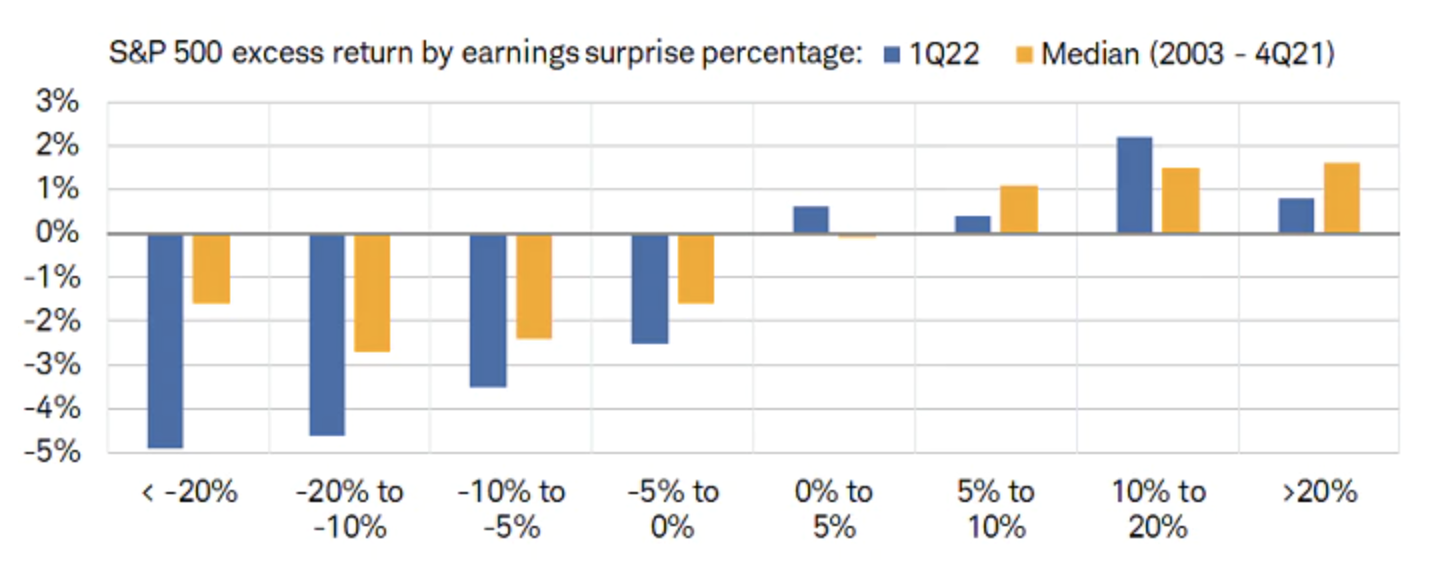

Volatility tied to earnings releases has been significant. As shown below, on earnings report days, stocks disappointing the most (at least a 20% miss relative to expectations) have been hammered relative to the 2003-2021 median. At the same time, stocks beating expectations by at least 20% have had weaker performance relative to the 2003-2021 median.

Misses getting punished disproportionately

Source: Charles Schwab, 22V Research, as of 4/29/2022. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

In sum

It's been a mixed-to-weaker bag in terms of macro drivers and we expect significant bouts of volatility to persist. Based on the initial report, the economy contracted in the first quarter, but consumer spending remained relatively healthy. Although inflation may have peaked, it's unlikely to decelerate quickly, putting increasing pressure on the consumer looking ahead. Investor sentiment, as measured by surveys, has turned pessimistic, which could provide some support for stocks; however, behavioral measures of sentiment do not yet show a "washout," or full-scale capitulation.

Last year was a story of pro-cyclical (or demand-pull) inflation, while this year it's turned into a story of counter-cyclical (or cost-push) inflation. The pressure associated with the latter should be somewhat proportional to the power of the former, which suggests even if some measures of inflation have peaked, the negative economic consequences are likely not yet in the rearview mirror.

This is not a time for investors to take on risk outside the parameters of their strategic asset allocations. It is a time for investors to employ traditional disciplines around diversification (across and within asset classes), to focus on quality in terms of stocks' fundamentals, and to stay in gear via periodic rebalancing. In the case of rebalancing, it's one of the investment world's greatest disciplines, as it forces investors to adhere to a derivative of the adage, "buy low, sell high," which is: add low and trim high.

© Charles Schwab

Read more commentaries by Charles Schwab