2022 Mid-Year Corporate Credit Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAfter the steep drop in prices during the first half of this year, yields on many corporate bond investments are at or near 12-year highs. While that is attractive from an income perspective, we still suggest a maintaining a defensive approach, as risks are rising.

The first half of 2022 has been one to forget, with many corporate bond investments down more than 10% so far. The drop in prices was driven by a combination of higher Treasury yields and rising credit spreads, as investors demanded additional yield to compensate for the risk of slower economic growth and the potential for corporate profits to decline.

There was nowhere to hide, as even short-term bonds and those with floating coupon rates suffered declines. After the steep drop in prices, yields on many corporate bond investments are at or near their 12-year highs, but we still suggest a maintaining a defensive approach, as risks are rising.

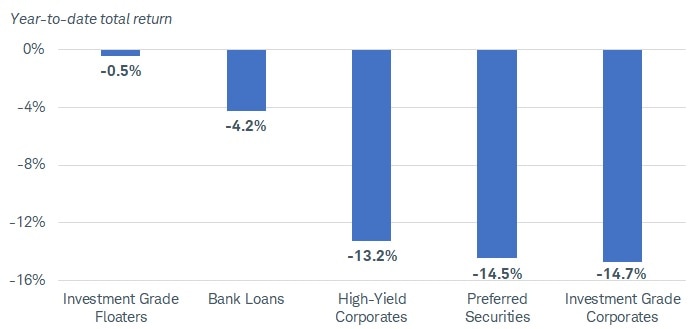

Corporate bond investments suffered losses in the first half of the year

Source: Bloomberg. Total returns from 12/31/2021 through 6/22/2022.

Indexes represented are the Bloomberg U.S. Floating Rate Notes Index (Investment Grade Floaters), S&P/LSTA Leveraged Loan Index (Bank Loans), Bloomberg U.S. Corporate High-Yield Bond Index (High-Yield Corporates), ICE BofA Fixed Rate Preferred Securities Index (Preferred Securities), and Bloomberg U.S. Corporate Bond Index (Investment Grade Corporates). Total returns assume reinvestment of interest and capital gains. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no indication of future results.

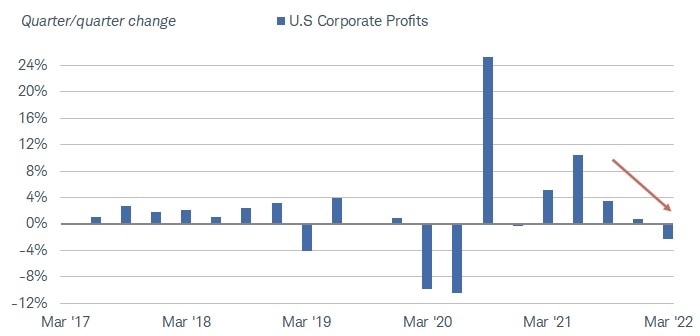

Corporate profits are one concern, due to the combination of slowing consumer demand and rising input costs for companies. High inflation could take a bite out of the consumer's ability to spend, so top-line revenues may slow. Rising labor costs may also eat away at profit margins. According to Bureau of Economic Analysis data, which includes public and private companies of all sizes, corporate profits actually declined in the first quarter of 2022 after decelerating the two previous quarters.

Corporate profits declined in the first quarter

Source: Bloomberg, using quarterly data as of 1Q 2022.

US Corporate Profits With IVA and CCA Total SAAR (CPFTTOT Index).

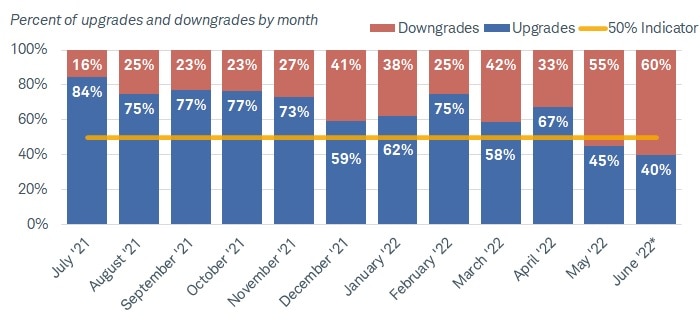

The rating agencies have been taking notice, and the number of downgrades has begun to pick up for high-yield bond issuers. For most of 2021, we viewed corporate fundamentals as strong, with many companies taking advantage of record-low borrowing costs to lower their interest expenses and to extend their bond maturities, all while corporate profits were growing. In 2022, borrowing costs have risen sharply, the corporate profit outlook is poor, and demand may slow. There was a noticeable uptick in downgrade activity of high-yield-rated issuers over the last two months, with the number of downgrades outpacing the number of upgrades. For investment-grade issuers, the number of downgrades still remains relatively low.

High-yield downgrades have outnumbered upgrades over the last two months

Source: Bloomberg, with data from Moody's.

Monthly upgrade/downgrade actions of high-yield rated companies from July 2021 through June 2022. June 2022 data through June 22, 2022.

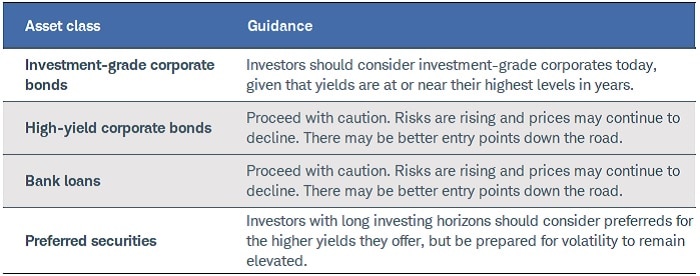

Here's a quick summary of our views, and below we provide more details about the various parts of the bond market, highlighting some areas of opportunity and some potential pitfalls.

Source: Schwab Center for Financial Research

Investment-grade corporate bonds

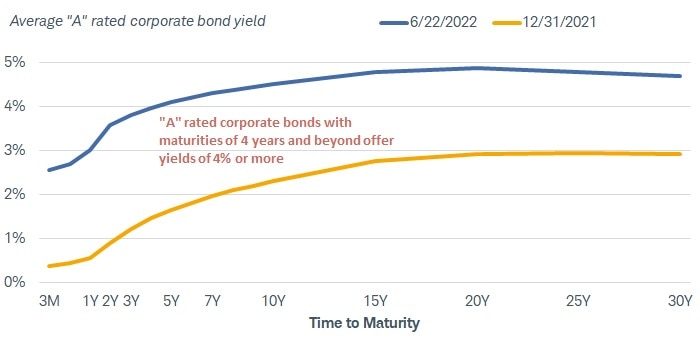

Investment-grade corporate bonds appear attractive today, with yields at their highest levels in years. The average yield on intermediate-term investment grade bonds1 is more than 4.5%. For investors who want to stay in higher-rated bonds, even "A" rated bonds can offer yields above 4% without taking much interest-rate risk.

For years, "TINA" was an investment theme. It stands for "There Is No Alternative" to stocks, as bond yields are so low. We no longer believe that's the case, and there's finally "income" in the fixed income markets, including higher-rated investments like investment-grade corporates.

There are risks of course—corporations all across the credit rating spectrum are at risk if economic growth continues to slow. But investment grade rated issuers carry investment grade ratings for a reason. They tend to be larger companies with strong balance sheets and more stable cash flows. Those factors should be helpful if economic growth declines. While that won't prevent prices from falling if the stock market continues to decline, the potential declines would likely be a lot less than the potential declines of high-yield bonds.

Intermediate-term "A" rated corporate bonds have more than doubled this year

Source: Bloomberg, as of 6/22/2022.

USD US Corporate A+, A, A- BVAL Yield Curve (BVSC0074 Index). Indexes are unmanaged, do not incur management fees, costs and expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

Investor takeaway: Investment grade corporate bond yields appear attractive today given the recent rise in yields. To consider investment options, you can search using the ETF Screener or Mutual Fund Screener, or explore funds on the ETF Select List or Mutual Fund Select List. You can also consider a separately managed account.

High-yield corporate bonds

High-yield corporate bond yields may appear attractive at first glance, but we'd caution that additional price declines seem likely. Although we believe the worst of the bond market rout may be behind us, that's not necessarily the case with high-yield bonds.

High-yield bonds offer average yields2 of roughly 8.5%, more than double the yields they offered at the end of 2021.The rise in yields was driven by a combination of rising Treasury yields and rising credit spreads. (Corporate bond yields are generally comprised of a Treasury yield plus a "spread" meant to compensate investors for the risk of investing in riskier bonds.)

We believe Treasury yields may be near their peak, but credit spreads may keep rising. Despite rising from less than 3% at the end of 2021 to more than 5% today, spreads are still below many of their other peaks over the last 12 years. Because credit spreads are an indication of risk—when risks are high, investors demand more compensation—they may continue to drift higher in the near term.

High-yield bond spreads are just barely above the 10-year average, and still below previous peaks

Source: Bloomberg, using daily data as of 6/22/2022.

Bloomberg U.S. Corporate High-Yield Bond Index (LF98TRUU Index). Option-adjusted spreads are quoted as a fixed spread, or differential, over U.S. Treasury issues. OAS is a method used in calculating the relative value of a fixed income security containing an embedded option, such as a borrower's option to prepay a loan. Past performance is no guarantee of future results.

The risks mentioned above are most acute with high-yield-bond issuers. They tend to have more volatile cash flows, weaker balance sheets, and more leverage (debt relative to earnings) than investment-grade issuers. Given the rising borrowing costs, which can eat into already thin profit margins, and a challenging economic outlook, spreads should continue to rise from here.

Compared to other instances of rising spread, the level of spreads is still low. At just 5.2%, the average OAS of the Bloomberg U.S. Corporate High-Yield Bond Index is still below the 5.4% peak at the end of last Fed rate-hike cycle in 2018, and well below the other peaks over the last 12 years. If spreads continue to rise, high-yield bonds will likely appear more attractive, but until then we'd exercise some caution, given the risk that higher spreads would pull high-yield bond prices even lower.

Investor takeaway: Additional price declines and heightened volatility seem likely. Although yields of 8% or more may appear attractive, we suggest a cautious approach and believe there may be better entry points down the road

Bank loans

Bank loans are a niche part of the bond market—they are secured by a pledge of the issuer's assets and have floating coupon rates. They're usually only available to large institutional investors, so for most individual investors the only way to access the market is through a mutual fund or ETF.

First, investors shouldn't consider bank loans "safe" just because they are secured by a pledge of assets. Even with that pledge, they carry sub-investment-grade, or "junk," ratings. Most of our concerns for the high-yield bond market are concerns for bank loans, as well, as bank loan issuers also tend to have high leverage and volatile cash flows.

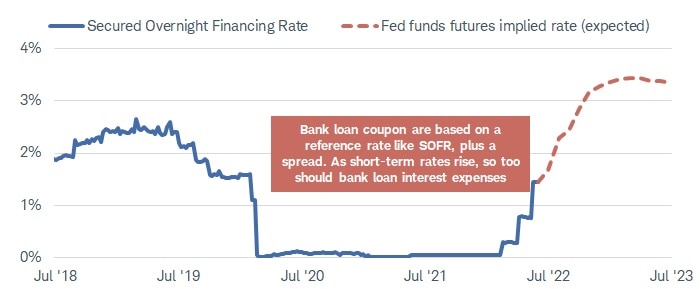

Second, bank loans' floating coupon rates can be both a blessing and a curse. The blessing for investors is that their income payments tend to rise alongside the rise in the federal funds rate. Bank loan coupon rates are based on a short-term reference rate plus a spread (just like the high-yield spread meant to compensate for the greater risks.) The reference rate is usually a short-term benchmark rate that has a strong relationship with the fed funds rate; many bank loans are referenced to the Secured Overnight Financing Rate (SOFR) or the 3-Month London Interbank Offered Rate (LIBOR).

The curse for borrowers is that they may see their interest expenses rise very quickly. In 2021, for example, the average coupon rate for the bank loan universe was roughly 3.5%, assuming a short-term reference rate of just above zero and average spreads of 3.25% to 3.5%. If the federal funds rate does in fact rise to 3.5% or above, borrowing costs for bank loan issuers will rise sharply. Given the rising input and labor costs already burdening many corporations, rising interest expense is one more factor that can eat into corporate profit margins. Like high-yield bonds, bank loan prices may fall modestly lower from here.

Bank loan income payments may keep rising, but that also means rising interest expense for the issuer

Source: Bloomberg.

United States SOFR Secured Overnight Financing Rate (SOFRRRATE Index) using weekly data through 6/21/2022, and Fed funds futures implied rate using monthly expectations through July 2023. For illustrative purposes only. Futures and futures options trading involves substantial risk and is not suitable for all investors. Please read the Risk Disclosure Statement for Futures and Options prior to trading futures products. Futures accounts are not protected by SIPC.

Investor takeaway: Bank loans are high risk investments even though they are secured by a pledge of the issuer's assets. Price may continue to fall if the economic outlook deteriorates even more. Like high-yield bonds, there may be better entry points down the road.

Preferred securities

Preferred securities appear relatively attractive, with a few caveats.

Given their hybrid nature, as they have characteristics of both stocks and bonds, they are sensitive to movements in both the stock market and the bond market. While we believe Treasury yields may be near their peak, preferred prices may still decline if common stock prices continue to fall. Given today's low starting point, price declines may be relatively limited, however.

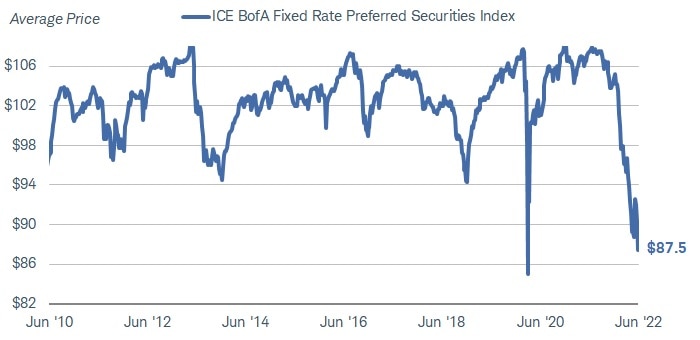

Preferred prices have rarely been lower

Source: Bloomberg, using weekly data as of 6/22/2022.

Note that average price of the preferred index is rebased to $100, despite many of its underlying holdings having par values of $25. As a result, the price fluctuations of $25 par value preferreds wouldn't likely be as large in dollar terms, but would be similar in percentage terms. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

Banks and other financial institutions tend to be the largest issuers of preferreds. In the U.S., the large banks are generally well-capitalized, given tight regulations in the years following the 2008 financial crisis. Bank earnings may decline, given slower economic growth and a flattening yield curve, but they should still be well-positioned to remain current on their preferred coupon payments. Concerns about dividend suspension may begin to make headlines if recession fears continue to grow, but we view that as more of a risk for non-rated or very low-rated preferred securities. For investment-grade rated preferreds, or even those rated in the "BB" range, we believe the risk of preferred security dividend suspension is low.

Because preferred securities have long maturities or no maturities at all, they should always be considered long-term investments. Although preferreds may be "called," or redeemed, by the issuer after a certain period of time has passed, it's unlikely that many recently issued preferred securities will get called anytime soon. With yields up so much this year, it doesn't make much economic sense for an issuer to retire them early.

It's hard to ignore the nearly 6.5% yields that investment-grade preferreds offer, but investors should be ready to ride out some volatility to earn those high yields.

Investor takeaway: Preferred securities appear attractive for investors who have a long investing horizon and are willing to ride out the ups and downs. While banks are well capitalized, any risk-off sentiment could lead to modest price declines.

There are a number of ways to learn more about preferred securities. Schwab clients can use the Preferred Shares Screener, can search for funds using the ETF Screener or Mutual Fund Screener, or explore funds on the ETF Select List or Mutual Fund Select List under the Morningstar category of "Preferred Stock."

1 Based on the Bloomberg U.S. Corporate Intermediate Bond Index (LD06TRUU Index). The average yield-to-worst was 4.6% on 6/22/2022.

2 Based on the average yield-to-worst of the Bloomberg U.S. Corporate High-Yield Bond Index (LF98TRUU Index), as of 6/22/2022.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All