Equity markets plunged to start the week based on increased FOMC pressure to raise rates to combat inflation. As markets tumble from recent highs seen last week, the at-the-money monthly $VIX option contract for September shows significantly more premium on the call side compared to the put side, indicating a potential bullish skew favoring an increase in volatility. One way to combat uncertainty in the market is to implement a hedge position in your equity portfolio. Today, I would like to discuss three different methods that can be utilized to hedge a large cap stock portfolio and provide context to the information necessary to place a proper hedge.

For the purposes of this discussion, let’s assume we are looking to hedge a $500,000 portfolio of large cap stocks using Index products that track the S&P 500. The E Mini S&P 500 or ES futures contract, SPY ETF, and $SPX options are three common products used to hedge a portfolio of large cap stocks.

We will also discuss the importance of beta weighting your portfolio. Beta is a measurement of volatility of an individual stock in comparison to the market. The level of the beta indicates the degree of correlation between a security and a market benchmark, in this example the S&P 500. A beta greater than 1 means the stock is more volatile than the overall market, while a beta less than 1 indicates that the security is more stable than the market. To find your portfolio’s beta you will need to multiply the percentage of the stock in your portfolio by its Beta, then add up the results of each position.

Another concept you will need to understand when hedging a portfolio is Delta. Delta measures how much an option's price is expected to change per $1 change in the price of the underlying security or index. For example, a Delta of 0.40 means that the option's price will theoretically move $0.40 for every $1 move in the price of the underlying stock or index.

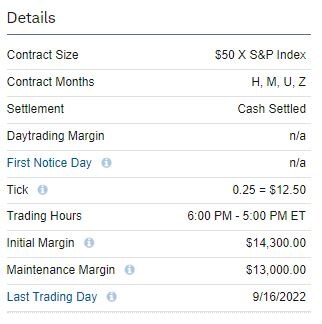

In order to hedge a portfolio using the E Mini S&P 500 futures contract a client will need to first have a margin account that has been approved to trade futures. For the purposes of this discussion, we will assume a $500,000 portfolio of large cap stocks, which has a beta of 1. At the time this article was written, the E Mini S&P 500 September 2022 contract (ESU22) was trading at 4175.00 which computed to a notional value of $208,750 (4175.00x$50). In order to calculate the number of contracts needed to place the hedge we will divide the total portfolio value by the notional value of one ESU22 contract.

$500,000/208,750=2.40 ESU22 futures

Three ESU22 contracts would come very close to fully hedging this $500,000 portfolio of large cap stocks. The current initial margin requirement for an ESU22 contract is $14,300. You are not able to trade fractional contracts in the futures market so in order to hedge a $500,000 portfolio of large cap stocks utilizing E Mini S&P 500 futures contracts we will slightly under hedge with two contracts at an initial requirement of $28,600. Two contracts would protect $417,500 of the $500,000 portfolio.

2 x $208,750= $417,500

Exchange traded funds (ETF) on broad based indices also provide hedging opportunities. We can create a hedge strategy for a $500,000 portfolio with a beta on 1 using SPY the Spdr S&P 500 ETF. To place a short hedge using SPY you will need a margin account. As of this writing, SPY was trading at $416.00 per share. To fully hedge our $500,000 portfolio, we will need to sell short 1202 shares of SPY at a price of $416 per share. The standard margin requirement of a short position of this nature is 30%, which would leave the total requirement for this hedge position at $150,009. This is a straightforward strategy that is easy to conceptualize but fairly expensive.

The third example that I would like to discuss is a hedge strategy using options on the S&P 500 index, ticker symbol $SPX. Using options as a hedge strategy brings in the added element of time. We will also have to factor in Delta to the equation to create a complete hedge on a $500,000 portfolio of large cap stocks. For the purposes of this discussion, I will use an at-the-money option 6 months from expiration. The SPXW 01/20/2023 4160.00 P was trading at $225 per contract at the time this was written with a Delta of .45. Factoring the $416,000 underlying value of the contract and the .45 delta, the hedge value of SPXW 01/20/2023 4160.00 P is $187,200 per contract.

$500,000/187,200= 2.67 SPXW 01/20/2023 4160.00 P

Three SPX SPXW 01/20/2023 4160.00 P contracts would slightly over hedge a $500,000 portfolio and would cost $67,500 at the time this was written. When using Index options to hedge it is very important to factor in strike and expiration selection to meet the tailored needs of your portfolio.

As you can see through these three examples, futures can provide excellent hedging opportunities. The added leverage with lower cash outlays can allow you to protect a $500,000 portfolio with an initial margin requirement of around 7% of the underlying value. However, this strategy does not go without risk. If the market rises, you may need to deposit additional funds in your futures account in order to meet a margin call. A poorly timed hedge can result in missed opportunities and can produce losses.

With the introduction of the CME’s micro contract traders can use futures to hedge portfolios of nearly any size. Using broad based index ETF’s, one is required to meet the 30% margin requirement, which can be very expensive. When trading index-based options a trader is forced to select the proper time frame as well as the proper strike price. Other benefits of hedging through futures contracts include longer trading times, with futures trading 23-hour trading days. Futures are also taxed as a 1256 contract, with 60% taxed as long-term gains and 40% taxed as short-term gains.

There are many ways to hedge your portfolio, and futures contracts may provide a trader yet another way to mitigate risk.

Futures trading carries a high level of risk and is not suitable for all investors. Certain requirements must be met to trade futures. Please read the Risk Disclosure Statement for Futures and Options on our website for additional information.

Technicals

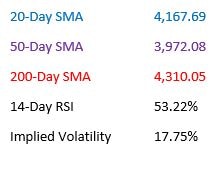

Looking at the daily chart for the E Mini S&P 500 September 2022 (ESU22) contract we can see the substantial selling pressure over the past three sessions. The contract was not able to hold a level above the 200-Day Simple Moving Average and broke below the 50-Day SMA level during trading yesterday. The 20-Day SMA point could be the next support for this contract.

Trading Central’s Daily Technical Analysis has support levels found at 4155.0 and 4126.0 with resistance levels found at 4234.0 and 4259.0.

The CFTC Commitment of Traders report released on August 16th shows asset managers increased their position by +23,615 contracts and a decreased their short position by -56,556 contracts. Asset managers are net long 376,090 contracts.

The 14-Day Relative Strength Index at 53.22% indicates the contract is not overbought or oversold at this time.

Contract Specifications

E Mini S&P 500 September 2022 (ESU22)

Henry Hub Natural Gas July 2022 (NGN22)

Trading Calendar

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice.

Hedging and protective strategies generally involve additional costs and do not assure a profit or guarantee against trading losses.

Futures and futures options trading involves substantial risk and is not suitable for all investors. Please read the Risk Disclosure for Futures and Options prior to trading futures products. Futures accounts are not protected by SIPC. Futures and futures options trading services provided by Charles Schwab Futures and Forex LLC. Trading privileges subject to review and approval. Not all clients will qualify.

Charles Schwab Futures and Forex LLC (NFA Member) and Charles Schwab & Co., Inc. (Member FINRA/SIPC) are separate but affiliated companies and subsidiaries of The Charles Schwab Corporation.

Virtual Currency Derivatives trading involves unique and potentially significant risks. Please read NFA Investor Advisory – Futures on Virtual Currencies Including Bitcoin and CFTC Customer Advisory: Understand the Risk of Virtual Currency Trading.

Charles Schwab & Co., Inc., 211 Main Street, San Francisco, CA 94105

0822-2WOD

© Charles Schwab

Read more commentaries by Charles Schwab