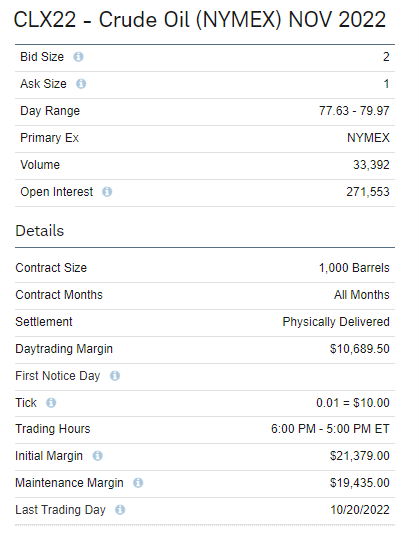

Oil has been routing since summer after reaching historic highs of over $130 per barrel, but we may see some relief soon as near-term events may trigger a rally. Light Sweet Crude November Futures, CLX22, hit an eight-month low on Friday as it fell to $78 per barrel a 6% drop, closing at $78.74.

Since Spring, the Biden Administration has been authorizing a release of one million barrels per day from the Strategic Petroleum Reserve to reduce the cost of gasoline, the effort has been a success. According to the U.S. Energy Information Administration (EIA), the cost of gasoline has dropped over $1 since hitting a historic national average high of $5.032 per gallon in June. According to the EIA the national average for August was $4.087 per gallon and currently at $3.714 per gallon according to AAA.com. The current program to release from the strategic reserve ends in October and not expected to be renewed.

Conversely, the U.S. Government through the Department of Energy plans re-stock the strategic reserves through market action and oil royalties as defined in Part 626 Revisions Notice of Proposed Rulemaking republication. These deliveries are not expected to happen until after fiscal year 2023.

The European Union adopted sanctions against Russian seaborne imports of crude oil in June to start December 5th, then to ban petroleum product imports starting February 5th, 2023. This effort coupled with the ending of U.S. strategic reserve releases, may create a supply shortage later this year.

It is expected that oil demand will rise by 2.1 million barrels per day through the end of the year according to the market oil report released in August. This will put eyes on the Organization of the Petroleum Exporting Countries (OPEC) when they meet on October 5th. During their last meeting, OPEC decided to cut output, of which it fell short by 3.58 million barrels per day in August.