Inflation Is Up, so Why Are TIPS Returns Down?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTreasury Inflation-Protected Securities can be a buffer against long-term inflation, but it's possible for TIPS price declines to outpace principal adjustment in the short term.

Investors holding Treasury Inflation-Protected Securities, or TIPS, as a hedge against inflation may be confused by their performance this year: TIPS prices have declined sharply despite the surge in inflation. Many may wonder: Is this normal?

It's not "normal" for TIPS to fall so much, but it's common for TIPS returns and the rate of inflation to diverge over short periods of time. TIPS can help protect investors against inflation over the long term, but they aren't a hedge against inflation in the short run, because price changes may more than offset the principal adjustment over shorter periods of time. While this year's performance may have investors worried about the outlook for TIPS, we believe the rise in yields and the decline in breakeven rates makes them more attractive today than they have been recently.

Investing in TIPS isn't always straightforward. They have many unique characteristics that can make the investing experience a bit confusing. Here are answers to some of the most frequently asked questions about the TIPS market:

1. What are TIPS?

TIPS are a type of Treasury security whose principal value is indexed to inflation. When inflation rises, the TIPS' principal value is adjusted up. If there's deflation, then the principal value is adjusted lower. Like traditional Treasuries, TIPS are backed by the full faith and credit of the U.S. government.

The coupon payments are based on a percent of the adjusted principal, so investors can benefit from higher income payments when inflation is rising as well.

At maturity, however, a TIPS investor would receive either the adjusted higher principal or the original principal value. In other words, TIPS never pay back less than the initial principal value at maturity.

Principal adjustment and coupon payments for a hypothetical five-year TIPS

Source: Schwab Center for Financial Research.

The initial hypothetical TIPS principal value is $1,000. For simplicity, this examples shows an annual inflation adjustment for the principal value, although in reality the adjustment occurs twice a year. The annual coupon payment equals the fixed coupon rate multiplied by the adjusted principal value. Example is hypothetical, for illustrative purposes only.

2. Why have TIPS performed so poorly when inflation is so high?

TIPS prices have fallen more than the principal has adjusted higher, resulting in negative total returns for the year. TIPS are still bonds, meaning their prices and yields move in opposite directions. Like most fixed income investments this year, TIPS yields have surged, pulling their prices lower.

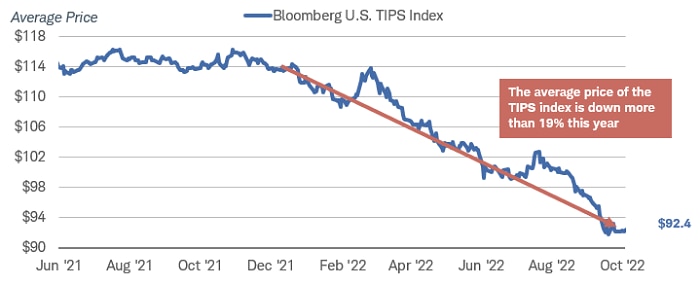

The chart below highlights that the average price of the TIPS index has dropped by more than 19% this year. The plunge in price is a key reason why TIPS don't necessarily protect against inflation over the short run, as price movements can be larger than those principal adjustments.

TIPS prices have plunged this year

Source: Bloomberg, using daily data as of 10/18/2022.

Past performance is no guarantee of future results.

Keep in mind that TIPS prices in the secondary market do not include the adjusted principal value. When buying or selling TIPS in the secondary market, for example, the transaction amount may be different than what the price would suggest because of the adjusted principal value.

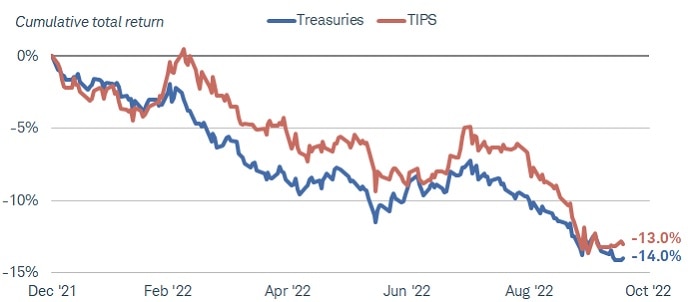

3. How have TIPS performed relative to traditional Treasuries this year?

The Bloomberg U.S. TIPS Index is down 13% this year through October 18th, while the Bloomberg U.S. Treasury Index is down a bit more, with a negative 14% total return over the same period. So even though the Consumer Price Index (CPI) is up 8.2% in the 12 months ending September 31, 2022, the price decline more than offset that positive principal adjustment.

TIPS have delivered deeply negative total returns this year, just like traditional Treasuries

Source: Bloomberg.

Total returns from 12/31/2021 through 10/18/2022. Bloomberg U.S. Treasury Index (LUATTUU Index) and the Bloomberg U.S. Treasury Inflation Protected Notes Index (LBUTRUU Index). Total returns assume reinvestment of interest and capital gains. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

4. Is this normal?

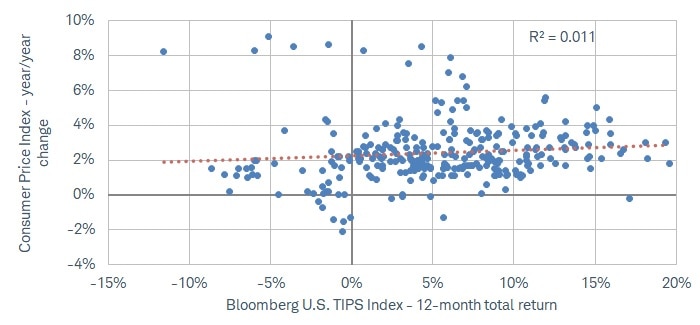

The magnitude of the losses this year isn't normal, with the 12-month return of the TIPS index through the end of September being the worst on record. But historically, over one year time horizons, there hasn't been much of a relationship between the total return of the TIPS index and the change in the consumer price index.

The chart below compares the year-over-year change in the CPI to the 12-month rolling return of the Bloomberg U.S. TIPS Index since index's inception in 1997. Although the trendline is upward sloping, there's not much of a relationship between the two measures—one more reason why TIPS can help protect against inflation over the long run, but why they shouldn't be considered an inflation hedge.

There hasn't been much of a relationship between TIPS returns and the change in the CPI over 12-month time horizons

Source: Schwab Center for Financial Research with data from Bloomberg.

Bloomberg U.S. TIPS Index (LBUTTRUU Index) and US CPI Urban Consumers YoY NSA (CPI YOY Index). Data from March 1998 through September 2022. Total returns assume reinvestment of interest and capital gains. Indexes are unmanaged, do not incur fees or expenses, and cannot be invested in directly. Past performance is no guarantee of future results.

Note: This scatter plot graph shows the relationship between the 12-month change in the CPI (Y axis) and the 12-month total return of the Bloomberg U.S. TIPS Index (X axis). The dotted red line represents the trendline, while the R-squared is statistical measure that helps explain the strength of the relationship between an independent and dependent variable, and is on a scale of 0 to 1.

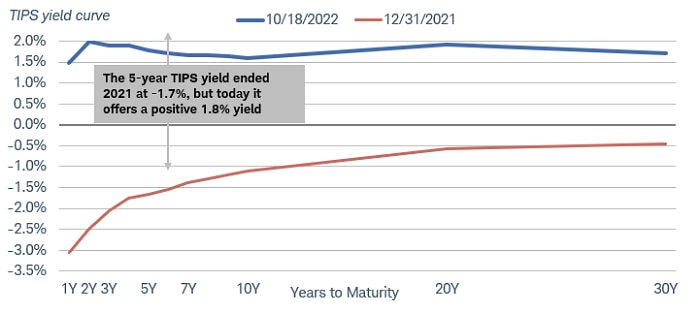

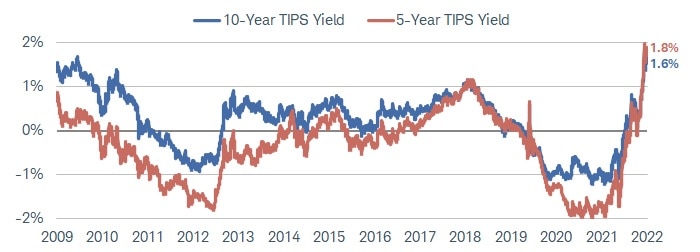

5. What sort of yields do TIPS offer today?

TIPS yields are all positive. That might not seem like much, but TIPS yields generally spent much of 2020 and all of 2021 in negative territory. Today, most TIPS yields are around 1.5% or above, significantly higher than where they ended last year.

TIPS yields have risen sharply this year

Source: Bloomberg, as of 10/18/2022.

US Treasury Inflation Indexed Curve (YCGT0169). Past performance is no guarantee of future results.

With TIPS yields at their highest levels in more than 10 years, we don't see much room for additional upside. Given that outlook, we don't expect prices to fall much further, but we do expect volatility to remain elevated as the Fed aggressively hikes rates.

TIPS yields haven't just risen sharply this year—many are at more than 10-year highs

Source: Bloomberg, using daily data as of 10/18/2022.

US Generic Govt TII 5 Yr (USGGT05Y Index) and US Generic Govt TII 10 Yr (USGGT10Y Index). Past performance is no guarantee of future results.

TIPS yields are "real" yields, meaning they are already adjusted for inflation. But another way to consider those "real" yields is to consider the impact of inflation on the nominal returns.

The annual rate of inflation over the life of a TIPS is ultimately added to the stated yield when held to maturity. If inflation averages 3% for the next five years, for example, that 3% inflation rate would get added to the roughly 1.8% "real" yield that five-year TIPS offers today—resulting in a nominal return of 4.8% annually. The higher (or lower) inflation comes in, the higher (or lower) that nominal total return would be. That can be an important concept for investors who are worried that inflation will remain very elevated for a while.

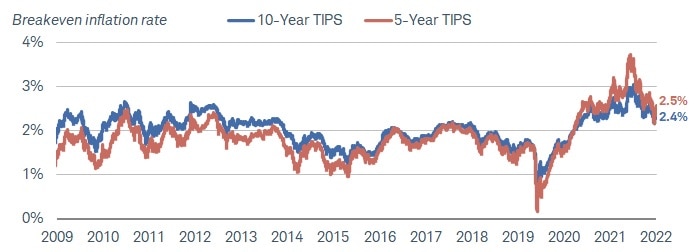

6. How can I compare TIPS to traditional Treasuries?

Breakeven inflation rates. The breakeven rate is the difference between the yield of a nominal Treasury and the yield of a TIPS with a similar maturity. For TIPS investors, the breakeven rate can be considered a hurdle rate—it's what inflation would need to average over the life of the TIPS for it to outperform the nominal Treasury.

Breakeven rates are well off their recent highs. At 2.5%, the five-year TIPS breakeven rate is well off its recent high of 3.7% hit the past March. If the CPI were to average more than 2.5% over the next five years, the five-year TIPS would outperform a five-year nominal Treasury. (Likewise, if inflation averaged less than 2.5%, the nominal Treasury would outperform.)

TIPS breakeven rates are relatively low given the high current rate of inflation

Source: Bloomberg using daily data as of 10/18/2022.

US Breakeven 5 Year (USGGBE05 Index) and US Breakeven 10 Year (USGGBE10 Index). Past performance is no guarantee of future results.

While the current breakeven rates are elevated relative to the last 20 years, they are still well below the current rate of inflation. Considering that the CPI rose by 8.2% during the 12 months ending September 2022, a 2.5% breakeven rate seems relatively low.

7. When I look at various mutual funds or exchange-traded funds (ETFs) that hold TIPS, why are the stated yields so different?

TIPS' mutual fund or ETF yields may appear distorted due to short-term fluctuations in the CPI, and they might not be reflective of the market yield of the underlying securities. Yield calculations may also differ across fund sponsors.

For example, the SEC yield—a standardized yield developed by the Securities and Exchange Commission (SEC)—may be distorted when there's a lot of fluctuation in the monthly payments. While the SEC yield is designed to allow for a fairer comparison of bond funds, there are pitfalls to using it with bond funds that hold TIPS. The yield for a TIPS fund is adjusted monthly based on changes in the rate of inflation, and these changes can cause the yield to vary substantially from month to month. Very high or low yields are attributable to the rise and fall in inflation rates and might not be repeated.

8. Anything else I should know?

Yes—consider the potential for deflation for TIPS with short-term maturities.

TIPS mature at the greater of the adjusted principal or the initial value at issuance. Investors who buy new-issue TIPS are therefore protected against deflation, but that's not the case when buying TIPS in the secondary market. If you buy a TIPS that already has been adjusted higher, and then the CPI begins to decline, you could actually lose money.

That might seem unlikely given that inflation continues to run relatively hot, but the "headline" CPI index that TIPS are referenced to includes volatile food and energy prices. If energy prices (or any other prices, for that matter) resume their downward trend, monthly CPI readings potentially could begin to fall.

What to do now

Consider TIPS if you're looking for long-term inflation protection. With real yields well above zero, investors can finally earn higher income with TIPS while also helping protect against inflation over the long run.

We don't believe TIPS yields should rise much further, so we believe the worst of the price declines is likely behind us. However, Treasury market volatility has been elevated this year, and we expect it to continue as the Fed tightens financial conditions. Additional price declines are therefore still possible, reiterating our view that TIPS shouldn't be considered short-term hedges against inflation—but they can help over the long run.

For individual TIPS holders, any potential price declines might not matter if they're held to maturity. For those who invest in TIPS through ETFs or mutual funds, that could mean modest declines from here, but that doesn't mean you need to abandon your holdings. If yields rise and the funds rebalance, investors may be rewarded with higher income payments to help offset some of the potential price declines, while additional increases would result in positive principal adjustments to the underlying holdings.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All