Given the topsy-turvy nature of the market thus far in 2023, it remains crucial for investors to know what they are buying—especially as it relates to growth, value, and quality.

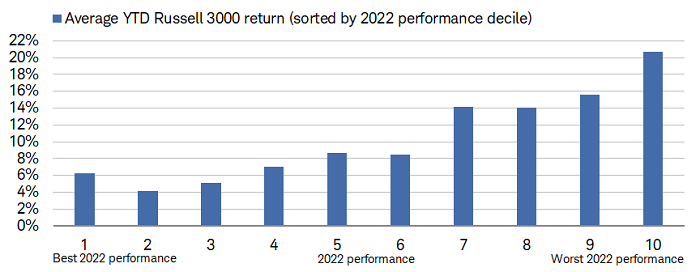

At the macro level, summing up year-to-date market leadership is nearly as simple as saying it has been one big mean reversion trade. In other words, stocks that fell the most in 2022 have been outperforming over the past couple months. As you can see in the chart below, the contrast is stark. Grouping the Russell 3000 (the best way to capture the "whole" market) into deciles based on 2022 performance, you can see (via the left-most column) that the best performers in 2022 have relatively muted gains this year. Conversely, it's clear (via the right-most column) that the worst-performing stocks in 2022 have surged thus far in 2023.

From worst to best, in two months

Source: Charles Schwab, Bloomberg, as of 3/3/2023.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

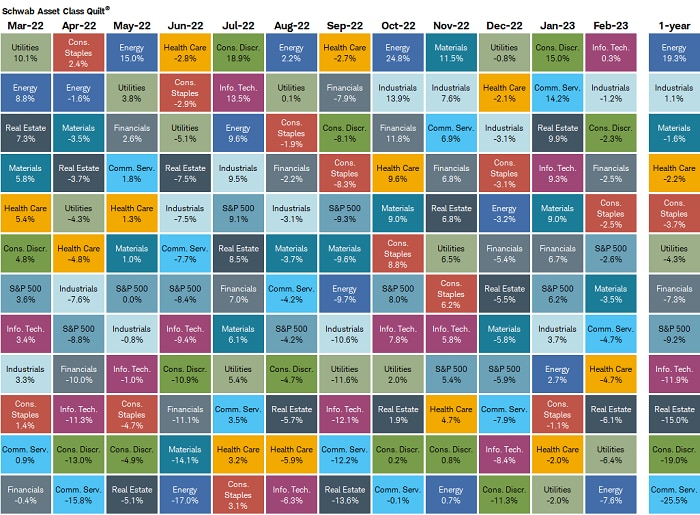

Reversals have been just as strong at the sector level. Shrinking the scope of stocks to just the large-cap space, let's take a deeper look at leadership switches among the S&P 500®'s sectors. Inspired by the flip of the calendar (or something else), investors embraced a huge swing in leadership at the start of 2023. As shown in the sector quilt below, Consumer Discretionary surged in January (outpacing all sectors) while Utilities fell the most. That was the complete opposite of the leader/laggard profile in December.

Through February, the resurgence in the large-cap "growth" trade (more on why we put that in quotes later in this report) continued to hold up relatively well, albeit with more muted gains. Not only that, but the "growth trio" of Information Technology (Tech), Consumer Discretionary, and Communication Services continued to lose its monolithic status. One of the themes within "growth" stocks over the past year has been a notable performance discrepancy between some of the largest names in that cohort. One way to see that split is in the far-right column, in which you can see a large divergence between Tech and Communication Services.

Sector shifts large and swift

Source: Charles Schwab, Bloomberg, as of 2/28/2023.

Sector performance is represented by price returns of the following 11 GICS sector indices: Consumer Discretionary Sector, Consumer Staples Sector, Energy Sector, Financials Sector, Health Care Sector, Industrials Sector, Information Technology Sector, Materials Sector, Real Estate Sector, Communication Services Sector, and Utilities Sector. Returns of the broad market are represented by the S&P 500. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

A mean, meme reversion

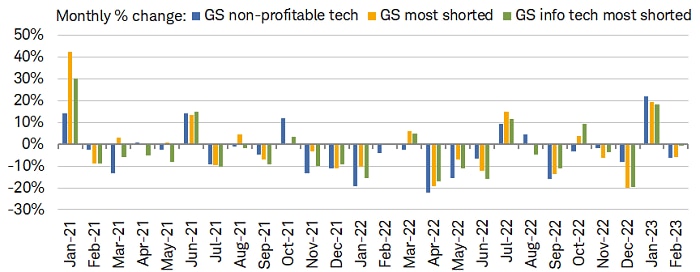

Whether the current move off the October lows proves to be another bear market rally will only be confirmed with time. Worth noting, though, is that some of its drivers (earlier in January) have been consistent with prior bear rallies in the back half of 2022—most notably the strongest from mid-June through mid-August, when investors were bulled up on hopes that the Federal Reserve was set to pivot quickly to rate cuts.

Similar hopes emerged at the start of the year on the heels of slower economic data at the end of 2022. Much of that translated into major outperformance for speculative segments of the market. As shown in the chart below, non-profitable and heavily shorted stocks (both tech and non-tech) surged by double-digit percentage points in January—notching their best gains since the meme frenzy in early 2021.

We continue to have high conviction that market leadership will not be dominated by non-profitable, speculative names. That isn't only due to the reversal in performance in February, but also because the fed funds futures market has virtually priced out all expectations of Fed rate cuts this year. With investors coming to grips with higher-for-longer rates, they have recognized (and likely will continue to recognize) that companies reliant on zero interest rates should struggle in an environment of expensive capital.

Flash rally in speculation

Source: Charles Schwab, Bloomberg, as of 2/28/2023.

Goldman Sachs (GS) non-profitable technology basket consists of non-profitable U.S.-listed companies in innovative industries. Technology is defined quite broadly to include new economy companies across GICS industry groupings. Goldman Sachs (GS) most-shorted basket contains the 50 highest short-interest names in the Russell 3000; names have a market cap greater than $1 billion. Goldman Sachs (GS) info tech most-shorted basket contains the top 20 Information Technology stocks with the highest short interest as a % of float in Russell 3000; names have a market cap greater than $1 billion. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance does not guarantee future results.

"Growth" vs. "Value"

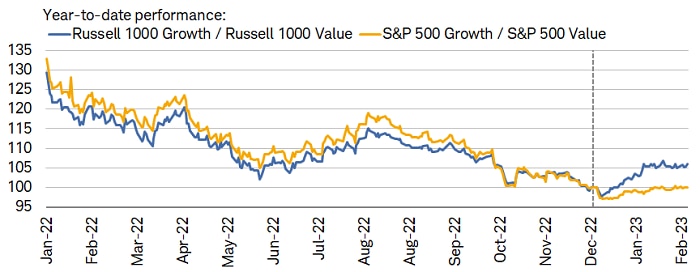

Another defining characteristic of the market's rally this year has been the outperformance of growth stocks relative to their value counterparts…or has it? Our regular readers know that we do not provide tactical recommendations on growth and value from an index perspective; chiefly because there are often major differences between the characteristics of growth and value (lowercase "g" and "v") and the index labels/constituents of Growth and Value (uppercase "G" and "V").

Even within different indexes, there can be a stark contrast in sector weights, which in turn distorts performance (and often leaves investors confused). This has been prevalent recently when comparing the Russell family of indexes to the S&P family. As shown in the chart below, Russell 1000 Growth has outpaced Russell 1000 Value by 6% this year, whereas S&P 500 Growth hasn't had any edge over S&P 500 Value. It's quite a divergence, considering both ratios moved in lockstep with each other last year.

Growth outperformance not uniform

Source: Charles Schwab, Bloomberg, as of 3/3/2023.

Data indexed to 100 at 12/31/2022. An index number is a figure reflecting price or quantity compared with a base value. The base value always has an index number of 100. The index number is then expressed as 100 times the ratio to the base value. Past performance is no guarantee of future results.

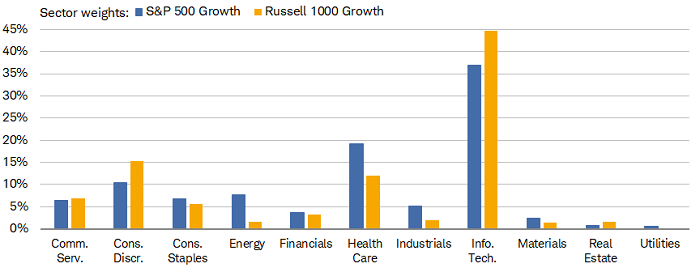

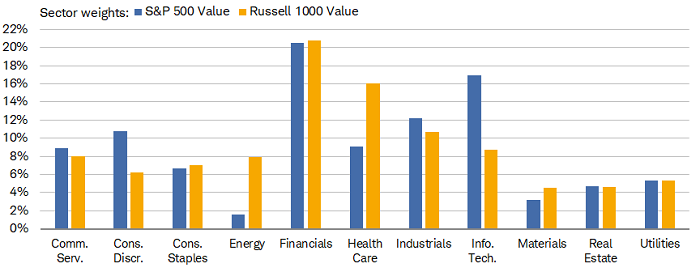

Accounting for the change is the difference in sector dominance within each index. S&P does its annual index rebalancing in December, while Russell does theirs in June. As shown in the pair of charts below, S&P 500 Growth now has a smaller share of Tech and larger share of Health Care compared to Russell 1000 Growth given December's rebalancing. Not only that, S&P 500 Value now has a much larger share of Tech; and in fact, the sector is the second-largest weight in the Value index, behind Financials. Yes, you read that correctly.

Follow your preferred index wisely

Source: Charles Schwab, Bloomberg, as of 2/28/2023.

For illustrative purposes only. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly.

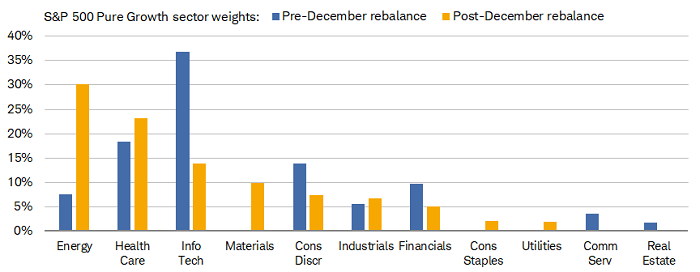

Diving one level deeper into the growth and value discussion, let's focus on one of the most interesting developments that has taken place over the past few months. When S&P rebalanced its Growth and Value indexes in December, there were huge adjustments made not only to the indexes shown above, but also to S&P's Pure Growth and Pure Value indexes. Those Pure indexes have no overlap with each other, meaning a stock can only show up in one or the other (not the case with the regular S&P Growth and Value indexes, where some stocks reside in both).

As shown below, the December rebalance ushered in a huge drop in Tech's weight and a spike in Energy's weight within S&P 500 Pure Growth. Again, you're reading this correctly: Energy is now the largest weight in the Pure Growth index and Tech is only the third largest.

Pure Growth looks less "growthy"

Source: Charles Schwab, S&P 500 Dow Jones Indices, as of 12/19/2022.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly.

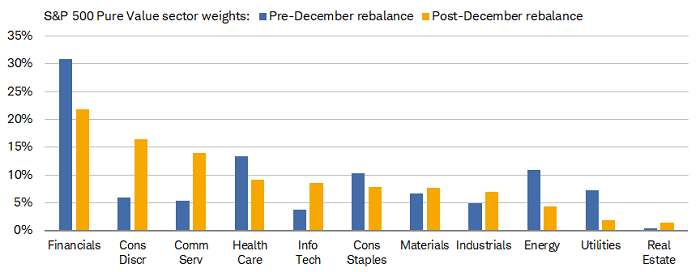

There was a less dramatic shift in S&P 500 Pure Value, in that the leadership status of Financials didn't change. However, the sector did lose some weight in the index, giving way to an increase for both Consumer Discretionary and Communication Services. Interestingly, both sectors have larger weights in S&P 500 Pure Value than they do in S&P 500 Pure Growth (Communication Services isn't even in the latter anymore).

Pure Value gets some more "growth"

Source: Charles Schwab, S&P 500 Dow Jones Indices, as of 12/19/2022.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly.

For index-oriented followers, this hammers home a point we often make when discussing growth and value. If you are investing based on the indexes themselves, it is crucial to be aware of what you're buying. Investors focusing on S&P 500 Pure Growth, for example, might be disappointed if they're looking for—or assuming they'll get—outsized Tech exposure; and they might be equally as surprised that they'd be much more exposed to Energy than any other sector.

In sum

It's been a topsy-turvy start to 2023, with mirror-image leadership relative to last year. We continue to recommend that investors fade the low-quality/speculation-driven rally and instead lean into higher-quality stocks. For index-oriented followers, caveat emptor, given the divergent sector breakdown among the Russell and S&P Growth and Value indexes. "Growth" favorite Tech has passed the leadership baton to Energy withing S&P's Growth indexes; other "growth" favorites—Consumer Discretionary and Communication Services—are moving up in weight within S&P's Value indexes. In an environment with active management competing on a more level playing field with passive indexing, knowing what you're buying is crucial.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Investing involves risk including loss of principal.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Diversification and rebalancing strategies do not ensure a profit and do not protect against losses in declining markets.

Short selling is an advanced trading strategy involving potentially unlimited risks, and must be done in a margin account. Margin trading increases your level of market risk. For more information please refer to your account agreement and the Margin Risk Disclosure Statement.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

S&P 500 Pure Growth is a style-concentrated index designed to track the performance of stocks that exhibit the strongest growth characteristics by using a style-attractiveness-weighting scheme.

S&P 500 Pure Value is a style-concentrated index designed to track the performance of stocks that exhibit the strongest value characteristics by using a style-attractiveness-weighting scheme.

© Charles Schwab

Read more commentaries by Charles Schwab