Elevation: Largest Stocks to Market's Rescue?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn the face of banking stress and a hawkish Federal Reserve, stocks have advanced impressively so far this year, but narrow breadth doesn't bode well for continued strength.

If all you knew were the facts in the list below, what might the most logical conclusion be in terms of the stock market's performance? In just the past few months, we've seen:

- The second and third largest bank failures in U.S. history;

- The Federal Reserve continue its most aggressive tightening cycle in decades, bringing the fed funds rate to the highest since 2007;

- Core PCE inflation (year-over-year) move from 4.7% in January to 4.6% in February, still well above the Fed's target;

- The two-year U.S. Treasury yield slide from a high of 5.07% in early March to a low of 3.55% just a few weeks later (the fastest drop of that magnitude since October 1987).

Conventional wisdom and simple logic might suggest the above list paints a dire scenario for the market. Yet, the S&P 500 finished higher by 3.5% in March, while the Nasdaq jumped by 6.7%. That brought first quarter (and year-to-date) gains for both indexes to 7% and 16.8%, respectively. Some have cheered a "new bull market" for mega-cap tech/growth indexes (like the Nasdaq 100) that have climbed by more than 20% from their December low; while bears have pointed to the lack of participation down the cap spectrum (the Russell 2000 has gained only 2.3% year-to-date) as a building risk.

Au contraire

To give some credence to the bears' argument, it is noteworthy that the market's recent rally has looked incredibly anemic when it comes to participation. That can be shown in numerous ways, the first of which is the performance of the S&P 500 equal-weight index relative to its cap-weight counterpart. As you can see in the chart below, the ratio has plunged so far this year, eliminating much of the edge equal-weight had until recently. A short look back at the past two bear markets shows that a steep drawdown in this ratio is consistent with acute pain in the broader market. This time, it's much more about the outperformance of larger members as opposed to massive losses for the rest of the crowd.

All else is not equal

Source: Charles Schwab, Bloomberg, as of 3/31/2023.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance does not guarantee future results.

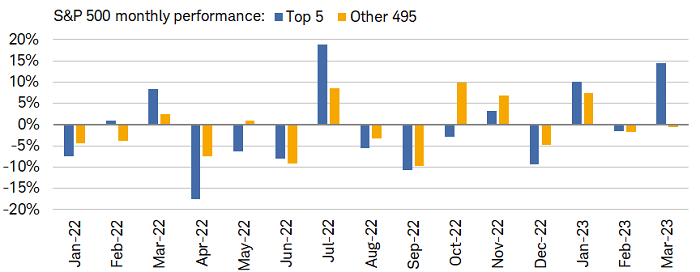

Zooming in on the current bear market, it's clear that performance this year has been dominated by just a handful of names. As shown below, the five largest stocks in the S&P 500 have dominated performance this year, with their average performance totaling +10.1% in January, -1.5% in February, and +14.4% in March. That is in stark contrast to the rest of the index, which saw an average move of +7.4% in January, -1.7% in February, and -0.5% in March.

Take five

Source: Charles Schwab, Bloomberg, as of 3/31/2023.

"Top 5" represent five largest stocks in the index by market capitalization in any given month. "Other 495" represent the rest of the index not included in the top five. Past performance is no guarantee of future results.

Broadening this out a little, the 10 largest stocks in the S&P 500 were responsible for 90% of the index's first-quarter increase, with the triumvirate of Apple, Microsoft, and Nvidia contributing more than 50%. (The remaining seven stocks are Tesla, Meta, Alphabet, Amazon, Salesforce, AMD and Broadcom.)

Perhaps unsurprisingly, the largest stocks' outperformance is consistent with narrow leadership at the sector level. Shown below is our crowd-favorite sector quilt, which maps out the S&P 500 sectors' performance each week this year. You can see that the "growth trio" of Tech, Communication Services, and Consumer Discretionary has hogged the top of the leaderboard this year, while all the rest of the sectors have stayed in negative territory.

"Growth trio" holding up gains

Source: Charles Schwab, Bloomberg, as of 3/31/2023.

Sector performance is represented by price returns of the following 11 GICS sector indices: Consumer Discretionary Sector, Consumer Staples Sector, Energy Sector, Financials Sector, Health Care Sector, Industrials Sector, Information Technology Sector, Materials Sector, Real Estate Sector, Communication Services Sector, and Utilities Sector. Returns of the broad market are represented by the S&P 500. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

A "value" clash: Tech vs. Financials

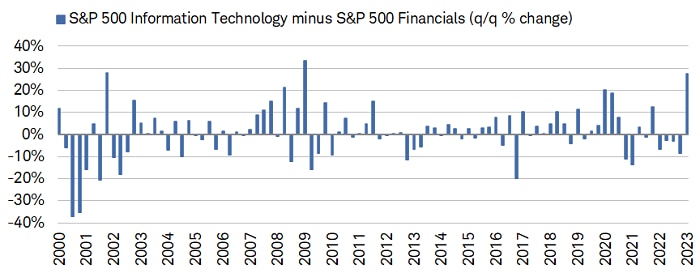

As the above quilt chart shows, the Financials sector has only spent one week at the bottom this year, but persistent pressure has been enough to send the sector to the bottom of the leaderboard year-to-date. It's a far cry from Tech's 21.5% gain, putting the spread between Tech and Financials at 27.6% for this year, as shown in the chart below. That is the widest gap since the first quarter of 2009.

Mind the gap

Source: Charles Schwab, Bloomberg, as of 3/31/2023.

Performance is represented by price returns. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

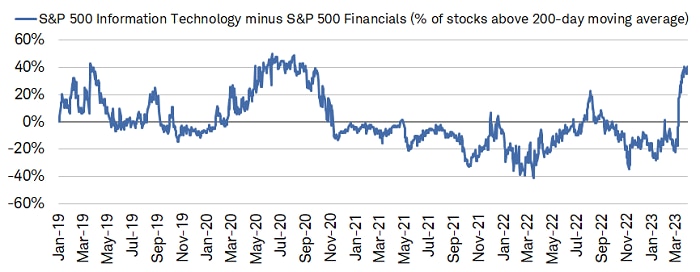

Not only that, but the difference in the share of members in the Tech and Financials sectors trading above their 200-day moving averages has disproportionately favored the former, as shown in the chart below. Tech hasn't seen relative strength like this since the end of 2020.

Financials struggling relative to Tech

Source: Charles Schwab, Bloomberg, as of 3/31/2023.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

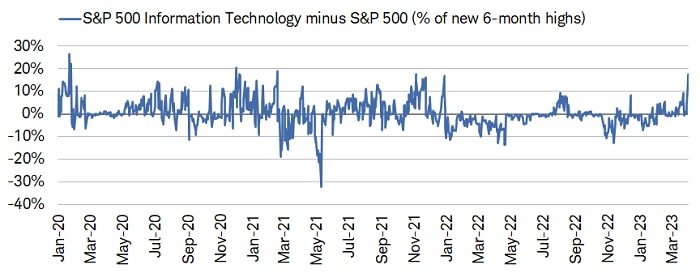

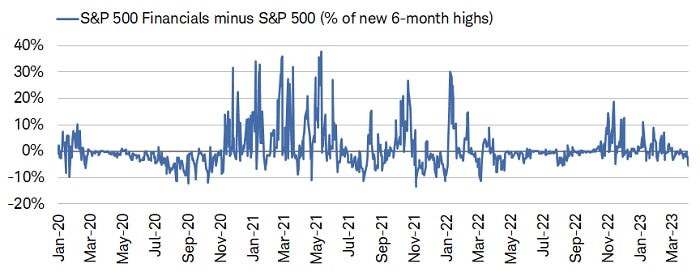

Not all of that is simply due to the weakness that is pervading the Financials space. The percentage of members in the Tech sector making new six-month highs has improved sharply of late when compared to the S&P 500. You can see in the chart below that the spread has turned positive, climbing to the highest since late 2021.

More Tech participation

Source: Charles Schwab, Bloomberg, as of 3/31/2023.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

Conversely, the spread for Financials relative to the S&P 500 has weakened over the past few months, which isn't terribly surprising given the stress and fear dominating the sector since the failure of Silicon Valley Bank (SVB).

Financials' strength waning

Source: Charles Schwab, Bloomberg, as of 3/31/2023.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

The widening divide between Tech and Financials is notable for a couple reasons, not least being the fact that the latter sector is typically looked to for confirmation of a new bull market. History shows that Financials' lack of participation has often capped the upside for a rally. Conversely, over the past year, the concentration in leadership up the cap spectrum—and in growth sectors like Tech—has at times preceded drawdowns and bouts of volatility for the market.

Another notable aspect of the divided performance is the "value-like" nature of both sectors. Tech is almost never considered a value sector, but as we wrote in early March, the recent rebalancing of the S&P 500 Value Index made the sector the second-largest in the index, only behind Financials. This is yet another example of why we emphasize the differences between indexes and factors when it comes to growth and value sectors. One can say that growth is outperforming value this year, but if you're looking within an index like S&P 500 Value, it's really value (Tech) that's outperforming value (Financials).

Love it or H.8 it

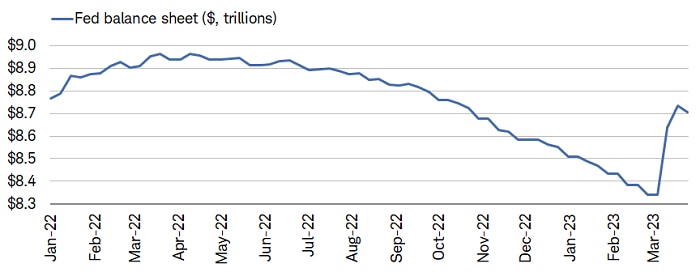

Recent stress in the banking sector—precipitated by the collapse of SVB—has put nonconventional data points under the microscope of late. Prior to March, most investors weren't focused on details of the Fed's balance sheet and/or deposits at small banks—the H.4.1 and H.8 reports, respectively. Yet, focus has rapidly shifted to the emergency borrowing some lenders are having to undertake. As shown in the chart below, the Fed's balance sheet expanded markedly in mid-March, underscoring stress in the banking system. Fortunately, total assets reversed lower last week, which, if continued, would signal an ongoing stabilization in the financial system.

On balance, still a huge increase

Source: Charles Schwab, Bloomberg, as of 3/29/2023.

The Fed balance sheet is the U.S. Federal Reserve System's balance sheet of assets and liabilities.

What to watch for

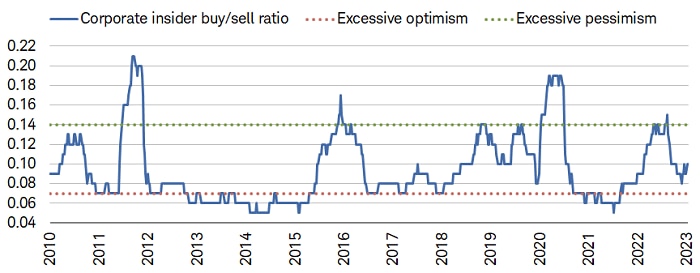

Fast-shifting market dynamics this year (especially with respect to leadership dynamics in 2022) have kept most investors away, evidenced by the relative lack of equity ETF fund inflows of late. Somewhat conversely, corporate insiders have started to up the purchase of their own shares. As shown below, the corporate insider buy/sell ratio has risen over the past few weeks, after falling close to excessive optimism territory. Worth noting is the fact that ratios at the sector level can vary widely; for example, Financials insiders have been scooping up a lot of stock (insiders tend to have a contrarian bent, buying as prices move lower), while Consumer Staples insiders haven't matched that enthusiasm.

Insider buys pick up

Source: Charles Schwab, SentimenTrader, as of 3/27/2023.

Buy/sell ratio represents total number of corporate insiders of S&P 500 companies that have bought shares on the open market during the past six months versus those that have sold shares.

The trend in insider activity is consistent with other sentiment metrics of late, some of which have recently jumped out of pessimistic territory. For now, sentiment isn't as much of a risk, but we'd start to flag it if equities continue to extend their rally in the face of deteriorating economic fundamentals and a persistently hawkish Fed.

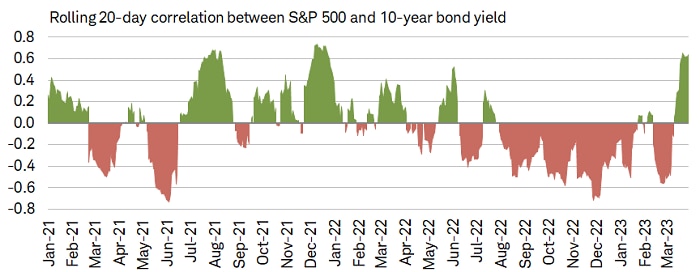

Also worth watching is the relationship between stock prices and bond yields, which we've highlighted numerous times over the past year. The next chart below is typically shown on a longer-term basis (a rolling 120-day correlation), but we've shortened the horizon to a rolling 20-day basis. You can see that the relationship between the S&P 500 and 10-year U.S. Treasury yield has jumped sharply into positive territory, which means stocks and yields have been moving together.

Stocks and bonds moving together again

Source: Charles Schwab, Bloomberg, as of 3/31/2023.

Correlation is a statistical measure of how two investments have historically moved in relation to each other, and ranges from -1 to +1. A correlation of 1 indicates a perfect positive correlation, while a correlation of -1 indicates a perfect negative correlation. A correlation of zero means the assets are not correlated. Past performance is no guarantee of future results.

The positive aspect of that is the fact that inflation concerns (higher yields) haven't been weighing on stocks, which reconnects the positive relationship investors enjoyed for much of the past two decades. The downside—at least in the medium term—is that lower yields and lower stock prices would be increasingly consistent with weaker economic growth and, eventually, a recession. It's too soon to tell whether the positive relationship will hold, but if it does, the upside is that bonds would reestablish themselves as a hedge for stocks.

In sum

In 2021, the stock market was characterized by significant strength in the indexes (like the S&P 500 and Nasdaq)—with the largest cap stocks dominating performance—but there was notable weakness and churn under the surface. Last year, indexes suffered bear-market declines, but at the mid-October lows, underlying breadth had improved, with the average stock outperforming the indexes. So far this year, the indexes are showing better performance courtesy of the strength of the largest stocks, but churn under the surface has resurfaced.

As investors learned last year, often the hard way, there can be pops in shorter-term breadth; but without confirmations from longer-term breadth, rallies have a tendency to ultimately fade. Strong outperformance from the "generals" (largest stocks) can power indexes higher, but a healthier market would be characterized by greater participation by the "soldiers."

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Investing involves risk including loss of principal.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income, small capitalization securities and commodities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All