Debt Ceiling Standoff

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPolitical brinkmanship in Washington adds to concerns about the economy.

Markets are keeping a wary eye on Washington, where the urgency is growing for lawmakers to resolve the debt ceiling standoff before the federal government runs out of money—which the Treasury says could be as early as June 1st. Although the stock market has been relatively sanguine, concerns have seeped into the Treasury market. Meanwhile, global markets are grappling with diverging views on what central banks will do next.

Washington: Stalemate

Concern about the debt ceiling intensified in Washington and on Wall Street after a May 9th White House meeting between the president and top Congressional leaders produced little progress on a stalemate that threatens to roil the markets and hurt the economy.

The meeting was the first face-to-face discussion between President Joe Biden and House Speaker Kevin McCarthy (R-Calif.) since February. Both reiterated their incompatible positions. The president and congressional Democrats continue to stand by their long-held position that Congress should pass a clean debt ceiling increase with no strings attached, while Republicans say they will only consider lifting the debt ceiling if it is paired with spending cuts and other policy priorities.

The need for a resolution is becoming urgent. Treasury Secretary Janet Yellen told Congress in a May 1st letter that the U.S. could default as soon as June 1st, though her letter indicated that the imprecision of predicting Treasury revenues and outlays could push the default date later into the summer. That uncertainty has made it difficult for Congress to set a real deadline for negotiations.

The Republican majority in the House narrowly passed a bill on April 27th that would raise the debt ceiling by $1.5 trillion or until March 31, 2024, whichever comes first. The bill also outlined nearly $5 trillion in spending cuts over the next 10 years, though it did not include any specific cuts. The legislation also would repeal about $72 billion in funding for the IRS and repeal several green-energy provisions that were approved last year as part of the Inflation Reduction Act; streamline the permitting process for energy projects; increase work requirements for recipients of food stamps and Medicaid; and claw back unspent funds that were allocated to fight the COVID-19 pandemic. McCarthy has repeatedly said that the House bill should be the starting point for negotiations. But that bill is a nonstarter in the Democrat-controlled Senate.

The next steps are uncertain, though participants in the May 9th White House meeting agreed to a follow-up meeting during the week of May 15th. With the clock continuing to tick toward an unprecedented default, the pathway to a resolution remains as murky as ever.

Fixed income: The potential cost of default

It seems like the markets just can't get away from the never-ending drama in Washington, D.C. Because Congress has always ended up raising the debt ceiling in the past, the debate has come to be seen as political brinkmanship rather than a serious issue. However, concerns are building this time because the two sides are just so far apart. Yields for short-term Treasuries maturing in the next few months are elevated compared to those maturing in the third quarter, as investors shy away from the risk that the interest on T-bills could be deferred—i.e., a "technical default."

The standoff also has heightened the uncertainty about the economy. A default would risk sending short-term yields higher, while riskier assets and the dollar would likely fall. This is the scenario that played out in the 2011 debt ceiling fight, which resulted in the U.S. federal government credit rating being downgraded by several rating agencies, including Standard & Poor's, to below AAA for the first time ever.

If no deal is reached, the Treasury has a couple of options:

1. Technical default. A technical default is defined as an extended period of time of non-payment of interest and principal on the debt. It happens from time to time in emerging-market countries, but not in major developed countries with the ability to pay. An actual default is more likely when a government does not have the ability to pay, which often results in a restructuring of the debt. In the U.S., the issue is an unwillingness to pay and assuming an agreement were eventually reached, investors would receive their interest and principal payments—likely with extra accrued interest.

The market reaction would likely be quite severe, however—potentially a spike in short-term interest rates, a drop in the value of the U.S. dollar, and a downgrade by major rating agencies. Banks and financial institutions that use short-term U.S. Treasuries for financing would likely bid up the price to secure liquidity. It could mean a long-term rise in the cost of borrowing for the U.S. government.

On the economic front, the spike in interest rates would likely cause a recession, sending the unemployment rate higher.

2. Creative possibilities: Premium bonds/minting a platinum coin/invoking the 14th Amendment. Among the more creative suggestions that commentators have made is that the Treasury could issue premium bonds—bonds with higher coupons—that would generate a price that is above par, giving the Treasury more cash. It's not clear how this would work in practical terms. And the Treasury secretary has dismissed the idea.

There also has been a suggestion that the Treasury could mint a trillion-dollar platinum coin, place the money at the Fed and use the proceeds to pay the country's bills. This seems pretty far-fetched and potentially illegal.

Finally, there is talk that the Treasury could invoke Section 4 of the 14th Amendment—which states that "the validity of the public debt of the United States, authorized by law, including debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellions, shall not be questioned"—and just keep paying the bills. However, Yellen has downplayed that idea as well, calling it a "constitutional crisis" during a television interview on May 7th.

Clearly, there are no good choices for the Treasury. Even if feasible, these creative suggestions may not pass muster in court if challenged.

The debt ceiling debate, coming on top of banking sector turmoil, makes any more Fed rate hikes unlikely. The markets are already volatile enough from the impact of rate hikes. The longer the debt ceiling debate lingers, the more damaging it could be for the economy.

U.S. Stocks and Economy: The Market's Battles

Amid myriad concerns for investors this year, the labor market remains in focus given its strength in key areas. In April, the U.S. unemployment rate fell to 3.4%, average hourly earnings grew by 4.4% year-over-year, and 253,000 jobs were created. The latter data point far outpaced economists' estimates of 185,000 and March's gain of 165,000. However, the rub is that March's gain was revised down heavily (by 71,000 jobs). The pace of job creation, while still strong, is continuing to slow down.

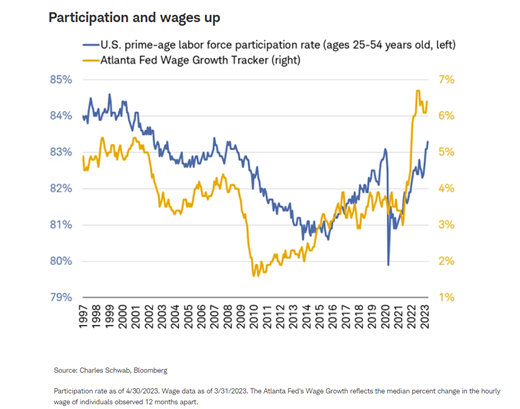

One of the brightest spots of the April jobs report was the prime-age labor force participation, which rose to its highest since March 2008. That underscores continued success in getting workers back into the workforce, which is exactly what the Fed has been looking for. It hasn't yet led to easing wage growth, however, as you can see in the chart below. As that takes longer to unfold, it will likely help keep pressure on the Fed to keep rates higher for longer.

To be sure, strong wage growth is typically desired and a feature of a strengthening economy. Yet, when inflation remains an issue, faster and stronger pay hikes make it more difficult for the Fed to maintain price stability. One way that shows up is in higher labor costs for companies. As you can see in the chart below, the annual change in unit labor costs started outpacing the annual change in the consumer price index (CPI) in the first quarter—meaning corporate pricing power is fading as labor grows more expensive. That is consistent with prior instances of the economy either shortly entering or already being in a recession, given the dynamic is consistent with downward pressure on corporate profit margins.

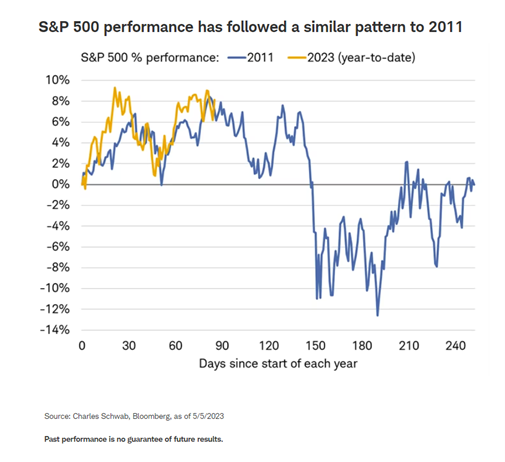

And then there's the debt ceiling, as discussed above. Anxiety has crept into certain markets (notably, the Treasury market), but for now, stocks haven't shown much concern over the possibility of the U.S. defaulting on its debt. You can see in the chart below that, somewhat eerily, the S&P 500's performance this year looks very close to its moves in 2011.

By no means are we suggesting this year is a repeat of 2011, but it's worth pointing out that stocks' waterfall decline that year came after the debt ceiling agreement was reached. Rather than the market scaring legislators into forging a deal, it was the U.S. debt downgrade that sparked a near-bear market.

Global stocks and economy: Data dependence

The central banks of the United States, the eurozone, and Australia were united in hiking policy rates by 25 basis points (bps)1 earlier this month. However, there are divergent views among the members of each of these central banks about what comes next, with hawks and doves at odds over the future path of rates. Even the futures market holds very different views about the trajectory of rates among these central banks. Markets have priced in rate cuts by year-end to varying degrees for the United States, Australia, Canada, and New Zealand, and have projected further hikes in the eurozone, United Kingdom and Switzerland.

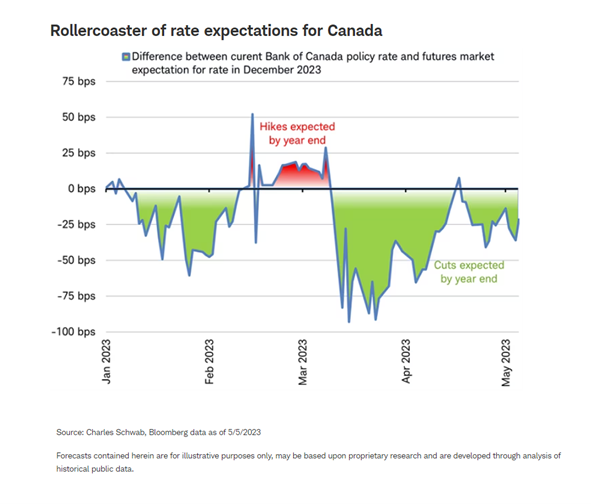

The Federal Reserve and the European Central Bank both have communicated their confidence that the recent bank stress is not systemwide, implying that any changes in policy are not likely to be driven by these events. The market has not reflected the same interpretation of these events, displaying wide swings in expectations for policy rates by year-end over the past few months. For example, the Bank of Canada policy rate expectations for year-end had priced in as much as 50 bps of rate hikes during February, which swung to nearly 100 bps of rate cuts in March as two U.S. regional banks failed. Expectations then moved to no change in late April, then back to cuts again as another U.S. regional bank failed in early May.

Instead of being event-driven, central banks everywhere seem to remain data-dependent, making it hard to be confident that any central banks will pivot to rate cuts soon, given sticky core inflation and a tight global labor market. The Reserve Bank of Australia's (RBA) surprise rate hike in May illustrates the possibility of a restart after a pause. Even though the RBA signaled it was finished hiking and held rates steady in April, it then had to hike again by 25 bps in May. The RBA isn't the only central bank to stop and start again based on policymakers' dependence on the data—we saw Norway do that earlier in the year.

The European Central Bank (ECB) has made it clear it was not finished with rate hikes after stepping down from a pace of 50-bp hikes to a 25-bp hike last week. ECB President Christine Lagarde stressed that there was more work to do in upcoming meetings—suggesting multiple rate hikes are likely in store—to manage the ongoing resilience of economic growth, strong wages, and sticky core inflation.

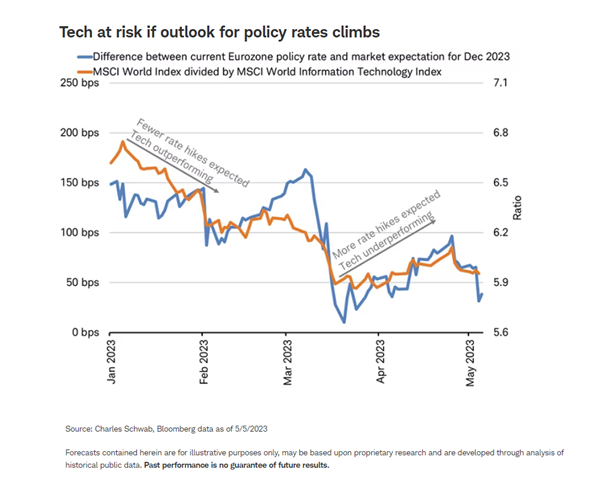

Global technology stocks, in particular, may be at risk if the market prices in more rate hikes by year-end than what is expected today. The chart below highlights the relationship between the tech sector and policy rates, using the market's outlook for the change in ECB rate by year-end as an example. Global tech stocks outperformed the market as the amount of expected rate hikes by year-end faded, and underperformed as the market lifted its year-end rate expectations.

Michael Townsend, Managing Director of Legislative and Regulatory Affairs, and Kevin Gordon, Senior Investment Strategist, contributed to this report.

1 A basis point is one-hundredth of 1 percentage point, or 0.01%, so 25 basis points would be equal to 0.25%.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research, and are developed through analysis of historical public data.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Fixed-income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Currencies are speculative, very volatile, and are not suitable for all investors.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approve or endorse this material, guarantee the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith. 0523-3HX7

To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All