Banking Stress and Preferred Securities: Now What?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBanks and financial institutions are big issuers of preferred securities, so the recent banking industry volatility has had an impact. Our guidance on preferreds is unchanged but with some caveats.

The preferred security market has been hit hard lately. With banks and other financial institutions being the most common issuers of preferreds, the recent banking sector turmoil has resulted in more volatility and lower prices.

Our guidance is unchanged but with some caveats. We continue to suggest a neutral allocation to preferreds, meaning investors can consider them if an investment in preferred securities is in line with their risk tolerance and investing time horizon. Volatility is likely to remain elevated, however, and additional price declines are possible. While the entry point appears attractive for long-term investors, some caution is warranted over the short run.

Most importantly, and as we'll discuss below, security selection is important in the current environment. Preferred securities issued by the large, highly rated banks have generally held up better than preferred issued by small and midsize banks, and we expect that trend to continue.

Preferred security prices remain near their cyclical lows. Closing at $85.7 on May 16th, the average price of the ICE BofA Fixed Rate Preferred Securities Index is still near its lowest level in more than 12 years. Volatility remains elevated, as the right side of the chart below suggests, with prices rising and falling sharply over the past year. Prices initially fell last year as bond yields surged. As hybrid investments with characteristics of both stocks and bonds, preferred securities' long maturities (or no maturities at all) make them very sensitive to interest rate changes. Prices plunged last year as the 10-year Treasury yield rose more than two percentage points.

The recent volatility, however, is due more to bank sector concerns sparked by the early March failures of Silicon Valley Bank and Signature Bank. With banks representing a large share of the market, preferred investors appear concerned that more bank failures could harm the market. Because many bank preferreds are considered a form of stock, there likely wouldn't be much recovery value left for preferred investors should the issuer fail.

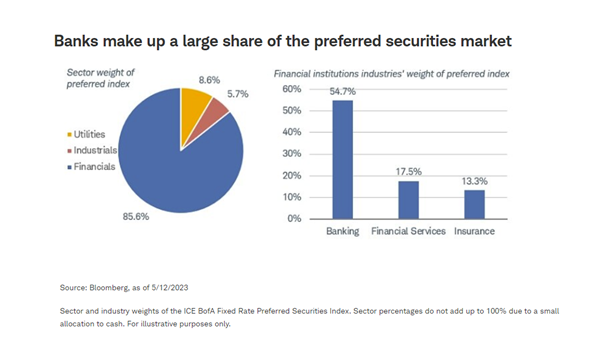

The banking turmoil has had an outsized impact on preferred securities because banks tend to be the largest issuers of preferred. Preferreds issued by financial institutions make up roughly 86% of the ICE BofA Fixed Rate Preferred Securities Index. The Financials sector includes a handful of industries, like banks and insurance companies, for example. As you can see in the chart right below, banks make up almost 55% of the index, the largest share relative to other financial institutions' industries.

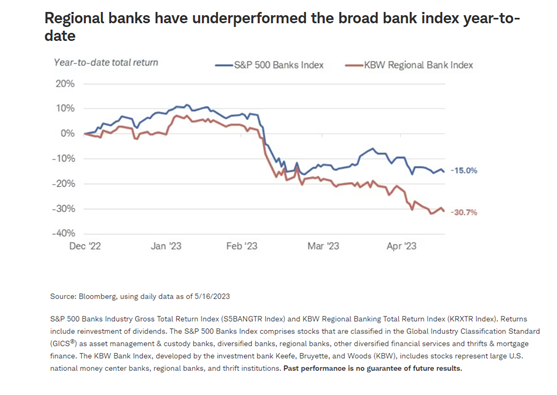

Large U.S. banks have generally performed better than small and regional banks after the recent bank failures—that's been true in both the common stock and preferred stock markets. A key issue leading up to the recent failures was the number of deposits held by banks relative to the value of their bond holdings. Banks generally invest the deposits into investments with higher yields. But given the rise in interest rates last year, the value of many of those bond investments fell, but the value of the deposits didn't. That's a risk if many bank customers should want to withdraw their deposits at the same time because the value of the bank's investments might not be enough to cover those withdrawals.

Given that risk, small and midsize regional bank common stocks have underperformed the broad bank stock market index. The chart below compares the year-to-date total return of the broad S&P 500 Banks Industry Group Index to the KBW Regional Banking Index.

To gauge the performance of the preferreds, we screened for securities using the following criteria:

- Moody's rating of Ba3 or above or Standard and Poor's rating of BB- or above1

- Par values of $25, $50, or $100

- The amount outstanding of $100 million or more

- Denominated in U.S. dollars

- Issued by banks and diversified financial institutions

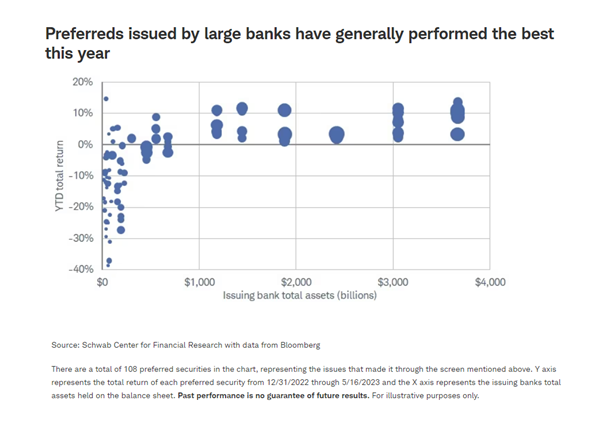

The scatter chart below compares the total returns of the individual preferreds that fit the above criteria with the size of the issuing bank, according to the issuer's total assets. The results are in line with the stock chart above, where regional banks are generally underperforming the broad bank stock index.

In this chart, the year-to-date total returns are on the Y axis, with the issuing banks' total assets on the X axis. The bubbles represent individual preferred securities, and the size of the bubble represents the size of each issue relative to others. For example, the largest bubbles represent preferred issues that have more than $2 billion outstanding, while the smaller bubbles represent issues as small as $100 million.

Preferreds issued by banks with the most assets have performed the best this year. For the securities included in the screen, every preferred security issued by a bank with $1 trillion or more in assets has posted a positive total return this year. When we look at the small and midsize banks, on the left side of the chart, the dispersion of total returns is much wider, and the sizes of the negative returns for some of the issuers have been sharp. Finally, the preferreds that have a relatively small amount outstanding have been some of the worst performers, as illustrated by the size of the bubbles.

We believe this trend may continue, with preferreds issued by large banks holding their value more than those issued by small banks as banking concerns linger. The large, highly rated U.S. banks appear to be in better shape to withstand a potential outflow of deposits, and their more diversified business models can help them weather a potential economic slowdown.

What to do now

Most importantly, make sure that any investment in preferred securities matches your risk tolerance. They should generally be considered moderate- to aggressive-risk investments given their high-interest rate risk and credit risk (the risk that an issuer will fail to make interest payments or pay back principal). For more conservative investors looking for income today, we prefer investment-grade rated corporate bonds. For those investors who are willing to take more risk to earn higher yields, highly rated preferreds appear more attractive than high-yield bonds. If the economy slows, as we expect, high-yield bond prices may fall sharply, but the prices of preferreds issued by the large, highly rated U.S. banks may hold their value better.

If you are considering preferreds, those issued by large, highly-rated banks appear to be the most attractive now. While their prices have generally held up better than the preferreds issued by small and midsize banks, meaning their yields are likely lower, they should perform a bit more defensively should banking turmoil remain a risk in the near term.

Investors who hold individual preferreds should always look at the characteristics of any preferred security they are considering, and not just search for those with the highest yields. If given security—preferred or otherwise—offers a significantly higher yield than what appear to be similar securities, there's likely additional risk with that issue or issuer.

Finally, given the bifurcated nature of the market lately, an approach that uses active management, like a mutual fund or a separately managed account, might make sense. With an active strategy, a portfolio manager can make the decision about what to hold—or more importantly in today's environment, what not to hold.

1 Ba3 represents Moody’s Investors Services rating scale, and BB- represents the Standard & Poor’s rating scale. Ba3/BB- ratings are considered speculative and imply substantial credit risk. The preferred security screen in this article included preferred issues with ratings of Ba3/BB- or above as many banks whose senior unsecured bonds are rated investment grade have preferred securities that are rated a few notches below. Moody’s investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Each rating (aside from Aaa, Ca, and C) has a numerical modifier of 1, 2, or 3. Modifier 1 indicates that the obligation ranks at the higher end of its generic rating category; modifier 2 indicates amid-range ranking; and modifier 3 indicates a ranking in the lower end of that generic rating category. Standard and Poor’s investment grade rating scale is AAA, AA, A, and BBB and the sub-investment grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories.

Investors should consider carefully the information contained in the prospectus or, if available, the summary prospectus, including investment objectives, risks, charges, and expenses. Please read it carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Investing involves risk including loss of principal.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Fixed-income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Preferred securities are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features may affect yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so they are subject to increased loss of principal during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than the original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

The information provided here is for general informational purposes only and is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific advice is necessary or appropriate, consult with a qualified tax advisor, CPA, financial planner, or investment manager.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Investments in managed accounts should be considered in view of a larger, more diversified investment portfolio.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All