With unanimity, the Federal Open Market Committee held the federal funds rate in its current range, but updated projections suggest this rate-hike cycle is not yet over.

The Federal Open Market Committee (FOMC) held the federal funds rate in the 5% to 5.25% range, the first meeting since February 2022 during which the Federal Reserve didn't raise rates. The decision was unanimous and was widely expected by the markets.

Updated Fed projections suggest the rate-hike cycle is not yet over, however. The updated "dot plot" projects a year-end 2023 fed funds rate in the 5.5% to 5.75% range, or an additional 0.5% (50 basis points) in rate hikes later this year. While the Fed "skipped" a hike at this meeting, it signaled that more hikes are likely.

The statement was mostly unchanged, highlighting that economic activity has continued to expand at a modest pace, unemployment remains low, and inflation remains elevated. There was one minor tweak in the statement that further supports the case for more hikes—the statement now says that the committee will determine "the extent of additional policy firming that may be appropriate" to get back to 2% inflation. The previous statement said that the committee will determine "the extent to which additional policy firming may be appropriate" to reach their inflation target. It's a minor change but suggests that the question is now "how much" the Fed will hike rates going forward, rather than "if" it will hike rates.

Taking the statement, updated economic projections, and Fed Chair Jerome Powell's comments at the press conference together, this highlights the Fed's determination to bring inflation down by leaving open the option to hike rates more if needed.

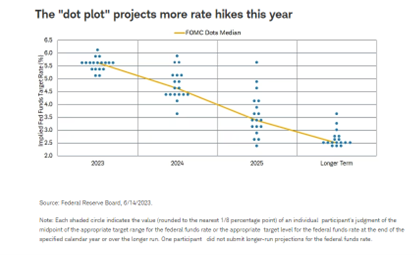

Updated "dot plot" and economic projections

This FOMC meeting was accompanied by the updated Summary of Economic Projections, with the "dot plot" likely drawing the most attention. The "dot plot" provides the projection of each FOMC participant for the fed funds rate at the end of each year.

The median projection for the year-end 2023 fed funds rate is now 5.625%, or in the 5.5% to 5.75% range. That suggests an additional two 25-basis-point rate hikes this year, or one 50-basis-point hike should the committee prefer to raise the rate more quickly. The new year-end 2023 projection is half a percentage point (0.5%) higher than the projection from the March meeting.

The 2024 and 2025 year-end rates were increased as well, but still suggest rate cuts nonetheless. The median year-end 2024 projection was increased to 4.625% from 4.275%, and 2025 was raised to 3.375% from 3.125%.

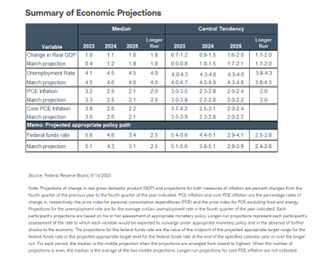

Elevated inflation and the strength of the labor market are two key reasons why the Fed may continue to hike rates, and that was reflected in the updated economic projections. Most of the large revisions to the Fed's economic projections were for this year, with very little change to the economic projections for the years 2024 and 2025.

The median year-end projection for the core Personal Consumption Expenditures (PCE) index, one of the Fed's preferred inflation gauges, rose to 3.9% from 3.6% in March. Core PCE (minus volatile food and energy prices) remains stubbornly high and has proven stickier than anticipated—through April 2023, the year-over-year change was still 4.7%, and it has been stuck in the 4.6% to 4.8% range since November 2022. That's well above the Fed's 2% target, and Powell specifically called out its elevated level in his press conference.

The median projection for the unemployment rate at the end of this year was revised to 4.1% from 4.5%, and the economy is projected to grow more this year than initially projected. With an unemployment rate still at just 3.7% at the end of May, Fed officials have mentioned the need to see labor conditions loosen to bring down spending and consumption, and therefore inflation.

In addition to the potential for more rate hikes this year, the Fed is continuing with its balance sheet reduction plans, also called quantitative tightening (QT). While that has generally been running in the background, it's still a form of tightening. Since the Fed allowed maturing securities to roll off its balance sheet, the Fed's Treasury holdings have declined by more than $600 billion and its mortgage-backed securities holdings have shrunk by roughly $180 billion.

In sum

Although the Fed held its benchmark rate steady for the first time since early 2022, additional rate hikes do seem likely. The Fed is keeping its options open, however, and updated projections don't guarantee additional hikes down the road. Powell suggested that there was no discussion at this meeting about what the committee might do at the July meeting and stated that the updated dots shouldn't necessarily be viewed as an expected "plan."

He also said that the decision to hold rates steady was a continuation of the process in which the Fed has moderated the magnitude of rate hikes. This gives the committee time to evaluate the inflation and labor market landscape before the next meeting.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Investing involves risk including loss of principal.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research, and are developed through analysis of historical public data.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Fixed-income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab