Though recent data suggests China's re-opening growth has slowed, it's likely temporary. As China's recovery continues, it may have implications for U.S. inflation and rates.

After an initial bump, China's post-zero Covid economic recovery appears to have slowed: April retail sales, factory production, and fixed-asset investment, as well as May manufacturing data, all fell short of analyst expectations. But there are reasons for hope, says Jeffrey Kleintop, chief global investment strategist at Schwab. "We believe China will zig while the rest of the world zags in 2023, with accelerating growth and additional stimulus relative to 2022, while other countries slow down and withdraw stimulus." The longer-term worry could be a revitalized China becoming a roadblock in the Federal Reserve's inflation fight.

Stimulus, consumer confidence, diplomacy: Three routes to growth

According to a Bloomberg survey of analysts in late May, the People's Bank of China (PBOC) is expected to cut reserve requirements for major lenders by 25 basis points by the end of the third quarter of 2023. Cutting reserve requirements helps a central bank stimulate economic growth without reducing interest rates.

Additionally, the PBOC has kept interest rates steady for nearly a year at levels below those of Europe and the United States, something it's been able to do in part because inflation remains low. That makes China a more attractive lending environment than many of its global peers. And some analysts think China might reduce rates later this year, though not all economists agree.

With more time and potentially lower rates, consumer confidence could rebound—a vital ingredient for sustained economic growth. Right now, Chinese consumers still appear to be worried about jobs, incomes, and the property market, Jeffrey says. They have used savings to pay down mortgages, and spending has been primarily on experiences. For instance, domestic travel bloomed after the country's reopening but consumers shied away from expensive capital goods.

While consumers appear to remain conservative about the kind of big purchases that can fuel stronger economic growth, auto sales, and production have been bright spots. Second-quarter retail sales growth is expected to improve significantly from the first quarter, according to Trading Economics.

Economists surveyed by Bloomberg expect 7.7% gross domestic product (GDP) growth for China in the second quarter, which would be the best in two years, though to be fair the comparison is easy versus a lockdown quarter a year ago. The data, due in mid-July, are worth watching for hints of potential re-opening progress.

Potentially warmer relations between the U.S. and China could also be a tailwind.

China's been under tough U.S. sanctions enacted during the Trump administration, and President Biden kept the ones initiated by his predecessor and added more, particularly in the semiconductor space. Relations sank to new lows after the spy balloon flare-up earlier this year, but there's hope for improvement.

"There is the potential for some thawing in the relationship as the U.S has restarted diplomatic outreach to Beijing, and high-level revisits could resume," Jeffrey says.

Will China's recovery give the Fed a headache?

Should China get back on track toward growth, it could present some temporary problems for the U.S. Federal Reserve.

"China's demand for commodities, from jet fuel for travel to copper for infrastructure, could begin to build in the second half of the year and offset softening demand in the U.S. and elsewhere, pushing up inflation pressures and keeping central banks from declaring a decisive victory over inflation," Jeffrey says.

That said, Schwab doesn't expect increased demand from China to drive the type of inflation that characterized the early pandemic. That variety of inflation came from supply-chain disruptions and excess demand for goods. "Since that time," says Kevin Gordon, senior investment strategist at Schwab, "inventories have increased at a faster pace relative to sales. It essentially means that businesses have more 'stuff' available when consumers want it."

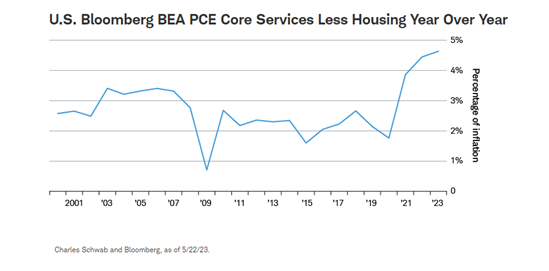

Right now, the Fed is more concerned with a measure known as Personal Consumption Expenditures (PCE) core services ex-housing, which strips out anything commodity-, housing-, and goods-related. Fed Chairman Jerome Powell and other officials believe this metric, which includes services like restaurant meals and hotel stays, has the tightest relationship to wage growth. It's also less influenced by China.

If the Fed keeps its focus on PCE core services ex-housing, U.S. wages could have a bigger impact on Fed decision-making later this year than a Chinese rebound. Still, Kevin agrees China's recovery could slightly increase inflation in the U.S., likely via commodity prices that elevate the price of goods.

"A turn higher in goods inflation—and a failure of core services inflation to ease—would likely compel the Fed to either raise rates by more than expected or keep them higher for longer than expected," Kevin says.

This brings us to a threat China's rebound does face: Current lofty U.S. and European interest rates could slow Western economic growth, reducing demand for Chinese goods.

"Weakness in the U.S. and elsewhere is acting as a drag on Chinese exports," Jeffrey notes. China is a major producer of commodities, including materials used in consumer products like electric car batteries. A recession in the United States and Europe that reduces demand for expensive products like EVs might reverberate in China's economy.

The United States imported $536.7 billion in goods from China last year, up about 6% from 2021, according to the U.S. Census Bureau. But U.S. imports of Chinese goods fell 35% in March from the same month a year earlier and have been down every month so far in 2023. The United States is the biggest importer of Chinese goods, so this downturn bears watching.

Still, with China's economic engine potentially revving again soon, Jeffrey thinks investors should look beyond the United States and Europe.

"We believe a broad exposure to emerging markets—including China, the largest weight in many emerging-market indexes—deserves a small allocation in portfolios, acknowledging both the potential opportunity and possibility of higher volatility than developed market stocks," Jeffrey says.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Fixed-income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower-rated securities are subject to greater credit risk, default risk, and liquidity risk.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, and illiquid and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Diversification and asset allocation strategies do not ensure a profit and do not protect against losses in declining markets.

Investing involves risks, including loss of principal.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab