After falling into its own recession last year, the housing market has started to turn decisively higher; but a sustained recovery might not be the strongest elixir for the economy.

One of our central theses for the better part of the past year is that the economy has been plagued by rolling recessions—bouts of weakness that weren't powerful enough to bring the entire economy down (courtesy of offsetting pockets of strength). As shown in the chart below, the first sector of the economy to fall into its own recession was housing. Proxied by the National Association of Homebuilders (NAHB) index, housing took a deep dive throughout 2021 and 2022 but has since started to show signs of life.

Given this report focuses on the housing market, we'll opine on the other indicators in the future; but the key to watch for are signs of life in confidence metrics and the manufacturing sector. A sustained turn higher would confirm the transition from rolling recessions into rolling recoveries, but it's too soon to make that determination.

The latest move higher in homebuilder sentiment had healthy breadth given that all of the index's components moved higher, led by the gain in expectations for single-family home sales in this year's second half. The optimism was also widespread throughout the country. The monthly report showed that optimism was due to improving supply chains and the low level of existing home inventory. The one rub was the citing of credit conditions, which have tightened notably and could crimp future growth.

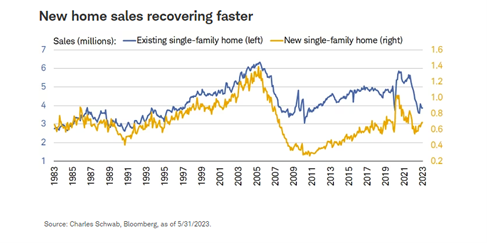

Given homebuilder sentiment is one of the leading economic indicators, one would expect a material turn higher in home sales to follow the recent return of optimism. That has happened to some extent, but not evenly. As you can see in the chart below, sales for both existing and new homes have bounced off their recent troughs, but the strength has been more pronounced in the new home market (caveat: this report was published before the release of May new home sales data). Not only did new home sales find their recent trough sooner (last July), but they're up by 26% (through April) since then. Existing home sales are up by a weaker 7% (through May) since their trough in January.

The split between the new and existing home market can be attributed to several factors, not least being the different supply backdrops. The new home supply came back online with gusto after the pandemic decline, while the existing home supply has failed to catch up. In addition, many existing homeowners are locked into low fixed-rate mortgages, resulting in a diminished incentive to move.

With demand for homes still relatively strong, some buyers in the existing market have been pushed into the new market. As many homebuilders have been offering incentives like premium finishes, mortgage rate buydowns, and other concessions, the process has looked relatively more attractive for buyers. Plus, high mortgage rates are not yet scarring the process, given that all-cash deals are still around.

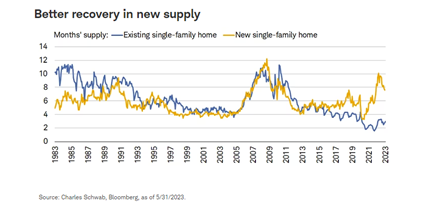

You can see in the chart below that there is a stark difference in monthly supply metrics As of May, existing monthly supply stood at three—meaning it would take only three months to sell every home currently on the market at the current sales pace. That has kept buyers in the existing market in an increasingly tough position, forcing them to explore new construction.

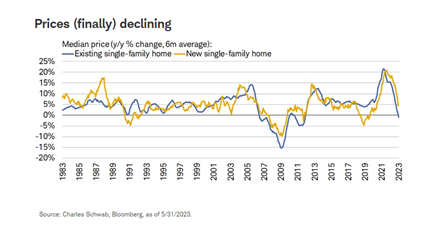

Some relief has crept in via the decline in home prices. As shown in the chart below, the six-month average of the year-over-year change in existing single-family home prices has dipped into negative territory. The modest drop is a relief for now (given price growth surged into double-digit territory a couple of years ago), but the key to watch is whether declines get more severe moving forward. Relatively robust demand in the new-home market would argue against that as of now, but the existing home market is not yet out of the woods.

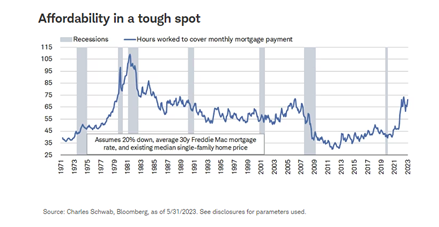

Unfortunately, the decline in home prices hasn't been enough to counteract other headwinds that are facing would-be buyers. Individuals and/or families in the market for a house are facing some of the worst affordability dynamics in over a decade. The chart below shows how many hours one needs to work to cover a monthly mortgage payment (assuming the parameters shown in the chart). We were starting to see some relief as mortgage rates eased at the beginning of the year, but that has vanished of late.

Hopeful signs of disinflation

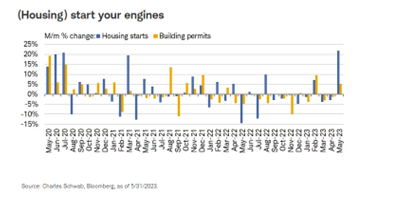

The standout housing data point for May was housing starts, which surged 22% month-over-month; a historic feat given there have only been 15 months since 1959 with gains larger than 20%. It was the eighth-largest monthly gain on record, likely aided by unusually warm and dry weather throughout most of the country last month.

The rub is that we can't glean a ton from that burst in activity. Some of the strongest jumps throughout history have been during both recessions and expansions (notably, the largest gain of 29% was in the midst of the recession that started in 1981). Previous spikes of similar magnitude were generally followed by at least some reversal in the subsequent few months, so keep that in mind near-term.

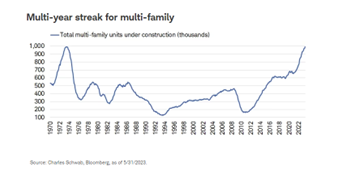

To be sure, any indication of a "cleansing" of the housing pipeline (more completions to catch up with units under construction) would be welcome for the housing shortage. One of the bittersweet aspects of the housing starts and building permits data has been construction activity in the multi-family (i.e., apartment) space. As shown in the chart below, the number of multi-family units under construction has reached its all-time high, with the prior high being all the way back in 1973. The bitter part is that completions have lagged behind; the sweet part is that this will eventually be a disinflationary force, providing relief to those who choose the rental market.

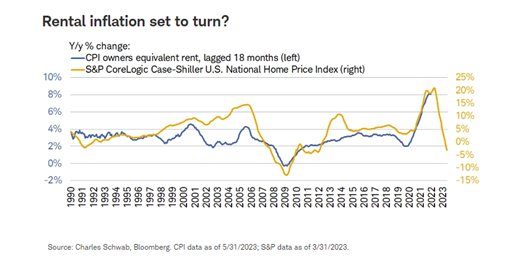

The home price decline underway bodes well for the future path of inflation. As you can in the chart below, the swift move lower (into contraction) in national home price growth (proxied by the all-encompassing S&P CoreLogic Case-Shiller Index) seems to indicate that the owners' equivalent rent (OER) portion of the consumer price index (CPI) is set to roll over. While history suggests that is the case, and we think the relationship will hold, we'd caution against assuming that this holds perfectly (in terms of the magnitude of the decline or the timing of its start).

As a reminder, OER is an imputed metric; it isn't measuring actual rents but is asking homeowners what they think they can charge to rent their current residence. Unsurprisingly, that goes up when home prices go up. The component has received a lot of criticism for inaccurately representing rental inflation, which is one of the reasons the Federal Reserve is currently excluding it from its core inflation analysis.

In sum

Some recovery in housing data is a welcome addition to this unique cycle landscape. There are ripple effects of course; however, residential investment is only 2.5% of gross domestic product (GDP), so it's unlikely to be anything resembling a full elixir for what ails the economy. However, residential investment appears to be on track to be flat to slightly better in the second quarter, after two years of significant weakness.

We do not expect a significant decline in mortgage rates, even if the Federal Reserve is getting close to ending its rate-hiking cycle. Even if mortgage rates begin to decline and housing continues to improve, it doesn't keep a formal recession at bay. Case in point: 2001, when (like at present) non-residential (business) investment was where weakness was concentrated. Perhaps the brightest spot will be the much-needed aid to still-high inflation, given the home-price decline underway. We'll take disinflationary forces anywhere we can get them.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Supporting documentation for any claims or statistical information is available upon request.

The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Investing involves risk including loss of principal.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

The information provided here is for general informational purposes only and is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific advice is necessary or appropriate, consult with a qualified tax advisor, CPA, financial planner, or investment manager.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

S&P CoreLogic Case-Shiller U.S. National Home Price Index tracks the value of single-family housing within the United States. The index is a composite of single-family home price indices for the nine U.S. Census divisions.

Parameters used for "Affordability in a tough spot" chart: existing one-family home sales median price from National Association of Realtors ($401.1k as of 5/31/2023), U.S. average hourly earnings of production and nonsupervisory workers (28.71 as of 5/31/2023), Freddie Mac U.S. Mortgage Market Survey 30-year Homeowner Commitment National (6.76% as of 5/31/2023).

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Charles Schwab

Read more commentaries by Charles Schwab