Get the Balance Right

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe recent broadening out in market breadth has been accompanied by frothier investor sentiment, but using sentiment as a market-timing tool is tricky (if not impossible).

It's been 285 days since the S&P 500®'s bear-market low on October 12, 2022; since then, the index is up nearly 27%. The Nasdaq has trumped that with a 37% return since its low on December 28, 2022. There were three characteristics in play last October that provided the "set up" for the S&P 500's rally that's ensued: dour investor sentiment, oversold indexes, and positive breadth divergences. In terms of the latter, you may recall that at the October low, the S&P 500 Index had taken out its mid-June 2022 low. However, the breadth under the surface was improving.

Fast-forward to the present, investors are not getting served the trifecta of last October. Although breadth has been improving relative to the extreme concentration that characterized the market through May this year, investor sentiment is at best complacent, and at worst, frothy; and the market is clearly not oversold.

Taking a closer look at the market's health via breadth statistics, it's clear that conditions have mostly improved over the past couple of months. At a broad level, the S&P 500 is faring better than its peer indexes (the Nasdaq and Russell 2000), but the good news is that participation started to broaden in June.

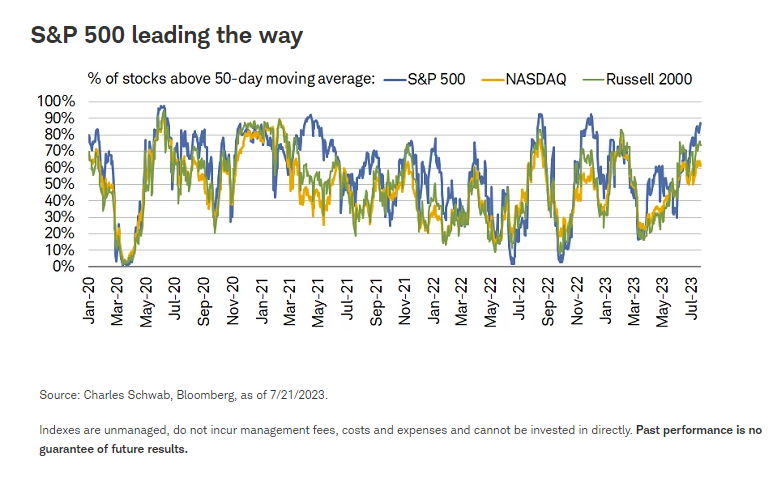

As shown in the chart below, nearly 90% of S&P 500 members are trading above their 50-day moving average, which is the highest since the end of 2022 and close to the 90% threshold that has historically been key in confirming uptrends (note: the index cleared that level in June 2022 but it was a failed signal). The Russell 2000 isn't too far behind, but the Nasdaq is taking longer to catch up (still far from its peak earlier this year).

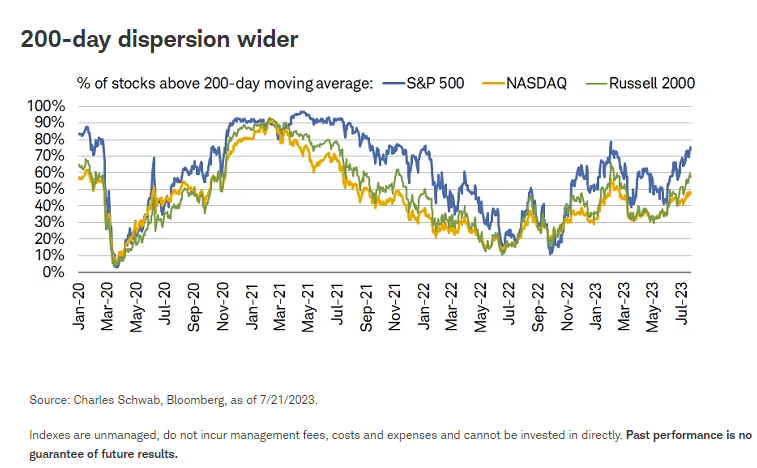

The story looks similar for the percentage of S&P 500 members trading above their 200-day moving average. You can see that although the index hasn't cleared its recent peak, it has steadily climbed over the past month. It's an important development given our late-May concerns about the lack of participation from the "average stock," even as the headline indexes continued to climb to new 52-week highs (save for the Russell 2000, which is still stuck in a range).

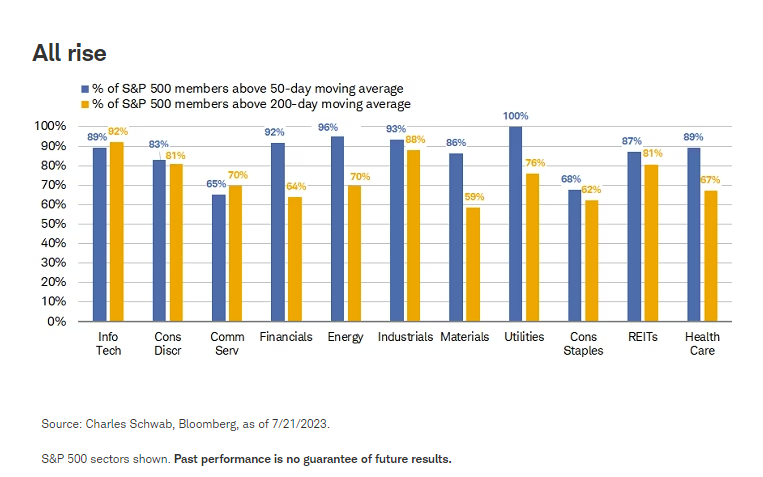

At the sector level, things are also looking up, given every S&P 500 sector has more than half of its members trading above both their 50- and 200-day moving averages. For a good chunk of 2023, the technology sector had been leading the charge for both metrics and while some of the strength has eased of late, the sector still looks relatively healthy. Overlooked, in our opinion, has been equal (if not more impressive) strength in other sectors, such as industrials. It's a reminder that, despite tech grabbing headlines most of the time, other sectors can exhibit strong qualities—namely, the quality-oriented factors we have been encouraging investors to screen for positive earnings revisions/surprises, strong free cash flow, healthy profit margins, strong balance sheet, etc. One development worth watching is the recent climb for the classically defensive utilities sector, which is outpacing all sectors in terms of 50-day breadth.

A new bull?

With major, large-cap indexes like the S&P 500 inching closer to new all-time highs, the debate has continued to heat up as to whether it's a new bull market or simply a bear market rally. In contrast to recessions, there isn't some concrete, widely adopted definition for new bull markets. Some view it as any 20% advance from a trough, while others believe the prior peak for the market must be surpassed. Given the former has been satisfied but the latter hasn't, both bull and bear camps have something to hang their hats on.

We think of cycles more broadly and over a longer-term time frame. There is a case to be made that a new secular bull market began in 2009, following the Global Financial Crisis. If that's the case, both the brief pandemic bear market in 2020 and the 2022 bear market would be considered cyclical bears within a secular bull. But, that doesn't mean the market is out of the woods.

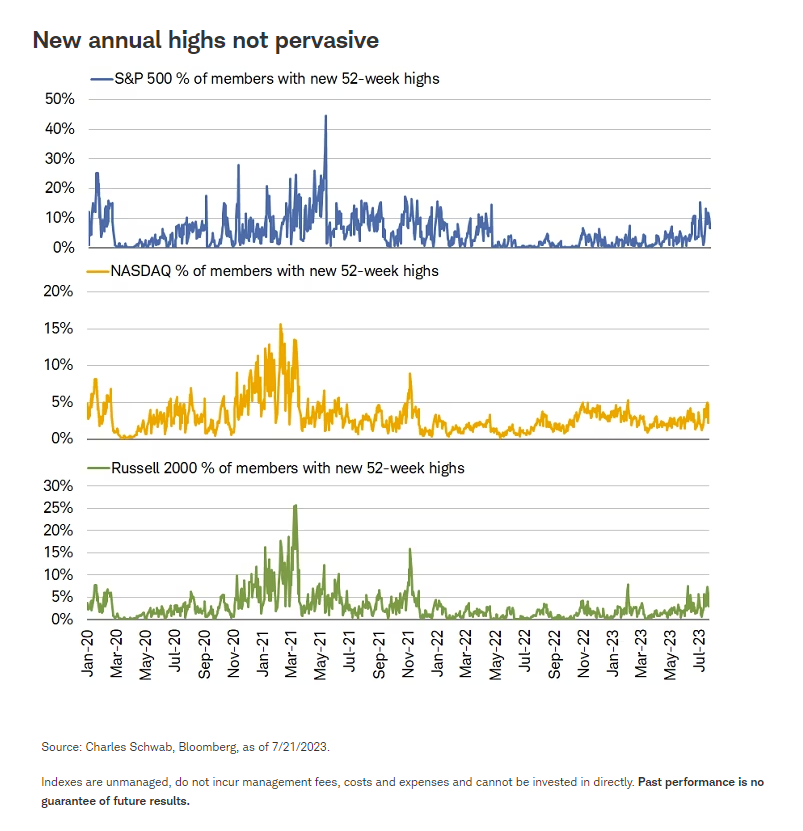

Objectively, the strength of the rally at the headline index level hasn't trickled down to the member level. Shown in the chart below are the percentage of members in the S&P 500, Nasdaq, and Russell 2000 making new 52-week highs. Fortunately for the S&P 500, the percentage finally breached double-digit territory in June. That hasn't yet happened for the other two indexes, despite some healthier advances at the headline level.

This data has become increasingly crucial in today's environment, given it's more than nine months off of a major market low. Historically, at this point, the major indexes were generally well into double digits in terms of performance, which can be clearly seen in the most recent bull stretch that started in March 2020 and saw a 52-week breadth improve sharply in November 2020.

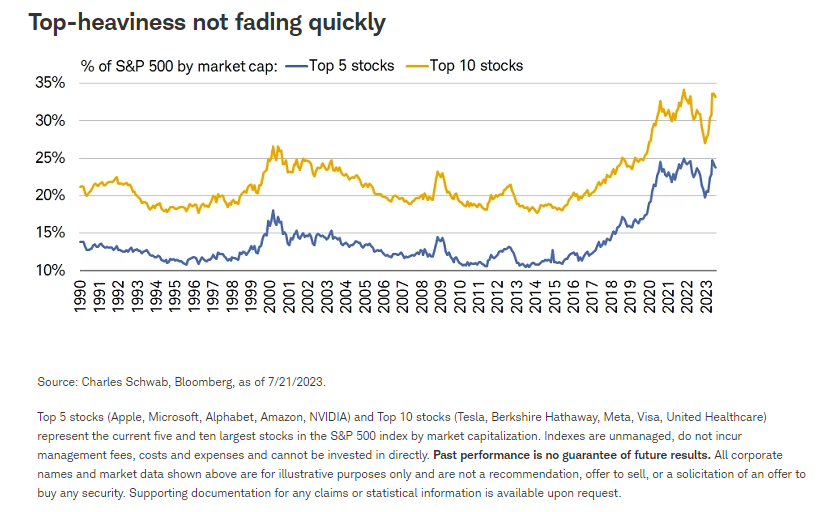

Admittedly, one of the main reasons the rest of the market hasn't "needed" to catch up in making new highs is that the largest players have been driving performance this year. That started to change in June as the market began to broaden. Yet, even with the average stock doing more of the market's legwork, the five largest stocks in the S&P 500 still represent 24% of the index's market value. For the 10 largest stocks, the share is 33%, only slightly down from the peak of 34% in May, as shown in the chart below.

Investors viewing these data points through a negative lens will often point to concentration as a reason for the market to turn lower, but we don't see that as strong evidence—in and of itself—to be negative. To be sure, the largest companies' market value share doesn't match up with their earnings share, which makes their weight harder to justify. However, they aren't low-quality, speculative names (which is a notable difference from prior periods of heavy contraction). Not only that, one major driver of their gains this year was the banking stress in March, which caused a (mostly) justifiable rush into large caps at the expense of small caps (particularly, financials).

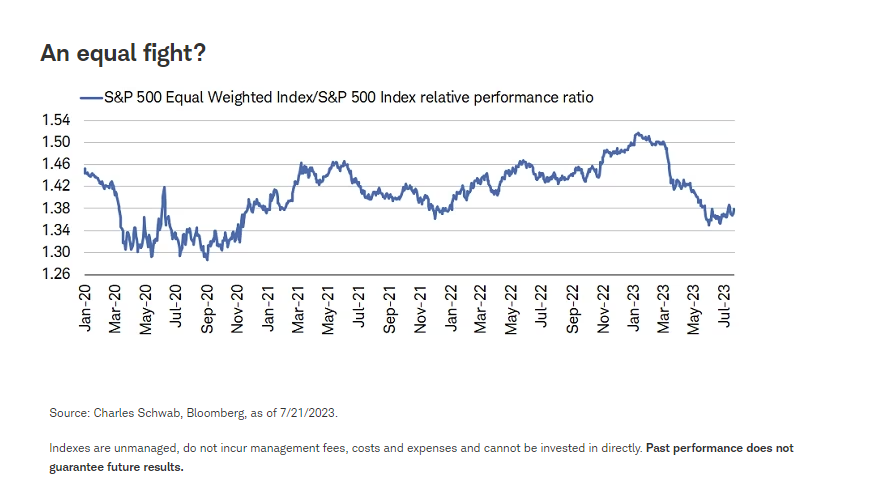

That swift move was seen most clearly in the ratio between the equal-weighted and capitalization-weighted S&P 500 indexes. The former—which assigns equal weight to every member, thus stripping out the effects of mega-cap dominance—failed to keep pace with the latter at a dramatic pace starting in March. As that continued throughout the first half of the year, relative outperformance from the prior couple of years was wiped out. In fact, the magnitude of the move was similar to that seen during the bear market plunge in early 2020 (obviously, the circumstances were different this time). As noted in our midyear outlook, we continue to look for the equal-weighted index to regain its relative footing. That would underscore better participation from the average stock and help bolster the rally.

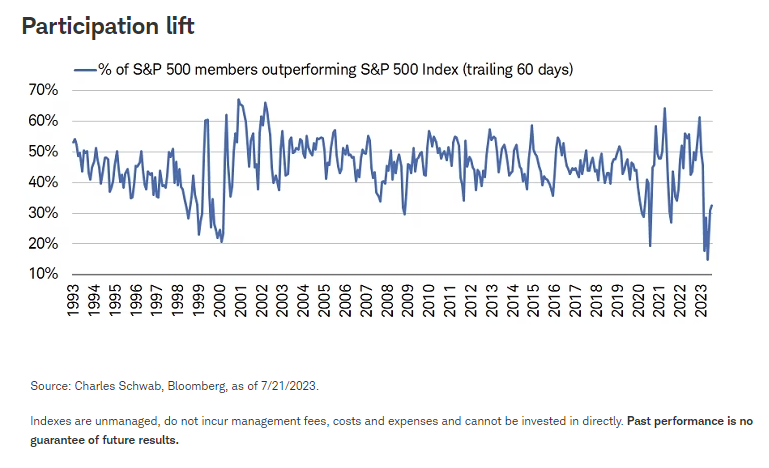

Another development we're on the lookout for is the share of members outperforming the headline index. As shown in the chart below, by the end of May, the lowest share of members (15%) in at least several decades was beating the S&P 500 over the prior 60 days. As of the market's close on July 21st, 32% of members were outpacing the index over the prior 60 days. While that is still below the long-term average, it's a marked improvement from just two months ago. This was a fact that was missed in analyses that suggested nothing was wrong with a handful of stocks driving gains this year. It wasn't just an issue that the mega caps were outperforming, it was that the rest of the market was underperforming by a significant degree.

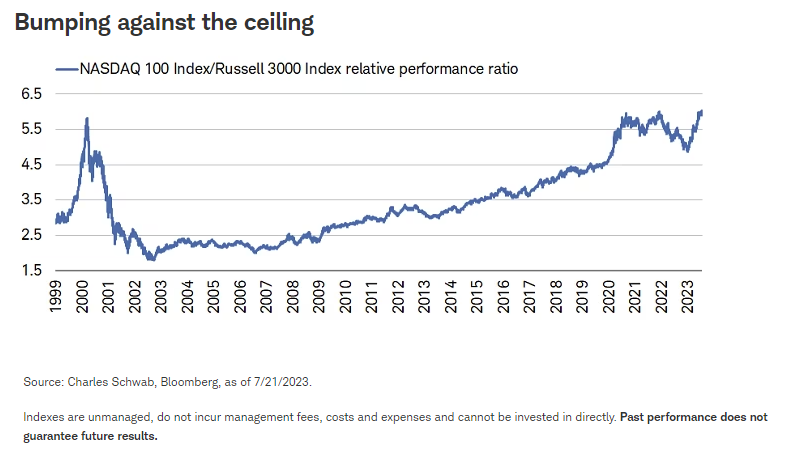

The recent turn higher in cyclical segments of the market, and simultaneous weakness in areas like tech, are consistent with better performance under the market's surface. One way to gauge if leadership is in fact shifting away from mega-cap dominance is via the relationship between the Nasdaq 100 (the proxy for "big tech") and the Russell 3000 (the proxy for "the market"). As shown in the chart below, the ratio of the two indexes is back to where it was in November 2021 and September 2020, with the recent leg higher sharply reversing the trend put in place last year—favoring the Nasdaq 100 at the expense of the Russell 3000.

One near-term potential source of volatility for the Nasdaq 100 may be the special rebalance the index is undergoing today. Conducted only twice in history—in December 1998 and May 2011—Nasdaq announced earlier this month that the index will undergo a special rebalance given the weights and heavy concentration of the largest constituents. The trigger is pulled whenever the weightings of all stocks with more than 4.5% of market capitalization individually top 48% collectively.

Market impact after the prior two rebalances

Per our friends at Bespoke Investment Group (BIG), the 1998 adjustment was driven by the adoption of the 4.5%/48% criteria described above, coming during the late 1990s internet-bubble-fueled tech rally. Microsoft, at that time, was more than 25% of the index. The 2011 adjustment was much more widespread, with 82 individual stocks adjusting down in weighting.

Subsequent performance was starkly different. In 1998, and after its December rebalance that year, the Nasdaq 100 was soaring, up 13% a month later, 20% three months later, 29% six months later, and 112% a year later. After the May 2011 rebalance, the index was actually down over the next one, three, and six months, but was back in positive territory to the tune of 9% a year later.

Concentrated rallies this year pushed the largest Nasdaq 100 stocks' collective weight to more than 55% of the index as of July 3rd (the reference date by the Nasdaq)—in conflict with the 48% concentration limit in the index's methodology. The target of the rebalance is no more than 40%, with the target weights among the largest constituents estimated as follows:

- Microsoft: 10.06% (from 12.8% on July 3rd)

- Apple: 9.79% (from 12.45% on July 3rd)

- NVIDIA: 5.46% (from 6.95% on July 3rd)

- Alphabet (Google) 5.76% (from 7.33% on July 3rd)

- Amazon: 5.37% (from 6.83% on July 3rd)

- Tesla: 3.56% (from 4.53% on July 3rd)

Per Bloomberg, the special rebalance is "intended to prevent fund managers linked or benchmarked to the index from violating a Securities and Exchange Commission (SEC) diversification rule." Interestingly, per a Birinyi Associates analysis, if the new Nasdaq 100 weights were in place at the beginning of this year, the new version of the index would have had similar returns: +44.8% for the old version and +46.9% for the new version (year-to-date as of July 18th).

In sum

A broadening out in terms of market breadth, all else equal, is a good thing. Unfortunately, the significant underperformance of equal-weighted indexes relative to capitalization-weighted indexes did not solve the valuation conundrum. The rally off last October's low was all accounted for by multiple expansions, with no lift coming from the denominator (E) in the price-earnings (P/E) equation.

That said, sentiment can remain frothy, markets can remain overbought, and valuations can remain stretched, for extended periods. Market timing is a tricky (if not impossible) exercise, which is why we don't try to pick tops and bottoms—and certainly never advise investors to either "get in" or "get out." As we always say, neither "get in" nor "get out" are investment strategies—they simply represent gambling on moments in time. Investing should always be a disciplined process over time, which should include periodic rebalancing. Nasdaq is doing just that.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistics.

Small-cap investments are subject to greater volatility than those in other asset categories.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Rebalancing does not protect against losses or guarantee that an investor’s goal will be met.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All