Should Muni Investors Take Note of California?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDuring the past decade, a turnaround in the Golden State has resulted in higher credit quality for many issuers.

Shortly after the 2008 credit crisis, a concern that we heard from many clients was, "Is the state of California likely to declare bankruptcy?" The answer was no for myriad reasons, but it illustrates the situation that the state's finances were in. That's no longer the case.

The turnaround in the Golden State has resulted in higher credit quality for many issuers in the state. As a result, we believe California municipal bond investors may want to consider a portfolio of all-California munis. And it isn't just California investors that should take note—because the state is the largest issuer of municipal bonds, so many mutual funds, exchange-traded funds (ETFs), or other investment options hold California municipal bonds. Here are a few things investors should know now:

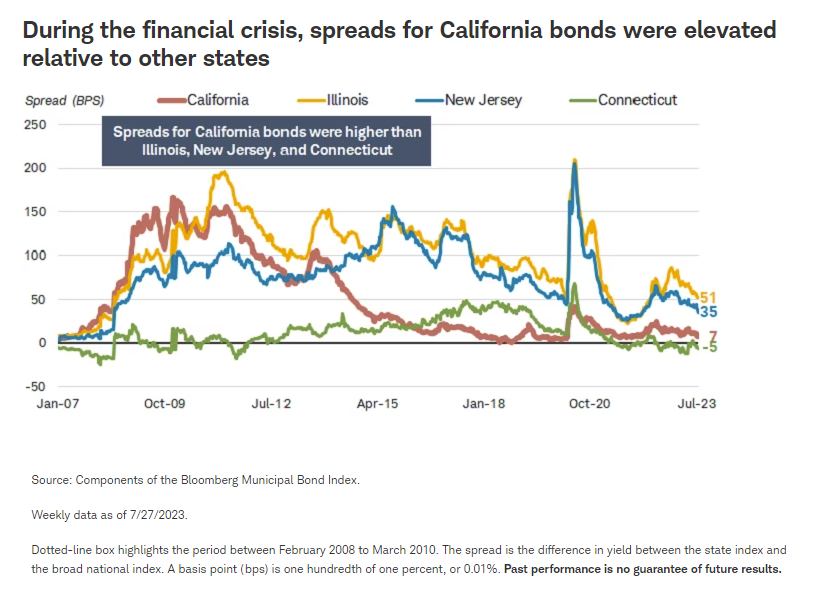

1. The state has turned its financial position around since the 2007-2008 financial crisis. Following the 2008 financial crisis, the state's general obligation (GO) bonds were the lowest-rated of any state.1 Politically, the state needed a two-thirds majority to pass a budget, which led to cash-flow challenges. Additionally, the rainy-day fund was depleted and real estate construction and values in many areas experienced a dramatic bubble, then collapsed. Spreads—that is, the difference in yields, which are a measure of perceived risk—for a broad index of California muni bonds were higher than for other financially stressed states like New Jersey, Connecticut, and Illinois. At one point, spreads were close to those of bonds issued by Puerto Rico, which is now going through a major debt restructuring.

The situation has since improved. Since the 2007-2008 financial crisis, the state has successfully passed measures to reduce the votes needed to pass a budget to a simple majority, which has helped to manage cash flows. Meanwhile, the economy has since improved and tax revenues have increased substantially, which has allowed the state to build up its reserves to record-level highs.

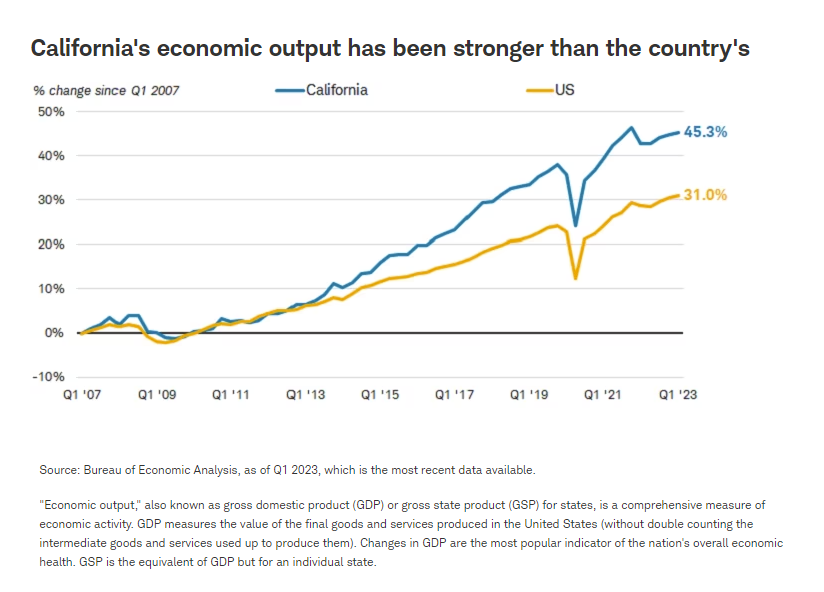

With roughly 12% of the U.S. population and a very diverse economy, California has benefited from the national economic recovery. The year-over-year change in the state's economic output has surpassed that of the nation in 41 of the past 50 quarters since 2010, according to the Bureau of Economic Analysis. The state has also taken measures to pay down billions of dollars of debts incurred during the credit crisis and to build up its rainy-day fund. As a result, the state has steadily built up its reserves to nearly 17% of general fund revenues, according to Moody's Investors Service.

2. Despite the turnaround, the state faces headwinds. However, all is not gold in the Golden State, and the shine in the state's finances may begin to tarnish. In late June, California's Governor Gavin Newsom signed a budget with a $31.5 billion deficit due to an unanticipated decline in tax revenues. The state is obligated to balance its budget so to close the gap, the state is using spending cuts, payment delays, and other budget tactics to cover it. It isn't defaulting on debt service, nor do we expect it to do so. Also notable is that it isn't tapping into its reserves, which bodes well for the future.

Unlike other states, California relies heavily on individual and business income taxes, which results in revenues that are more volatile than in other states because those two sources are generally closely linked to economic activity. In fact, "the top 1% of taxpayers contributed 49% of total personal income tax in calendar 2020" according to Standard and Poor's. The state gets approximately 72% of its tax revenues from these two sources. That's the third-largest dependency among all states. Other states have a greater reliance on sales, property, and other tax revenues, for example. Going forward, if the economy slows or the stock market declines, it could further hurt revenues.

Although the state has experienced a decline in revenues, this is coming off the back of multiple years of strong revenue growth. For California, the current situation is unlike the 2007-2008 credit crisis. Then, the state's available liquidity—which is akin to the state's savings account—was declining and was less than 5% of annual general fund revenue. Now, the state's available liquidity has been increasing and is almost 70% of general fund revenues. According to The Pew Charitable Trusts, the state could run off of reserves alone for roughly two months. That's one of the highest liquidity positions relative to other states.

3. California investors in a low state tax bracket may want to consider munis from other states, too. The improvement in the state's finances has in part contributed to lower spreads for California bonds. A spread is an additional yield above a highly rated index or bond, such as a Treasury bond or generic AAA-rated muni, to compensate investors for the increased risks.2 Spreads for a broad index of California bonds have been steadily decreasing since the 2008 credit crisis, to the point where yields for an index of California bonds are close to that of an AAA-rated index, as shown in the chart below. Because the state is rated lower than AAA—at Aa2 by Moody's and AA- by Standard & Poor's—investors are taking on lower-rated debt with a relatively small pickup in compensation from yield. As a result, California investors who are in a low in-state tax bracket should consider bonds from outside California as a complement to their existing holdings. Due to low spreads for bonds issued by California entities, it could be possible to achieve higher after-tax yields with out-of-state munis even after accounting for the tax differences. That's not to say that investors in lower state tax brackets should avoid California munis, but that they may be able to achieve higher yields after taxes and greater diversification by adding some munis from outside California.

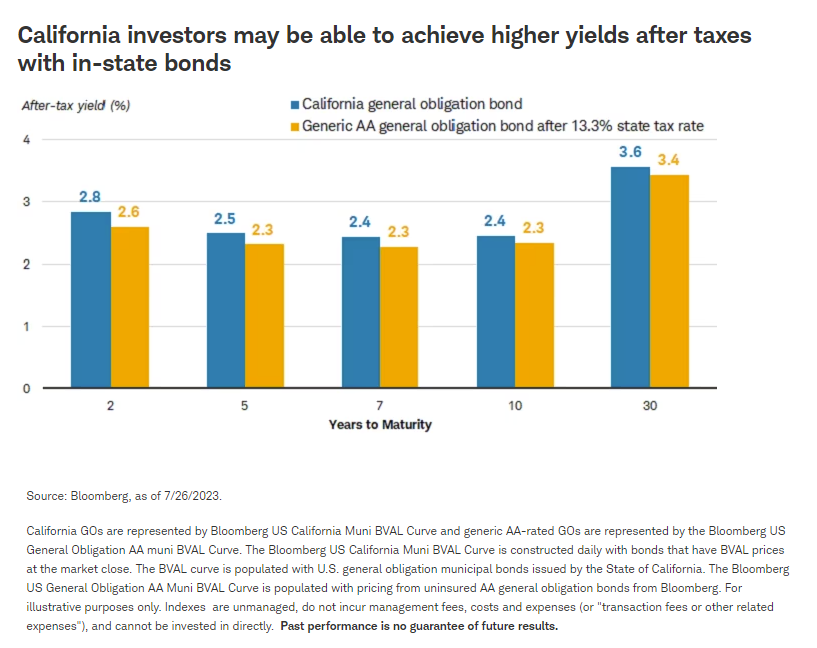

4. California investors in a high state tax bracket will likely benefit from staying in the state. Even though spreads are very tight, California investors in the state's top tax brackets may still achieve higher after-tax yields by sticking with in-state munis. For example, the chart below shows the yield on an index of 10-year California GO bonds compared to an index of 10-year generic AA-rated national GO bonds. The national GO index has been adjusted lower to account for the impact of paying the top California state tax rate of 13.3%. In all instances in this example, the California GO bond yields more than the out-of-state GO bond after the impact of taxes.

In particular, investors who are staying in the state may want to consider California GO bonds and local school district GO bonds, as we think they will be the most positively affected by the state's economic recovery. Higher revenues will give the state more flexibility to meet its debt service. State GO bonds are supported by a dedicated pledge by the state and are second only to education funding in terms of priority of payments from the state's general fund. However, if the economy slows or the stock market declines, revenues for the state may suffer.

In our opinion, local school district GO bonds should also benefit from their solid tax backing. Local school district bonds are generally secured by an unlimited and dedicated property tax pledge. They generally also have strong oversight. The underlying economics and characteristics of the district's tax bases will vary widely, though and a decline in property values could be a risk over the longer term. In our opinion, districts with a larger and wealthier tax base will generally have stronger tax bases available to pay debt service.

What to do now

The turnaround for the state of California over the past 15 years has been rather remarkable and has put the state's finances in a good position. However, there are headwinds such as a slowing economy, a decline in the stock market, or the state exhibiting a lack of fiscal discipline in the future even though it hasn't done so recently. Additionally, since the COVID-19 crisis, the state has started to experience outmigration. We don't believe this poses a near-term risk, as demographic issues take many years to develop, but it is something worth watching.

Despite the headwinds, we believe that many muni investors should consider California municipal bonds. Schwab clients can log in to research individual municipal bonds and view pre-screened municipal bond exchange-traded funds (ETFs) on Schwab's ETF Select List® or municipal bond mutual funds on Schwab's Mutual Fund OneSource Select List®. For additional help in selecting an appropriate solution for your needs, a Schwab financial consultant or fixed-income specialist can help.

1 Standard and Poor's, "History of U.S. Ratings," as of 7/21/2023.

2 The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

Investors should consider carefully information contained in the prospectus, or if available, the summary prospectus, including investment objectives, risks, charges, and expenses. You can request a prospectus by calling 800-435-4000. Please read the prospectus carefully before investing.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. The examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve. Supporting documentation for any claims or statistical information is available upon request.

Schwab does not provide tax advice. Clients should consult a professional tax advisor for their tax advice needs.

Investing involves risk including loss of principal.

Past performance is no guarantee of future results.

Fixed-income securities are subject to increased loss of principal during periods of rising interest rates. Fixed-income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

The information provided here is for general informational purposes only and is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific advice is necessary or appropriate, consult with a qualified tax advisor, CPA, financial planner, or investment manager.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

Diversification strategies do not ensure a profit and cannot protect against losses in a declining market.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approve or endorses this material, guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All