Don't Let Me Down: An Earnings Season Update

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWith nearly 85% of S&P 500® companies having reported results for second-quarter earnings season (as of August 4th), it's time for an update on how the profits picture has unfolded thus far—as well as a peek into what expectations are for the back half of the year. The simplest way to sum up performance in the second quarter is "mixed." On the one hand, earnings are contracting, revenue growth is virtually flat, and guidance has weakened. On the other hand, the beat rate has climbed, earnings estimates are up from their worst points, and the percentage by which companies are beating estimates has moved higher (all to be explained below).

On the right path?

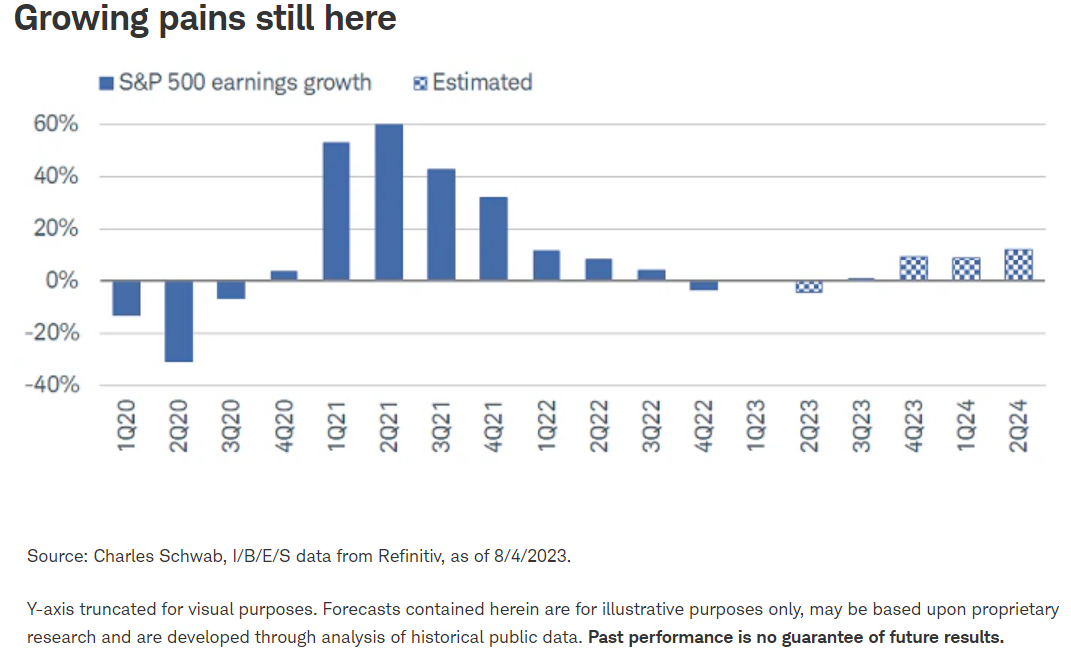

Starting with a broad overview, you can see in the chart below that the "blended" estimate for earnings growth—which combines results from companies that have already reported with estimates for those that have yet to report—is in negative territory. At -4.2% year-over-year, it's the worst decline since the third quarter of 2020 and is sandwiched between a zero-growth quarter (the first quarter of this year) and what is expected to be a rebound into positive territory (starting in the third quarter).

Putting results under the microscope yields an interesting reason as to why growth is negative for the quarter. As you can see in the table below, the drag is entirely due to the energy sector. You can see that if one were to exclude energy's -41.2% contraction, the S&P 500's earnings growth rate jumps to 2%. This dynamic won't last in perpetuity, but energy will face tougher base effects in the near future, given the sector's profits were growing by triple-digit percentage points this time last year (which had the opposite effect of boosting the overall market's earnings).

Worth pointing out is that earnings growth is expected to rebound at a steep pace in the back half of this year, then climb to a double-digit pace into 2024. In the face of leading indicators that continue to weaken, tightening lending standards, and the climb in interest rates, it seems rather lofty (for now) to assume that growth will hold at that pace. Plus, we like to consistently remind investors that estimates further out should be taken with several grains of salt. A year ago, the consensus estimate for earnings in the second quarter of 2023 was nearly 11%; that has clearly been chopped considerably.

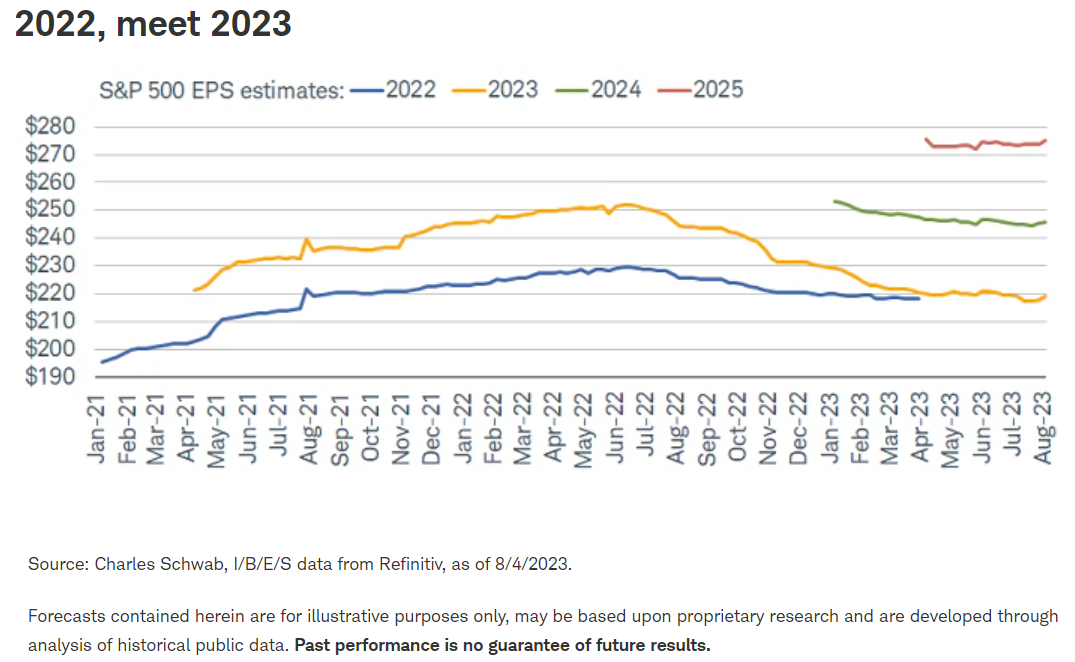

You can see that chopping-down process more clearly in the next chart, which plots out the path of estimates over time for this year. At certain points last year, analysts had expected first- and second-quarter earnings growth to jump above 12%. Yet, earnings didn't grow at all in the first quarter (the blue line) and they are contracting in the second quarter (the yellow line). Not only that, but despite the expectation for stronger results in the third quarter, estimates have continued to move down.

One development worth watching is if the "hook" pattern seen year-to-date continues. Even though there was no earnings growth in the first quarter, that was a significant improvement from the low point, which had baked in a nearly 5% decline. Admittedly, analysts lowered the bar too far, too fast at the beginning of the year, which made results look less terrible. You can see earnings starting to replay that pattern in the second quarter, but given reporting season is close to wrapping up, it would take a heavy lift from a small number of companies to get earnings back to breaking even.

The hook in the first quarter is virtually the entire reason that earnings estimates for the full year have stabilized. Shown in the chart below are dollar estimates for the S&P 500, broken down by year. With the yellow and blue lines right near the $220 level, the expectation (as of now) is that earnings will see almost no growth this year compared to last year. Yet, as we alluded to earlier, the expectation is for a miraculous jump in growth as we enter 2024 (the green line). Again, we'd be careful in extrapolating for several reasons, not least being some notable cuts to guidance of late.

Better-than-expected doesn't cut it

There has been a lot of enthusiasm stemming from the impressive beat rate this season, given nearly 80% of companies have reported earnings results above analysts' expectations (the highest since the third quarter of 2021). Additionally, as you can see below, the percentage by which companies are beating (shown via the yellow line) has jumped to 7.7%, which is also the highest since the third quarter of 2021. Undoubtedly, both are great statistics for which to cheer, but we would encourage investors to look at growth and revisions, since it's easy to clear a low bar if analysts drop it significantly—which was the case starting last quarter.

As such, you can see that there has been much less enthusiasm for the market when looking at revisions. The number of negative revisions has outpaced the number of positive revisions for the past six weeks, the longest streak since the end of 2022 into 2023. To be sure, the spread is less severe this time around. That, along with the fact that we have seen some notable pops higher (like in early June), suggests that the direst expectations are being rescinded.

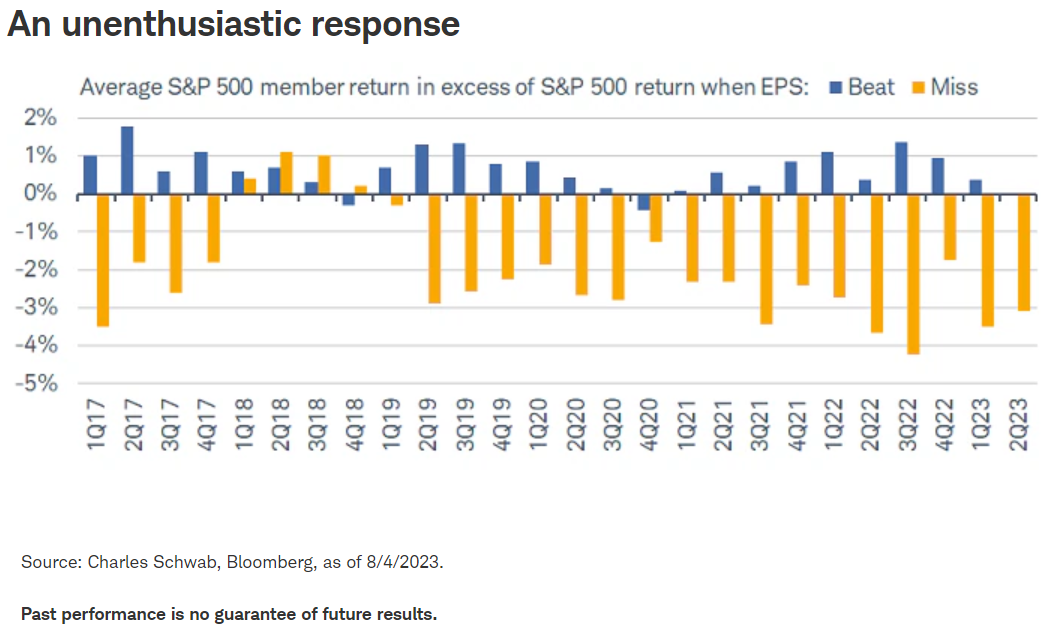

The chief reason we'd look to revisions and actual growth results (as opposed to the beat rate) is because companies' stock prices haven't been rewarded for outpacing analysts' estimates. The chart below plots out the average S&P 500 member's return in excess of the broader market's return when earnings beat and miss expectations. Conventional wisdom says a company should outperform when beating estimates, which has been the case most of the time. Yet, this quarter, there has been zero outperformance despite some notable earnings beats, making this (so far) the worst quarter for the average S&P 500 member's reaction since the fourth quarter of 2020. We view this as the market both having fully priced in better results and putting more emphasis on what guidance companies are giving.

In sum

There's something for everyone in earnings results for the second quarter. Our main takeaway is that the market is (rightfully) growing stricter in its assessment of companies' forward guidance, which is crucial given inflation-adjusted revenue growth for the broader economy is now contracting. As we turn to the second half of the year, earnings have to step up to the plate to justify the market's strong run, especially because the entire rally since the trough last October has been driven by multiple (price-to-earnings ratio, or P/E) expansion. It is true that multiples tend to rebound before earnings; but it's also true that for a rally to be sustainable, earnings need to start showing material signs of strength and contributing to the upside.

We are approaching critical moments of truth for the economy in the back half of the year. If earnings and revenue growth hold up (and rebound) as monetary policy continues to tighten and cracks in the labor market remain, resilience will have taken on a new, stronger meaning. For now, though, we're not yet out of the woods.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All