Vertigo: Market Succumbs to Myriad Pressures

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWith the path of least resistance for stocks seemingly lower for now, the key to watch will be a stabilization in interest rate volatility and clarity on the path of monetary policy.

As many readers know, I (Liz Ann) started in this business 37 years ago and worked for the late, great Marty Zweig for 13 years. He operated his hedge fund/money management/newsletter business with 17 "trading rules." Number one on the list: "The trend is your friend; don't fight the tape." Number six: "Don't fight the Fed." One of my favorites has always been his 17th: "Beware 'new era' thinking; i.e., it's different this time because … "

Those truisms have been in and out of play this year, with the strong equity market rally off last October's lows sometimes begging the question of whether the market was fighting the Fed. The (up)trend had certainly befriended many equity investors. What's interesting is that on Marty's list of trading rules, number six specifically read: "Don't fight the Fed (less valid than #1).

Long and variable lags

Most investors know that the effects of monetary policy (on the economy) operate with "long and variable lags." We've read a lot this year about a "new era" of irrelevance around the inversion in the yield curve and/or the plunge in leading economic indicators. We do not think the economy (or the market) has passed the expiration date on those lags. Some consideration—or version—of that is likely a contributor to the recent pullback in stocks.

As July came to a close, the S&P 500 was less than 5% from its early-2022 record high. What changed?

- Treasury yields surged to their highest levels since the period before the Global Financial Crisis;

- Increased focus on the federal budget deficit, high debt levels and the elevating cost of servicing the debt;

- U.S. economic growth has surprised on the upside, while inflation remains sticky (bringing Federal Reserve rate hikes potentially back into the picture);

- Concerns about the ripple effect of China's weak economic growth;

- S&P 500 earnings did not surprise into positive growth territory and forward estimates have been trending lower;

- Investor sentiment had become a bit frothy alongside elevated valuations.

Related to earnings, all of the appreciation in the stock market since last October came from multiple (P/E) expansions, with no aid from the denominator in the equation (earnings). Add the surge in yields into the mix and it was a recipe for a pullback—particularly among the most richly valued segments of the market.

The surge in yields is partly explained by the increased supply of Treasuries associated with the burgeoning federal budget deficit, which brings with it rising debt servicing costs. This finally seems to be capturing the market's attention. As we posited in our 2023 outlook report, written late last year, government indebtedness and its costs will be a growing part of the macro conversation. We will be writing more on this topic in future reports, so stay tuned.

Drawdown #2

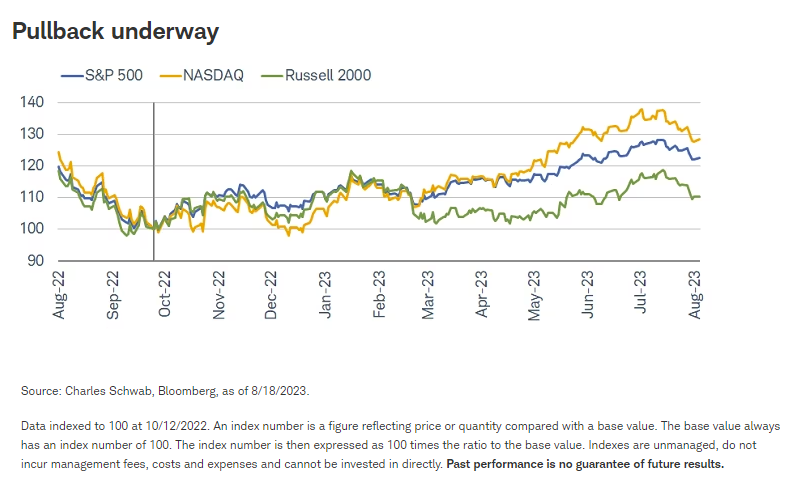

As shown below, the S&P 500 has had a near-5% drawdown from its late-July high, while the NASDAQ's and Russell 2000's recent drawdowns are both around 7%. The pullback has not been near enough to destroy still-healthy year-to-date gains, but there is likely still more downside (or at least higher volatility). As a reminder, this is the second notable pullback this year, with the first (and more significant) one occurring from early February to mid-March around the regional bank failures.

Prior high-flying stocks have taken it on the chin. The chart below, seen every day on my X (formerly known as Twitter) feed, shows the maximum drawdowns for the "super 7" stocks that had dominated performance this year through May. When June rolled around, those stocks had represented virtually all of the S&P 500's performance. At the same time, only 15% of the S&P 500's members were outperforming the index over the prior 60 days (a record low back to at least 1990). We contended at the time that concentration risk was elevated and that some convergence in performance was likely. That's what began in early June.

Some halitosis

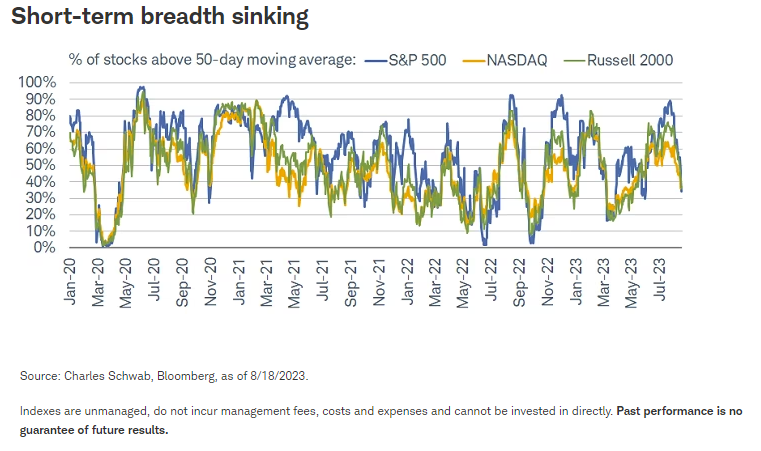

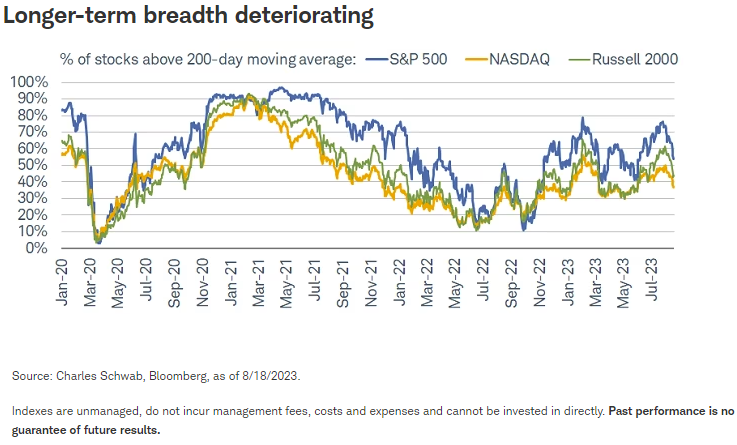

More recently, breadth has deteriorated across and within the major indexes. Shown below are the percentage of stocks trading above their 50-day (top chart) and 200-day (bottom chart) moving averages. In each case, the recent high in breadth was lower than the prior high, while it looks like there is probably more to go on the downside.

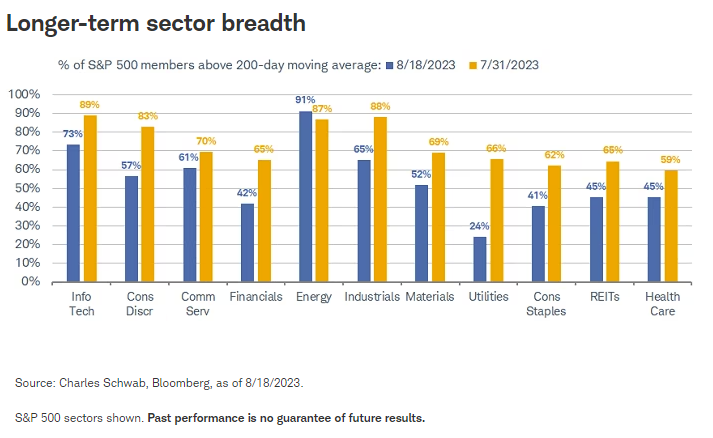

At the sector level, shifts have been fairly stark. Shown below, as of the end of July, only two sectors (Health Care and Consumer Staples) had less than 70% of their stocks trading above their 50-day moving averages; with Energy at 100% and three other sectors with at least 90%. Fast-forward to Friday's close, even Energy has seen a little breadth deterioration, while it has been particularly stark for Utilities and REITs.

In terms of the longer-term 200-day moving average, Energy has actually had a lift since the end of July, but that's the only sector without some deterioration. Relative to the 50-day moving average, Utilities have retreated the most. The relative weakness in Utilities tells a connected story to the surge in Treasury yields: The attractiveness of dividend yielders has lessened alongside the renewed "income" in fixed income.

Patchy quilt

Last year was Energy-dominated, both in terms of sector performance and the contribution from the sector's earnings. Its outperformance in terms of both market performance and earnings contribution faded with the market's lift-off last October's low, with the "growth trio" of Technology, Consumer Discretionary and Communication Services (housing the "super 7" group of stocks) taking the lead. Below is our "sector quilt," ranking the 11 S&P 500 sectors from top-to-bottom on a monthly basis over the past year.

Quilts like that for sectors above—as well as the more traditional broad asset class quilts—are always a healthy reminder of the benefits of diversification (and periodic rebalancing) both across and within asset classes.

The "Growth" trade vs. the "growth" trade

Alongside the focus on performance at the sector level, is an update on growth and value—not least because a handful of sectors can often drive outsized gains in the (uppercase G and V) Growth and Value indexes. Regular readers of our work know that we prefer to focus on the factors/characteristics of (lowercase g and v) growth and value since the index labels can often deviate from what is perceived by investors to be each style.

To explain further, we'll link to a report we wrote in March, in which we discussed an important rebalance that took place in December 2022 for the S&P Growth and Value Indexes. We'll focus on the Pure Growth Index in this report given it houses stocks that cannot exist in the Pure Value Index, and because the "growth trade" has come into focus this year—accentuated by the significant outperformance (until June) of large-cap stocks and indexes that are often considered to be in the growth family.

After the December 2022 rebalance of S&P 500 Pure Growth, all but one of the "mega-cap eight" stocks stayed in the index: Apple. All others (such as NVIDIA, Tesla, and Microsoft, etc.) were moved out. At that point, Technology had gone from representing 37% of the S&P 500 Pure Growth index to only 13%. The inclusion of more Energy stocks—given their outsized earnings growth last year—brought that sector to the top of the list of represented sectors in the Pure Growth index, with Health Care moving to the number two spot.

So, here's where it gets interesting now that we find ourselves with year-to-date performance that has still been dominated by the largest "growth" stocks (for example, NVIDIA is up by nearly 200%). Any group of investors would likely still consider the mega-cap eight to be growth stocks today, yet given the nature of December's index rebalancing, they are missing from S&P 500 Pure Growth despite their huge runs this year.

As such, as shown below, S&P 500 Pure Growth has underperformed the Tech-heavy NASDAQ 100 considerably year-to-date, with the former up only 2.1% and the latter up a whopping 34.3%. For two indexes that essentially moved in lockstep last year—and that are often considered to be emblematic of the large-cap growth trade—the split in performance this year is glaring. Not only that, but this has occurred even after the NASDAQ 100 underwent its own special rebalance in July, which diluted the weights of the mega-cap names.

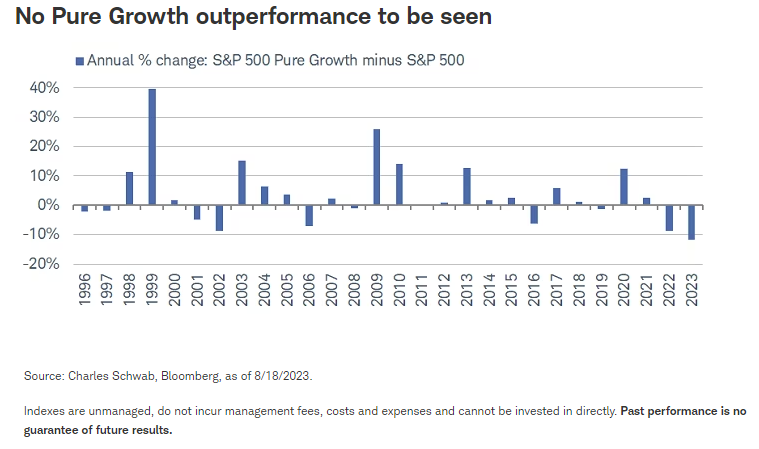

Looking at the mediocre performance of S&P 500 Pure Growth from another angle, you can see another index effect in the chart below. With the widely watched S&P 500 Index not having booted any mega-cap members, S&P 500 Pure Growth is underperforming the S&P 500 by 11.7% this year. If that holds, it will be the worst spread in the history of Pure Growth's existence; and as of now, cumulative underperformance over the past two years is by far the worst stretch in history.

This dynamic is a clear example of why we encourage investors to invest in growth and value based on factors/characteristics, not only index labels. Maintaining a focus on the former would have kept those with a growth bias on the right side of the trade this year. For index-oriented investors, the lesson is to know exactly what stocks are in each index, regardless of label (and/or preconceived notions). There is often too much of a focus on outperforming an arbitrary benchmark and trying to find the next hot segment of the market. Given that no one can pick tops and bottoms for stocks and/or indexes, a more feasible course of action is broadening one's knowledge bank to minimize negative surprises along the way.

In sum

The upside breakout in Treasury yields has weighed on equity multiples, which expanded since last October without the benefit of earnings growth. The pressure has been more acute on the more richly valued mega-cap tech and tech-oriented stocks. Some reversal is likely needed to establish a better footing for stocks. Better-than-expected recent economic activity, coupled with sticky inflation, is likely to keep uncertainty regarding Federal Reserve policy elevated. Fed Chair Jerome Powell has his much-anticipated speech at the Fed's annual confab in Jackson Hole later this week. It's possible he could try to establish some calm in the Treasury market. In the meantime, we continue to recommend that equity investors use diversification and periodic rebalancing to lessen risks while staying up in quality with a factor-oriented approach.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. The examples provided are for illustrative purposes only and are not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistics.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Rebalancing does not protect against losses or guarantee that an investor's goal will be met. Rebalancing may cause investors to incur transaction costs and, when a non-retirement account is rebalanced, taxable events may be created that may affect your tax liability.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

S&P 500 Pure Growth is a style-concentrated index designed to track the performance of stocks that exhibit the strongest growth characteristics by using a style-attractiveness-weighting scheme.

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 am ET. Click here to register.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All