5 Things to Consider About Taxable Municipal Bonds

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsTaxable municipal bonds may be an attractive option for investors in lower tax brackets, but there are things investors should know before making a decision.

There's a small portion of the bond market that investors may have overlooked but now may want to consider—the taxable municipal bond market.

Most munis pay interest that is exempt from federal and potentially state income taxes. However, interest on some municipal bonds is subject to both federal and state income taxes. These bonds, known as taxable municipal bonds, generally pay higher interest rates than tax-exempt munis to make up for the lack of tax benefits.

Below are some of the primary reasons we think investors should consider taxable munis. But first, a quick introduction to taxable municipal bonds:

A primer on taxable munis

The main difference between a taxable municipal bond and a tax-exempt muni is that taxable munis pay interest income that's subject to federal and state income taxes, whereas tax-exempt munis pay interest income that's generally exempt from federal and state income taxes. They're often issued by the same issuer and therefore don't differ in credit quality. For example, issuers like the State of California, the New Jersey Turnpike Authority and the University of Michigan, just to name a few, all issue both taxable and tax-exempt munis. An issuer may choose to issue a bond as either a taxable or tax-exempt issue for a variety of reasons, such as the yield environment or to attract a different investor base to increase demand for their bonds.

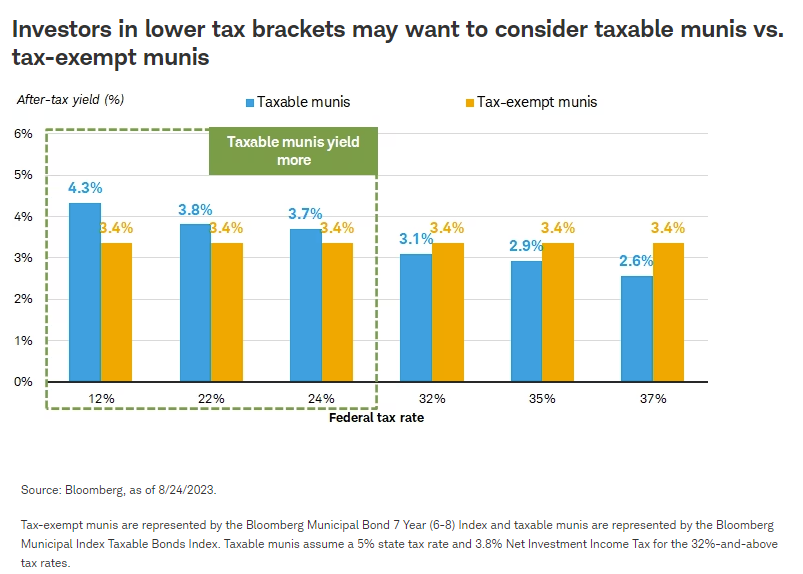

Due to the different tax treatments between taxable and tax-exempt munis, we believe that taxable municipal bonds may be an attractive option for investors in lower tax brackets or for tax-advantaged accounts like an individual retirement account (IRA). Investors in higher tax brackets may still want to consider tax-exempt munis, as they may yield more than taxable munis after considering the effects of taxes.

Five things to know

1. Taxable munis offer attractive yields relative to tax-exempts.

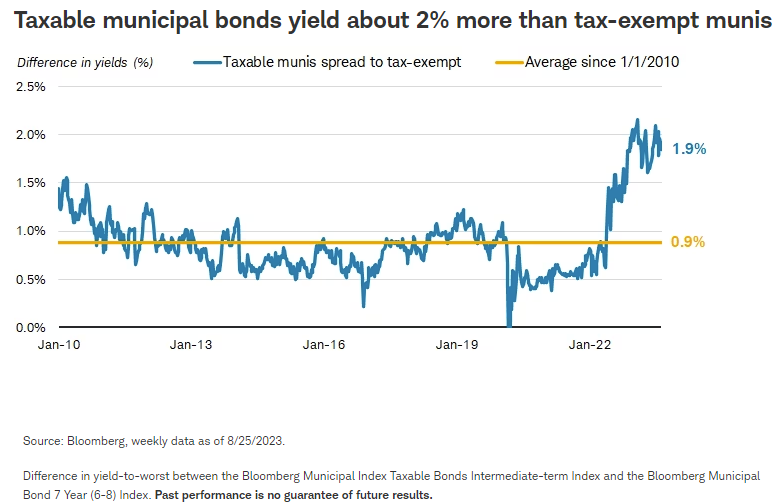

Yields for taxable municipal bonds are attractive, in our view, compared to tax-exempt munis of similar maturities. For example, since January 2010, on average, an index of taxable municipal bonds has yielded 0.9% more than an index of tax-exempt municipal bonds. Only during a brief period in March 2020 when the market was very volatile due to the onset of the COVID pandemic crisis did taxable munis yield less than tax-exempt munis. Today, that difference is close to its highest point since January 2010.

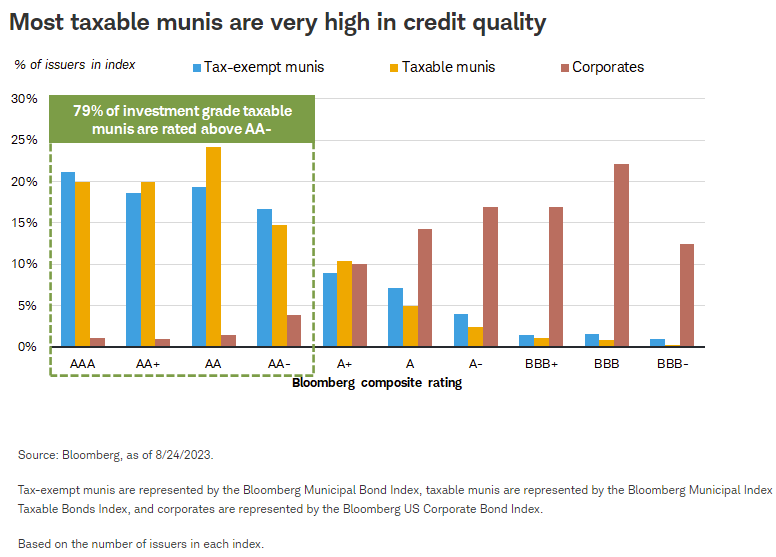

2. Taxable munis are generally high in credit quality, like tax-exempt munis.

Another potential benefit of taxable munis is that they're generally higher in credit quality than other alternatives. For example, 79% of the taxable muni market is rated in the top two rungs of credit quality–AA minus or above.1 This compares to 76% for the tax-exempt muni market and only 7% of the corporate market, as illustrated in the chart below.

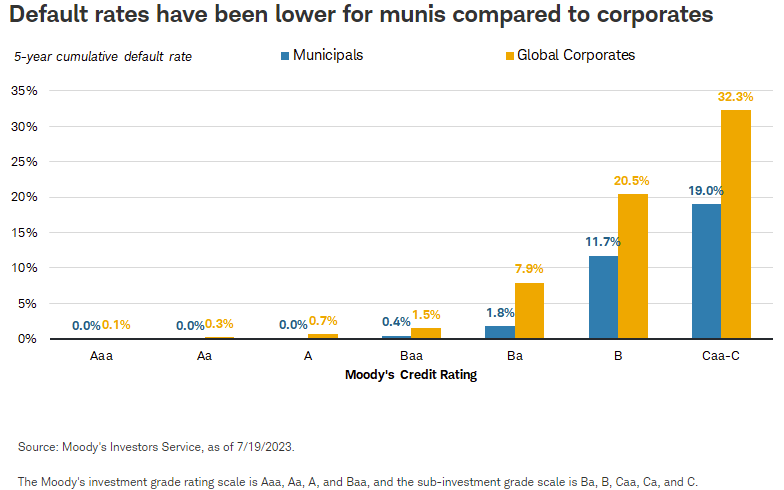

This is notable for investors because higher-rated issuers tend to default—that is, to miss an interest or principal payment—less frequently than lower-rated issuers. For example, over a five-year period ending in 2022, 0.4% of Baa rated munis defaulted, according to Moody's Investors Service. During the same period, lower-quality B rated munis defaulted 26 times more often, at a rate of 11.7%.

Moreover, municipal bond issuers, which include issuers of taxable munis, tend to default less frequently than corporate bond issuers. Looking at the Baa rated cohort, the default rate for munis was 0.4%, compared with 1.5% for corporates.

However, taxable munis do have some risks. Here are two of the most prominent:

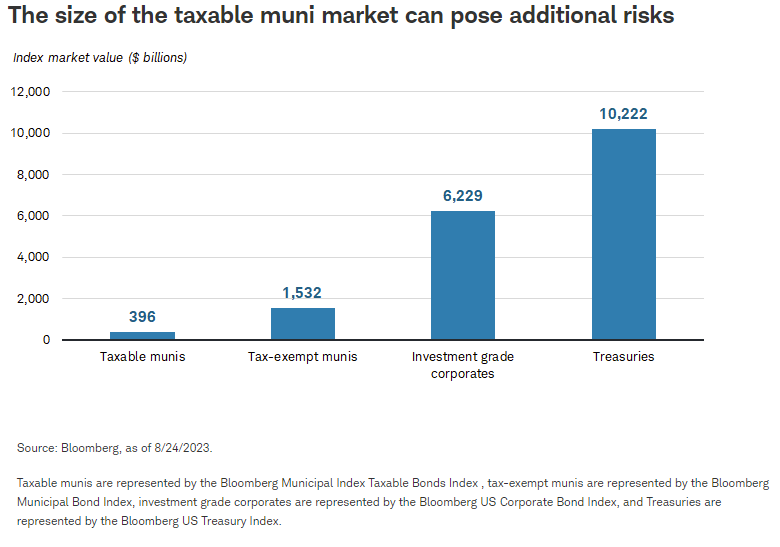

3. The relatively small size of the market

Although issuance has risen recently, the taxable muni market is much smaller than many other fixed income markets, as illustrated in the chart below. Smaller markets are generally less liquid than larger ones, like the Treasury market, which means that it can be more difficult to sell your bond if you need to. Therefore, we suggest that if you're considering taxable munis, plan on holding them until maturity. The smaller market and lower liquidity of taxable munis is also an issue for investors in funds like exchange-traded funds (ETFs) or mutual funds.

Due partly to the size of the market, there aren't many mutual funds or ETFs that invest solely in taxable municipal bonds. In fact, there is only one open-ended ETF that we know of that invests in taxable municipal bonds and doesn't use leverage. Leverage generally means using borrowed funds to try to amplify returns. However, leverage can also amplify negative returns. Bonds that are less liquid are generally more volatile in times of market stress.

4. A large portion of taxable munis are from smaller issues

Nearly one-third of all taxable munis are small issues and therefore not eligible to be included in the broad taxable muni index. This is important because passive strategies like ETFs that track the benchmark will generally not invest in these smaller issues which can reduce some diversification benefits.

5. The taxable muni index is sensitive to interest rate changes.

First, the taxable muni index has a longer average duration—which makes it more sensitive to changes in interest rates—than the tax-exempt index. For investments such as ETFs or passively managed mutual funds that simply track the index, investors are taking on greater interest rate risk with taxable munis compared to tax-exempt munis. This is the main reason taxable munis have underperformed other fixed income investments this year. If rates rise more than we expect, total returns for taxable munis would likely underperform their tax-exempt counterparts even more.

What to consider now

For investors in high tax brackets, we generally don't see value in taxable munis. However, investors in lower tax brackets or those investing a tax-sheltered account like an IRA may want to consider a small allocation to taxable munis to complement their other fixed income holdings.

Schwab clients can log in to their accounts and search for individual taxable munis using the "Federally Taxable" dropdown menu under "Search by Product" on Schwab BondSource on Schwab.com. Clients can also search for funds like ETFs or mutual funds on Schwab.com that invest primarily in taxable munis. If you need additional help, reach out to a Schwab Fixed Income Specialist for guidance in selecting the investments that are right for you.

1The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment-grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

Investors should consider carefully information contained in the prospectus, or if available, the summary prospectus, including investment objectives, risks, charges, and expenses. You can request a prospectus by calling 800-435-4000. Please read the prospectus carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results.

Investing involves risk including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

Tax-exempt bonds are not necessarily a suitable investment for all persons. Information related to a security's tax-exempt status (federal and in-state) is obtained from third parties, and Schwab does not guarantee its accuracy. Tax-exempt income may be subject to the Alternative Minimum Tax (AMT). Capital appreciation from bond funds and discounted bonds may be subject to state or local taxes. Capital gains are not exempt from federal income tax.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

Diversification and asset allocation strategies do not ensure a profit and cannot protect against losses in a declining market.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes please see schwab.com/indexdefinitions.

The Bloomberg Municipal Index Taxable Bonds Intermediate-term Index is a sub-index of the Bloomberg Municipal Index Taxable Bonds Index.

The Bloomberg Municipal Bond 7 Year (6-8) Index is a subset of the Bloomberg Municipal Bond Index that measures the performance of investment-grade issues with remaining maturities of six to eight years.

The Bloomberg Municipal Bond Index measures the performance of the investment grade, US dollar-denominated, long-term tax-exempt bond market. The index includes four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and pre-refunded bonds. It is a market-value weighted index.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All