Piece of Work: Dissecting Labor Market Trends

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe August jobs report confirms the labor market's continued slowdown, which is for now consistent with the Fed's soft-landing desires—but not without warning signs.

Just ahead of the Labor Day Weekend, which was glorious in our neck of the woods, was the monthly jobs report, released on Friday morning. It was also a sad day for Parrotheads everywhere when the news hit of the death of Jimmy Buffett, of whom I (Liz Ann) was a big fan. I had the pleasure of meeting him in 2008, and he was a true joy. The title of this report is in his memory.

Deceleration

In a sign of some renewed economic weakness, and marking the continuation of decelerating job growth, the Bureau of Labor Statistics (BLS) announced last Friday a headline payrolls increase of 187k. It was more than economists expected, but the rub was that the prior two months' revisions were -110k. The unemployment rate jumped 0.3% to 3.8%; but that was for a "good reason" as the labor force participation rate rose 0.2% (a 746k surge in the labor force) to 62.8% in another sign of a loosening of labor market conditions.

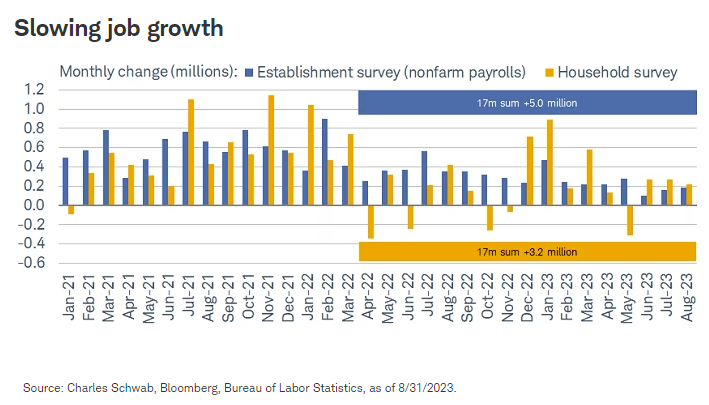

The BLS's household survey's job tally, from which the unemployment rate is calculated, jumped by 222k. As shown below, over the past 17 months (dating back to the first drop in this cycle in the household survey), the BLS's establishment survey (payrolls) suggests a much more robust labor market relative to the household survey. For what it's worth, the latter tends to lead the former heading into weaker economic environments.

In addition, and receiving surprisingly little attention, was the preliminary "benchmark" revision released by the BLS in August which showed 306k fewer jobs than originally reported for the one-year period through March 2023. The revision tally for private sector jobs was -358k. Payroll gains have clearly decelerated; with 2022's monthly average of nearly 400k in contrast to the past three months' average of 150k.

Friday's report marked the seventh consecutive month of negative revisions, as shown in the blue bars below. The last time there was a streak that long was in 2008. Revisions data only go back to 1997, so that means current streak and 2008 streak are the only two during that span when there were at least seven months of consecutive negative revisions. The cumulative revisions in nonfarm payrolls, which includes jobs in both the private sector and government, since January 2022 (orange) are -181k, while since January 2023 (green) they are -355k.

History lesson

Some commentary lately has suggested the labor market is "past the expiration date" in terms of the lead between Federal Reserve tightening cycles and a rise in the unemployment rate. Not true. Looking at all Fed rate cycles since the mid-1960s, the average span between the start of a hiking cycle and the trough in the unemployment rate has been 23 months, with a range between 12 months (in the early-1980s) and 36 months (in the mid-2000s). The Fed began raising interest rates 18 months ago in this cycle.

Good news from the perspective of the Fed's inflation-fighting efforts was that wage growth did slow modestly. Shown below, average hourly earnings rose +4.3% year-over-year in August, down from +4.4% in July. Average weekly hours did tick higher from 34.3 to 34.4, but that remains down from peak of 35 in January 2021. That said, the news recently from the Big 3 automakers, UPS, the major airlines, and West Coast dock workers point to ongoing/upward wage pressures.

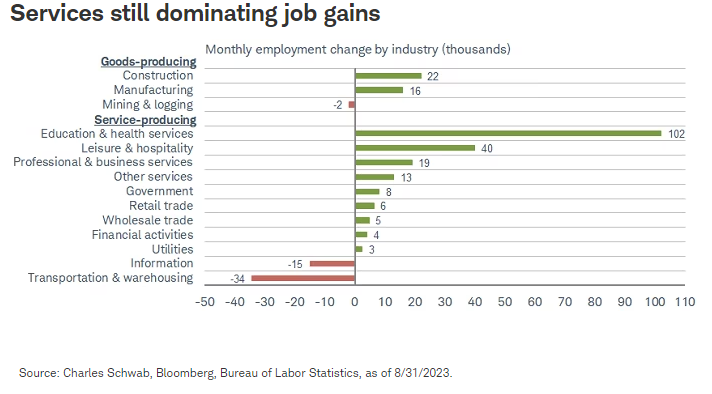

Private sector payrolls were decent at 143k, with private goods producing jobs up 36k. As shown below, the services sector continues to have the strongest payroll gains—with last month dominated by education and health services—in addition to another gain for leisure and hospitality. Bringing up the rear was transportation and warehousing—largely explained by the demise of the nearly 100-year-old Yellow Corp.—and the information sector.

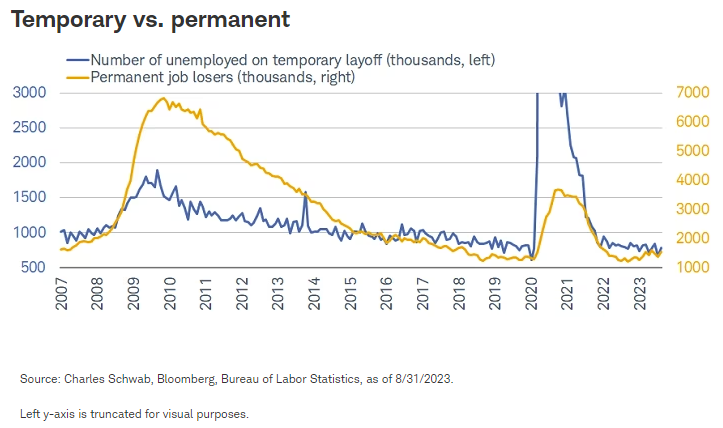

A key leading indicator, temporary layoffs ticked up, but have largely been moving sideways for more than a year. There was a 336k increase in permanent job losses from the most recent trough, which is getting closer to the jumps in advance of the recessions that began in 2007 (524k) and 2001 (400k). Both are shown below, with the scale for temporary layoffs truncated due to the extremes associated with the early part of the pandemic in 2020 through 2021.

From open to close

Arguably capturing as much attention as the jobs report last week was the July update for job openings. Despite the one-month lag and the fact that the data only go back to 2000, the Job Opening and Labor Turnover Survey (JOLTS) numbers were in line with what the Fed is looking for in a less tight labor market. That doesn't come without some warning signs, however.

As shown in the top panel of the chart below, the total number of job openings fell to 8.8 million in July (the lowest since March 2021), down markedly from the peak in March 2022. Given that the unemployment rate remains low at 3.8%, the magnitude of the decline in job openings means the Fed is currently finding success in its goal of crushing labor demand without causing a massive spike in unemployment.

Worth watching, however, is the pace of the decline in demand. As shown in the bottom panel, 1.49 million job openings have been shed over the past three months. In the history of the data, there has only been one other period with a larger decline (April 2020). Thus, our oft-used phrase is at work here: when it comes to market and economic data, "better" or "worse" tend to matter more than "good" or "bad." Put another way, the overall level of job openings is getting closer to a territory in which the Fed's soft-landing goal looks achievable. Yet, a continued and/or more precipitous decline would bolster a worsening trend that is usually seen in recessions.

We always encourage looking beyond the number of job openings for myriad reasons, not least because the definition of an actual opening—as is used for JOLTS—is quite wide-ranging. As an example, per the BLS, both a job posting on the internet and simply "networking" with colleagues about job opportunities are considered openings. The former is more formal than the latter, but both carry the same weight in the survey, which means the total number of openings is arguably overstated.

As such, looking at the other data within the JOLTS report gives us more of an indication as to how tight the labor market is. Both the quits and hires rates—shown below—show a sharper degree of loosening. The decline in the former underscores workers' decreasing confidence about leaving their current jobs. While that is mostly consistent with easing wage pressures (a plus for the Fed), the pace of the decline has picked up to a recessionary-like speed. In addition, the hires rate has fallen rather quickly.

In sum

The latest labor market data confirms the slowdown thesis. Specific to the JOLTS data, if the declines in quits and hires are not arrested, favorable soft-landing signs will start to turn into recessionary warnings. Momentum tends to feed on itself when it comes to labor data. The good news is it works in both ways; the bad news is the current path is toward a weakening state. Economic landings always look soft until they don't. While a soft landing shouldn't be ruled out, we also think investors need to view the data through a realistic lens when it comes to some of the pace of the declines in certain data. The labor market (and the Fed) cannot have it both ways.

The probability—based on positioning in the fed funds futures market—of a pause at the September Federal Open Market Committee (FOMC) meeting has jumped from 86% a week ago to 93% as of this writing. However, there remains a 38% probability of another hike at the Fed's November meeting, although that's down from 42% a week ago. We continue to believe that there is a possibility the Fed is already done hiking rates in this cycle, but that they are biased toward keeping rates high for an extended period in the interest of conviction around inflation not reigniting.

Finally, we continue to emphasize our "rolling recession" thesis and that best-case scenario is not really a traditional soft landing. For some economic segments—like housing/housing-related, manufacturing, consumer-oriented goods—hard landings have already occurred. Best-case scenario, therefore, would likely be a continuation of the "roll through," with stabilization/improvement in areas previously hit offsetting burgeoning weakness in areas of more recent strength—including the labor market.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistics.

The policy analysis provided by Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All